UNINSURED AND UNDERINSURED MOTOR VEHICLES IN INDIA

Almost a third of cars on Indian roads may not have mandatory third-party liability insurance, according to analysis by insurance companies. The insurance companies exposed the cover shortfall by comparing the number of registered vehicles with the number of policies issued. Uninsured vehicles are a problem in motor insurance. Nearly 70% of two-wheelers and 30-35% of four wheelers are uninsured. It is clearly a challenge to society as victims of accidents caused by these vehicles do not get adequate compensation. Some insurers estimate that the number of uninsured vehicles on road could be lower, however, around 20-25% of cars are uninsured and in two-wheelers the uninsured vehicles are likely to be around 50%. In two-wheelers, the renewals of first year policies are as low as 25%. Although most of the insurers do send renewal notices, lower premium on two-wheelers make it difficult to do a personalized follow-up. Some insurers have proposed the adoption of long-term policies, but this poses its own challenges. Issuing long-term policies is a challenge because it is difficult to predict the movement of income and inflation over a long period. In some markets in Europe and the US, insurers issue only six-month policies. However, there are discussions on long-term insurance policies for some segments of vehicles, which may be filed with the regulator for approval shortly. When an owner refuses or is unable to carry motor vehicle insurance, that owner puts more than just him- or herself at risk. If he injures another person, the compensation will not be there to cover the damages. Other damaged vehicles, however, may be covered by their own insurance policies.

