ON OVERVIEW OF UNIVERSAL LIFE INSURANCE POLICY

Introduction

Life Insurance provides financial security to the insured’s dependents or loved ones, if something were to happen to insured unexpectedly. There are lots of plans available in life insurance, but universal life insurance combines the best options to the insured. It is the affordability of term insurance with the long-term security of permanent or whole life insurance.

Universal life insurance is type of flexible permanent life insurance offering the low-cost protection of term life insurance as well as a savings element (like whole life insurance), which is invested to provide a cash value buildup. Unlike whole life insurance, universal life insurance allows the policyholder to use the interest from his accumulated savings to help pay premiums over time.

Universal Life Insurance Definition

Universal life (UL) insurance is a hybrid life insurance policy which combines elements of term life insurance with an investment savings option. Universal life combines the ability to build savings at the same time provides a life insurance policy. This allows flexibility in choosing savings or investment portion of the premium.

Universal Life Insurance policy is a cash value life insurance policy that combines the low cost of Term Insurance with the savings options and lifelong coverage of Whole Life.

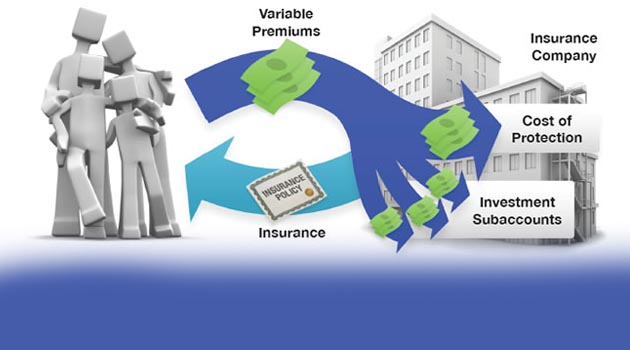

Universal Life insurance working Model

Universal life insurance was created under the umbrella of permanent life insurance options to provide more flexibility than whole life insurance. Premiums within a universal life insurance policy are broken down by the insurance company into two categories namely the cost of insurance and a saving component known as the cash value.

The cost of insurance must be covered so the policy remains in force, but premiums may be shifted over time based on the policyholder’s needs. Premiums paid over the minimum cost of insurance accumulate within the cash value portion of the policy, and funds can be used to pay premiums. For example, if the savings portion is earning a low return, it can be used instead of external funds to pay the premiums. As long as the minimum cost of insurance is covered, either through paid premiums or cash value, the policy is guaranteed for as long as the initial contract dictates.

In simple universal life insurance policy has two accounts, namely a savings account and the life insurance account. Each month the premium plus interest goes into the savings account. At the same time, the company transfers money into the insurance account to pay the cost of insurance plus any related fees.

Origin and Development of Universal life insurance

Prior to the 1980s, insurers sold primarily fixed-premium term and whole-life insurance to individual policyholders. Acute competition significantly reducing sales of whole-life products, insurers had little choice but to innovate in the 1980s to meet demand. They did so by redesigning whole-life into a hybrid product that included a traditional income protection component and a long-term investment component using market-based yields (and thus were interest return–sensitive). The first of these new complex products, universal life insurance, revolutionized the industry. Its popularity was rooted in its flexibility.

By the mid-1980’s, variable universal life insurance had emerged as a means of pairing the flexibility of traditional universal life insurance with the investment choices offered through variable life insurance. By the turn of the twentieth century, low-interest rates spurred many insurers to begin marketing indexed universal life insurance. Indexed universal life insurance combines the potential for market-based growth with protection from negative market returns. Sales of this product have grown considerably over the last decade as those nearing retirement seek to balance risk with growth that will support retirement income needs.

Features of Universal Life insurance

Beyond lifelong protection, there are a few additional features of universal life policy

- Withdraw money or borrow against the policy

- Earn Interest on Cash Values

- Flexibility with premiums.

- Adjust the death benefit.

- Withdraw money or borrow against the policy

- Earn Interest on Cash Value

- Flexibility with Premiums

- Adjust the Death Benefit

- Increase or decrease the premium

- Increase or decrease the sum assured by the company

- Lengthen or shorten the guaranteed protection period and

- Lengthen or shorten the premium payment period.

- The timing and amount of premium payments

- The net rate of return earned on the interest accounts

- The type of cost of insurance and death benefit option selected

- Cash withdrawals if any by the policy holders

- Outstanding balance of any policy loans

Leave a Reply