ENHANCING PROFITABILITY IN INDIAN LIFE INSURANCE INDUSTRY-A PROPOSITION

Abstract

With more than 35,000+ crore deployed as capital and over 11003 branches becoming operational Life Insurance companies are still grappling to wipe out accumulated losses. Going slow on expansion Insurance companies are attempting to take an evaluated risk. Commencing operations without grasping the determinants of profitability is bound to be fragmentary and incomplete. Because of long term nature of Insurance business there is no predetermined criterion to measure the effectiveness of operating companies. Hence for accounting purpose insurance companies rely on bookkeeping practices to land at profit for the financial year. This may offer us fractional info and will not provide us the factual viewpoint. Concept of embedded value where we examine the future cash flows at present moment is also not extensively received as it lacks accepted criterion. During initial years Insurance companies were investing heavily to build distribution but the ROI took unusually long time. Companies are adopting standard practices thanks to regulatory interventions at frequent intervals which only reiterate a point that cost effective products need to be offered to customers to gain their confidence and market share.

INTRODUCTION

At present many insurance companies are suffering loss which is a disturbing trend. It is because of the descending fortunes of the Indian life insurance industry which until a few years before was considered to be a sunrise industry guaranteeing decades of uninterrupted growth and loads of profits for shareholders. And year-on-year there is a decline in new business premium which is the yardstick to measure the efficiency of capital deployment. Charges of ambiguous sales pitch by agents led to the Insurance Regulatory and Development Authority step in with fitted controls on how a product is sold. The field that was unregulated i.e. agent commission which was never regulated also drew regulatory attention. There was a massive correction in the way insurance is being sold after both the regulators – SEBI and IRDAI indulged in public animosity on who controls the Unit Linked Insurance Plan (ULIP) which was similar to mutual fund units. Commission on unit-linked products has come down to 5% from as high as 18%. Hence, the sales also decreased which made insurance companies incur further losses.

Industry had lost more talents with a massive breakout of agents since 2010. The total number of agents dropped by 5 lakhs from 26.39 lakhs in March 2010 to 20.67 lakhs at the end of March 2015. Economic mishandling over the last few years had its undesirable influence. Inflation also averaged 10% at the consumer-level for much of the past decade and lowering employment coupled with drop in savings ratio all have compounded the already struggling insurance industry into chaos which kept potential buyers away from buying insurance policies. When industry is struggling not everyone would be willing to commit for a long haul in this scenario especially when growth rate was falling to decade low of 5% and salaries are forecast to grow only between 10 and 12% against the 20-30% in the past magnificent years.

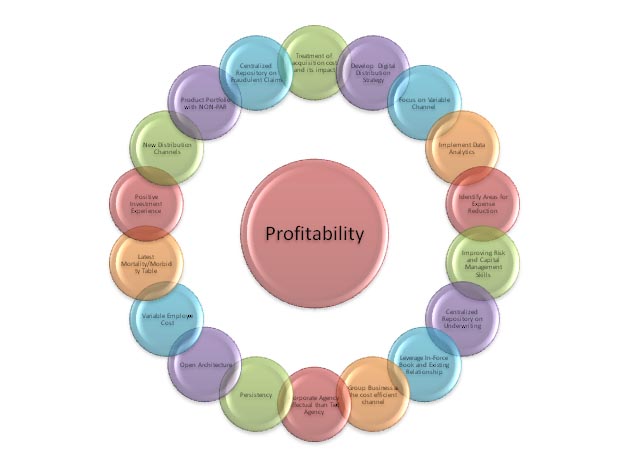

While we have many factors which influence the profitability of Life Insurance Companies the most prominent one are mentioned as below.

REFERENCES http://www.lifeinscouncil.org/about-us/industry-overview irda.gov.in policyholder.gov.in IRDA Annual Report 2013-14

- Treatment of acquisition cost and its impact

- Develop digital distribution strategy

- Focus on variable channel

- Implement data analytics

- Identify Areas for Expense Reduction/Efficiency Build Up

- Improving risk and capital management skills

- Centralized repository on underwriting

- Leverage in-force book and existing customer relationships

- Groupbusiness as the cost efficient channel

- Corporate Agency effectual than tied agency

- Persistency

- Positive Investment Experience

- New Distribution Channels

- Online/internet gateways

- Direct marketing and Telemarketing

- NGOs and affinity groups

- Insurance Marketing Firms

- Web Aggregators

- Worksite Marketing

- Product Portfolio with Non-Participating Plans

- Centralized repository on Fraudulent Claims

- Open architecture in both banking and tied

- Variable Employee Cost

- Latest Mortality/Morbidity Table

- INDIAN ASSURED LIVES MORTALITY (2006-08) ULT.

- MORTALITY FOR ANNUITANTS – LIC (A) (1996-98) ULTIMATE RATES

Author

Research Guide

Dr.Ashok Kumar,

Professor and Head of Department, Management,

Karpagam University, Coimbatore.

Research Scholar

Ramesh Kumar Satuluri, FIII, CFP, ALMI, MFA,

Research Scholar of Management,

Karpagam University, Coimbatore.

REFERENCES http://www.lifeinscouncil.org/about-us/industry-overview irda.gov.in policyholder.gov.in IRDA Annual Report 2013-14

Leave a Reply