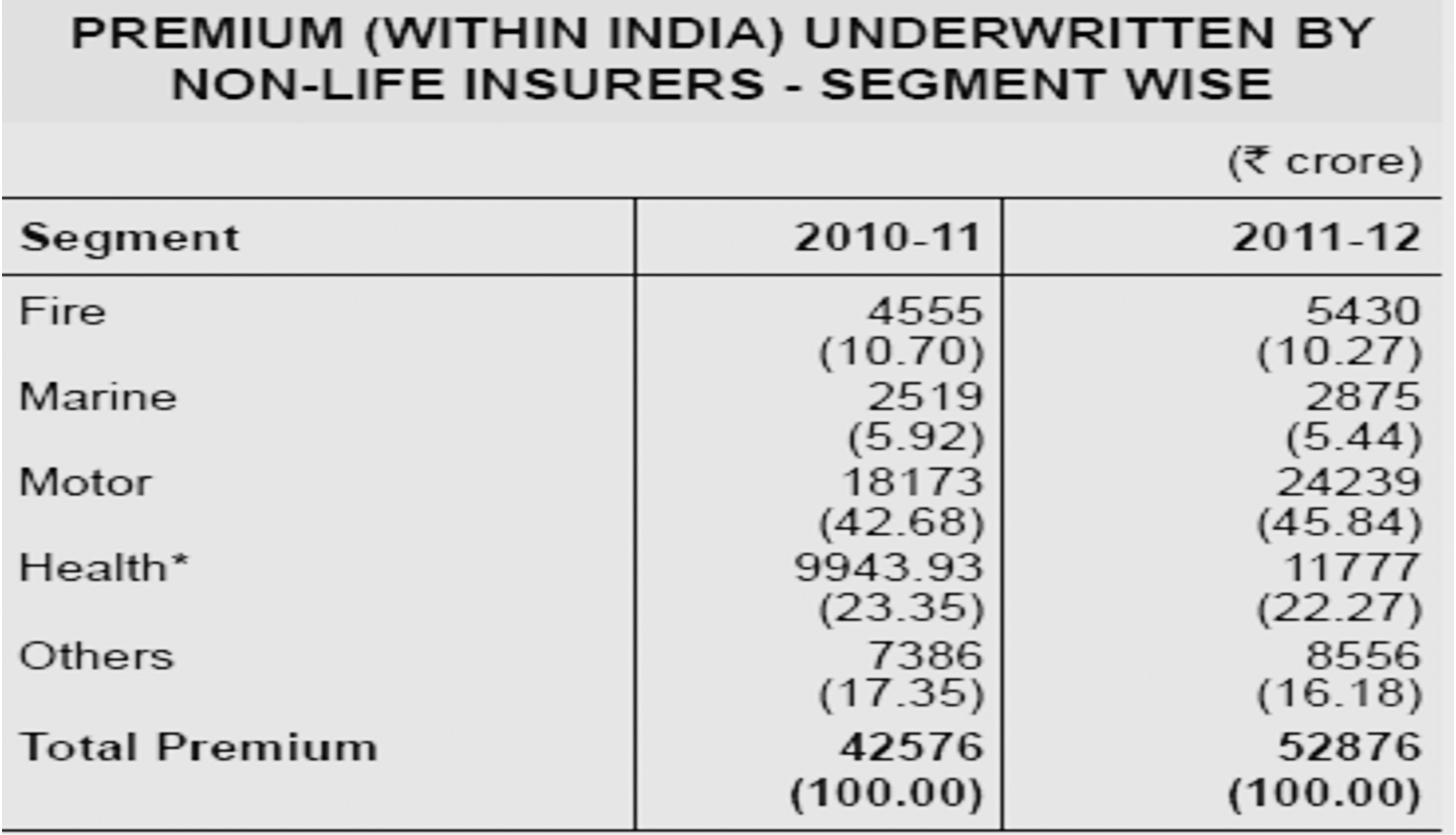

Not only should the vehicle be covered by a valid insurance but should also be driven by a person who has a valid license. In the case of commercial vehicles, validity of permit and fitness should be observed. Pricing in motor insurance has gone in for a sea change in the last five years. Prior to de-tariffing (where prices are market-driven) in 2007, the main factors governing motor insurance premium pricing was the year of manufacture of the vehicle, engine capacity, price and the zone in which the vehicle was bought. While these four factors continue to play a role in determining the insurance premium, other factors such as occupation are also playing an important role in determining the pricing of the motor cover. Insurers are seeing the emergence of differential premium pricing with respect to profession. Insurers are giving positive rating for some professions. This is translating to a discount of 5% on tariff premiums. Motor premiums contribute to nearly 40% of general insurance premium collected by insurers. The contribution of motor is significant to a company’s top line as well as bottom line. This has resulted in a lot of pricing sophistication in this line of business. A lot of segmentation is happening in the motor insurance space. Companies want to have a profitable set of customer. They are doing so by loading customers who are bound to give more losses and discounts to people who are giving profits. The segment wise premium position of general insurers was as follow:

Not only should the vehicle be covered by a valid insurance but should also be driven by a person who has a valid license. In the case of commercial vehicles, validity of permit and fitness should be observed. Pricing in motor insurance has gone in for a sea change in the last five years. Prior to de-tariffing (where prices are market-driven) in 2007, the main factors governing motor insurance premium pricing was the year of manufacture of the vehicle, engine capacity, price and the zone in which the vehicle was bought. While these four factors continue to play a role in determining the insurance premium, other factors such as occupation are also playing an important role in determining the pricing of the motor cover. Insurers are seeing the emergence of differential premium pricing with respect to profession. Insurers are giving positive rating for some professions. This is translating to a discount of 5% on tariff premiums. Motor premiums contribute to nearly 40% of general insurance premium collected by insurers. The contribution of motor is significant to a company’s top line as well as bottom line. This has resulted in a lot of pricing sophistication in this line of business. A lot of segmentation is happening in the motor insurance space. Companies want to have a profitable set of customer. They are doing so by loading customers who are bound to give more losses and discounts to people who are giving profits. The segment wise premium position of general insurers was as follow:

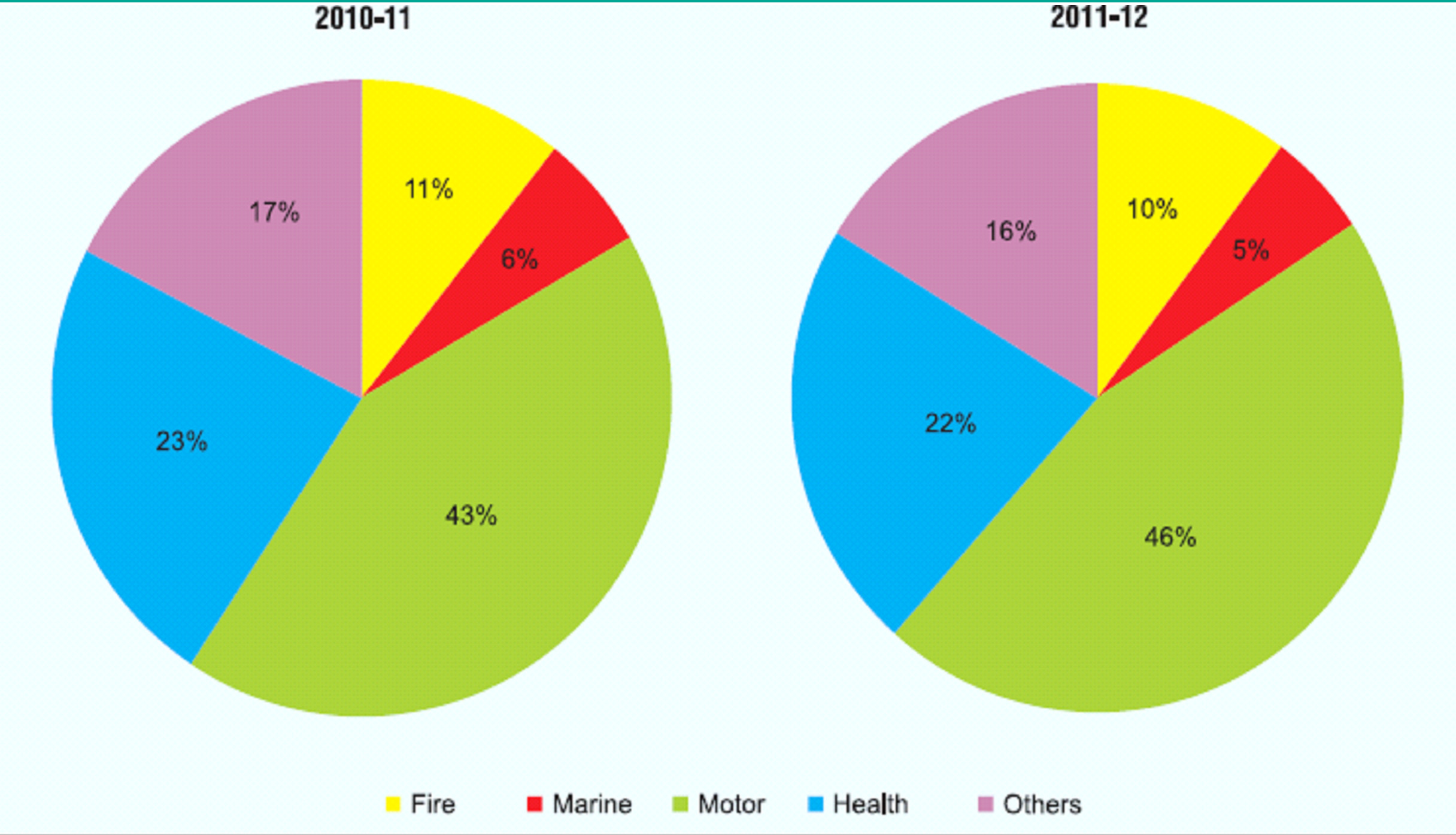

The Motor Vehicles Act, 1988, under section 146 mandates that every vehicle should be compulsorily insured for third party risk. The reason is because of the growing number of accidents that causes fatalities and disability among the victims. The objective of such insurance policies is to help the victims and the legal representatives of the deceased victims to secure substantial compensation. The compensation can be obtained only if the motor vehicle that was involved in the accident is insured. If the vehicles are not insured, then recovery of the compensation is a distinct possibility. For this reason, vehicle insurance benefits both the accident victims as well as the vehicle owners as they are saved of paying any compensation out of their pocket. In terms of ticket size, Motor is the biggest portfolio of non-life insurers:

The Motor Vehicles Act, 1988, under section 146 mandates that every vehicle should be compulsorily insured for third party risk. The reason is because of the growing number of accidents that causes fatalities and disability among the victims. The objective of such insurance policies is to help the victims and the legal representatives of the deceased victims to secure substantial compensation. The compensation can be obtained only if the motor vehicle that was involved in the accident is insured. If the vehicles are not insured, then recovery of the compensation is a distinct possibility. For this reason, vehicle insurance benefits both the accident victims as well as the vehicle owners as they are saved of paying any compensation out of their pocket. In terms of ticket size, Motor is the biggest portfolio of non-life insurers:

There is a differential pricing in motor insurance, and usage of the vehicle on roads and occupation are becoming important factors in determining it. Gender also has a role to play.. That’s because women are considered safer drivers and less rash on roads than their male counterparts. As the Indian passenger vehicle market moves decisively towards diesel, the shift is leaving its mark on motor insurance premia as well. The premia differential between petrol and diesel vehicles has shot up to 20-22% in certain categories with insurers claiming higher usage, pricier spare parts and steeper maintenance costs as the reason for the higher insurance premium.

There is a differential pricing in motor insurance, and usage of the vehicle on roads and occupation are becoming important factors in determining it. Gender also has a role to play.. That’s because women are considered safer drivers and less rash on roads than their male counterparts. As the Indian passenger vehicle market moves decisively towards diesel, the shift is leaving its mark on motor insurance premia as well. The premia differential between petrol and diesel vehicles has shot up to 20-22% in certain categories with insurers claiming higher usage, pricier spare parts and steeper maintenance costs as the reason for the higher insurance premium.

WHY VEHICLES ARE UNINSURED?

Motor insurance is mandatory as per the provisions of the Motor Vehicles Act 1988. So if your motor vehicle insurance policy has expired or if you have forgotten to renew your policy, it implies that you and your vehicle are not covered under insurance and your insurance company is not liable to pay any claims arising out of accident. Moreover, driving an uninsured vehicle in any public space is illegal under the said Act. In addition, your No Claims Bonus (NCB) will also be forfeited, if the policy is not renewed on time. Usually most insurance companies send a renewal notice well in advance of policy expiry date. With advancement in technology, you can also set your own car insurance renewal reminder through online alerts, mobile alerts etc. In case your car insurance policy has expired or if you have not renewed your car insurance policy on time, then you can approach your existing insurance company or your dealer / agent to renew your policy. You can also approach another insurance company for your car insurance, however, you need to fill in a fresh proposal form and the new insurer may ask for a physical inspection of your vehicle in case of a break. Insurance companies may apply additional loading on premium if policy has expired 30/45 days earlier or in view of bad claim history.EFFORT TO CURB THE MENACE:

The Supreme Court and the high courts had passed many directions asking the government to implement the Motor Vehicles Act. In 2009, the police commissioner assured the Delhi High Court to strictly comply with the rules under the Motor Vehicles Act. Meanwhile, according to the Insurance Information Bureau (IIB), there are a large number of uninsured vehicles on the Indian roads. Less than 40 million vehicles, out of the total 120 million automobiles and two-wheelers on Indian roads, had any form of insurance cover in the year 2009-10, according to IIB. The insurers are also experiencing higher claim incidence from the more popular small cars, as compared to bigger automobiles. The increase in the claim ratio to 70-80 per cent is attributed to the expensive spare parts and imported components in small cars. Moreover, the higher comparative use of small cars has increased the probability of their accidents. The Delhi High has asked the Centre, Delhi government and Delhi police to respond to a plea against allowing uninsured vehicles to ply on roads. The bench was hearing a Public Interest Litigation (PIL) seeking directions to authorities to “effectively” implement the provisions of Motor Vehicles Act 1988. The petition alleged the authorities deliberately neglect the provisions of the Act and do not prosecute the owner or driver for plying uninsured vehicles. The respondents permit the uninsured vehicles to ply on the road in breach of law and thereafter neither prosecute the owner or driver nor seize or auction the offending vehicle. The petition also sought directions to compensate the road mishap victims, suffering losses due to non-implementation of the MV Act. The PIL was filed by the family members of a 48-year-old man, Dinesh Sehgal, who died in a road accident when he was hit by an uninsured tractor. Sehgal’s family has sought compensation for his death. The family asked the court to direct respondents to explain measures adopted by them since 2009 to curb the menace of uninsured vehicles on roads. The plea urged the court to ask the respondents “to explain the measures adopted by them since 2009 to curb the menace of uninsured vehicles plying on road, drivers without valid driving license, fake driving licenses and drunken driving”.REFUSAL OF THIRD PARTY INSURANCE:

Insurance regulator had declared “severe” penal action against those general insurance companies refusing third party motor insurance. Some companies are declining third party insurance. They will find it not in their best interest to do so because if companies do not abide by the rules the IRDA has laid down, such companies will be visited by very severe penalties which will be more onerous than the business they are foregone. Third party motor insurance provides cover mainly pedestrians, fare-paying and non fare paying passengers in a vehicle. Private sector insurers try to avoid writing such policies because of the high claim ratio in the commercial vehicle space. This leads to the public sector companies being hit the most. Recently, IRDA came out with guidelines for implementation of declined risk pool system. The regulator has laid down a method for transferring risks to the newly formed declined risk pool for third-party motor policies. As per the guidelines, the declined risk pool would apply to commercial vehicles for standalone third-party liability insurance and no comprehensive motor insurance policy can be settled from the pool. The size of the pool is likely to shrink to a quarter because of the comprehensive policy going out of the ambit of the pool.INNOVATIVE MOTOR COVERS:

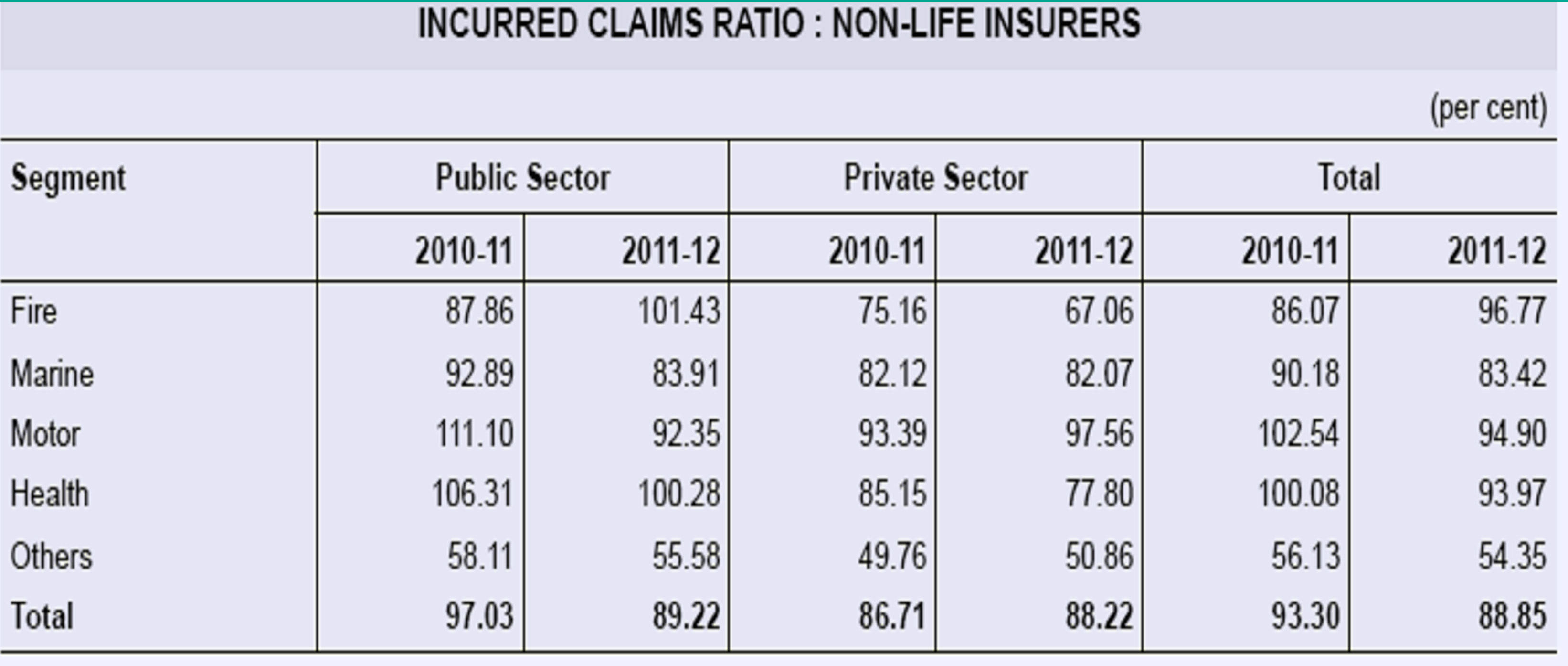

Insurance companies are bringing about innovations in covers for commercial vehicles after the regulator discontinued a system where losses on this segment had to be shared proportionately by all companies. Insurers are suddenly finding the need to innovate to gain more experience of the commercial vehicle segment following dismantling the ‘third-party pool’ earlier this year. The innovations include zero-depreciation policies, hitherto restricted to cars, and value-added policies. Insurance companies are trying to get a better experience of commercial vehicle business as they have been ignoring this business for the last five years. Insurers have been writing all kinds of proposals as the losses get shared. Private insurers have devised a value-added cover for commercial vehicles where they will get compensation for towing charges and transfer of goods from an accident vehicle to another one. A PSU company is also looking at bringing in value-added, zero-depreciation ‘own-damage’ policies for commercial vehicles. Zero-depreciation policies are those that settle repair claims in full without deductions and have been a big hit among car owners. The declined risk pool forces insurers to issue third-party insurance covers to commercial vehicles in proportion to their size. If they fall short, they will have to take on policies in the ‘declined pool’ which are essential vehicles that no insurer covers voluntarily. Motor insurance has the highest incurred claim ratio among all segments:

Not only should the vehicle be covered by a valid insurance but should also be driven by a person who has a valid license. In the case of commercial vehicles, validity of permit and fitness should be observed. Pricing in motor insurance has gone in for a sea change in the last five years. Prior to de-tariffing (where prices are market-driven) in 2007, the main factors governing motor insurance premium pricing was the year of manufacture of the vehicle, engine capacity, price and the zone in which the vehicle was bought. While these four factors continue to play a role in determining the insurance premium, other factors such as occupation are also playing an important role in determining the pricing of the motor cover. Insurers are seeing the emergence of differential premium pricing with respect to profession. Insurers are giving positive rating for some professions. This is translating to a discount of 5% on tariff premiums. Motor premiums contribute to nearly 40% of general insurance premium collected by insurers. The contribution of motor is significant to a company’s top line as well as bottom line. This has resulted in a lot of pricing sophistication in this line of business. A lot of segmentation is happening in the motor insurance space. Companies want to have a profitable set of customer. They are doing so by loading customers who are bound to give more losses and discounts to people who are giving profits. The segment wise premium position of general insurers was as follow:

Segment wise non-life premium

The Motor Vehicles Act, 1988, under section 146 mandates that every vehicle should be compulsorily insured for third party risk. The reason is because of the growing number of accidents that causes fatalities and disability among the victims. The objective of such insurance policies is to help the victims and the legal representatives of the deceased victims to secure substantial compensation. The compensation can be obtained only if the motor vehicle that was involved in the accident is insured. If the vehicles are not insured, then recovery of the compensation is a distinct possibility. For this reason, vehicle insurance benefits both the accident victims as well as the vehicle owners as they are saved of paying any compensation out of their pocket. In terms of ticket size, Motor is the biggest portfolio of non-life insurers:

There is a differential pricing in motor insurance, and usage of the vehicle on roads and occupation are becoming important factors in determining it. Gender also has a role to play.. That’s because women are considered safer drivers and less rash on roads than their male counterparts. As the Indian passenger vehicle market moves decisively towards diesel, the shift is leaving its mark on motor insurance premia as well. The premia differential between petrol and diesel vehicles has shot up to 20-22% in certain categories with insurers claiming higher usage, pricier spare parts and steeper maintenance costs as the reason for the higher insurance premium.

UNINSURED Vs. UNDERINSURED:

This trend in the percentage of uninsured motorists is an unfortunate consequence of the economic downturn. This results in owners with insurance bearing the burden of paying for injuries caused by drivers’ not carrying insurance. In addition to uninsured vehicles, many drivers also carry the state statutory minimum coverage limit under Workmen’s Compensation Act, which doesn’t cover much with today’s cost of healthcare. When you file an uninsured motorist claim, your insurance company’s interests can be adverse to your interests. However underinsured means insured for less than the market value. In India, the concept of “Insured’s Declared Value” (IDV) is applicable for first five years for each category of vehicles. Thereafter the value of the vehicle is decided mutually by the insured and the insurer according to the condition of the vehicle. In case of under insurance the policyholder may suffer the loss at the time of Theft/Total loss. Though the provision of “Average Clause” is not applicable in the motor insurance, however it is in the interest of the insured that the vehicle is insured for the IEV/Market value. The IDV is the market value of the vehicle. The higher the value, the greater the premium. You can save a few hundred rupees on your premium by declaring a lower value for your car. If your car is worth 7 lakh, declaring a value of 6.3 lakh could help you save 200-500 on insurance premium. This is a double-edged sword as the claim amount for accidents will not be affected by declaring a lower IDV. However, if your car is stolen, you will get a lower amount in line with the one declared by you.KEEPING TAB ON UNINSURED VEHICLES:

The General Insurance Council along with general insurers is working on establishing a Motor Insurance Bureau (MIB). It will keep track of vehicles that do not renew their third-party insurance, mandatory under the law. This data will be shared with all insurers so that they can approach the vehicle owners and have them covered. The database will also be shared with local police authorities as well as regional transport authorities so that they can take appropriate steps, in case they ply uninsured. Third party insurance covers accident victims other than the vehicle owners and its passengers during an accident. There are some 12 crore vehicles in India of which at least 3 crore ply uninsured, meaning one in every four vehicle do not renew their policies. The General Insurance Council is a representative body of all general insurers in India. General Insurance Council will work towards creating a central database of all registered vehicles and keep a tab on whether they renew their covers – both third party and own-damage. To start with, the Council will collate a list of all vehicles that are insured during a particular year. In the subsequent years they will compare the data with the ones that renew their cover, the ones that do not can thus be find out. The Council is looking at ways and means of collating the data, since all insurers will have to share details of third party policies sold, with the MIB. Interestingly, UK also has a similar MIB that works towards keeping all vehicles covered. Although UK is a fairly developed market, but according to the MIB there are about 9 lakh drivers under the age of 30 are currently driving without insurance. As much as 60% of drivers think they are likely to be caught and only 7% are aware of all the possible consequences when they are caught. The MIB data in Britain helps police detect uninsured drivers and is used by the police to seize about 500 vehicles a day. In India, the MIB may collaborate with vehicle manufacturers to track them. Additionally, a couple of private agencies are also trying to collate such data. The MIB may collaborate with them. Currently authorities can do little to find out if a registered vehicle plying on the road is covered with a third party insurance other than manually checking each vehicle. For Indian insurers, such data will help in two ways. They will have access to the claim history of vehicles. It will help in proper risk profiling and charge the right premium. Insurers will also be able to approach owners of uninsured vehicles. It may, however, not be possible to include existing uninsured vehicles in the first year when the database is created since they will remain uninsured. But we will be able to track all those who insure at least ones after the Bureau is formed. Nevertheless, a vehicle which never comes up for insurance may remain out of this database. There are instances, mainly, in rural India where vehicles are never insured.HOW TO VAN UNINSURED VEHICLES:

One out of every three vehicles on Indian roads does not have the mandatory third-party liability insurance, let alone personal cover. The laws on accident claims are quite stringent. The laws were formulated by prioritizing the best interests of the victims and those who are liable to disburse the compensation, such as insurance companies. Indian laws on motor vehicle accident claims are strict but beneficial for victims in claiming their legal rights in a court of law. Police/Traffic authorities are empowered to challan the uninsured vehicles. They have got the Interceptor system to check the speed and traffic violations. The Fatal Accidents Act, 1885 was enacted in India to protect the legal rights of the accident victims and their legal heirs. This Act entitles the legal heirs of a deceased accident victim to claim compensation from the person who committed negligence. The General Insurance Corporation (GIC), the national re-insurer that manages the ‘Indian market terrorism risk insurance pool’, has proposed a penalty for Indian companies proposing to switch to Indian insurers from insurers abroad. The penalty shall be equivalent to three years difference in the premium at the current pool rate and the rate charged by the overseas reinsurer.INDIAN LAW ON MANDATORY INSURANCE OF VEHICLES:

Indian law on accident claims is relevant due to the higher rates of accidents leading to loss of life and property across the country. In 1988, the Government of India introduced the Motor Vehicle Act, to make the Indian laws on accident claims more effective. The Act provides for compulsory third party insurance and procedure of adjudication, to ensure relief to victims of accident cases. Also, the Act stipulates for establishment of Motor Accident Claims Tribunal to address the accident claim cases. This means that if you are a victim of a motor vehicle accident, your first point of reference to press for a claim is at the aforementioned tribunal that has been established to address similar claims. Sec 196 of the Motor Vehicle Act says: “Whoever drives a motor vehicle or causes or allows a motor vehicle to be driven in contravention of the provisions of section 146 shall be punishable with imprisonment which may extend to three months, or with fine which may extend to one thousand rupees, or with both.” Means Auto Insurance in India is a compulsory requirement for all vehicles used whether for commercial or personal use. The Motor Vehicles Act does not make any distinction between private and government vehicle in the matter of mandatory insurance. The Indian Road rules, titled “Rules of the Road Regulation”, were brought into effect since July, 1989. These rules are germane to the Indian drivers (all inclusive of two, three and four wheelers), while on the road to ensure an orderly traffic and a safer journey. Violation of these “Rules of Road Regulation” is a punishable transgression as per the city specific traffic police rules and the “Motor Vehicle Act”. Enforcement of these traffic laws – rules, regulations and acts can bear out the road accidents. These laws are enforced by issuing challans in the name of the offenders and teaching them a lesson by making them pay penalties. These are: RRR: Rules of Road Regulations 1989 MVA: Motor Vehicles Act 1988 CMVR: Central Motor Vehicles Rules 1989A MAJOR PROBLEM IN UK:

Millions of UK motorists have run the risk of penalty points, a fine or a driving ban after driving without insurance, the latest research by LV= has revealed. The survey found that 2.2 million motorists have driven without insurance, with the majority (1.8 million) mistakenly believing they were insured at the time. The number of motorists borrowing cars rose by 14% last year despite facing fines of up to £5,000 if caught by the police, up to eight points on their license and, in some circumstances, an instant driving ban. According to official police data obtained under a freedom of information request from LV= car insurance, 22,000 drivers have been caught using a vehicle that was uninsured and been awarded penalty points in the past six months, yet this is just the tip of the iceberg as motorists driving friends’ or relatives’ cars without insurance goes mostly undetected. One in six (18%) motorists have lent their car to someone else and, of these, almost a fifth (19%) believed a valid insurance was in place when there wasn’t, and a further 4% did not care that the driver was not insured. Almost half (47%) of car lenders who are committing a crime by lending their car to an uninsured driver say they lend their vehicle at least once a month. Of these, a quarter (28%) lends their car to an uninsured son or daughter, and 15% to a flat mate. About four in 10 (44%) drivers say they would lend their car to a friend who is not insured to drive it, regardless of the law. Thousands of motorists lend their cars to others and don’t realize they are not insured to drive them. If someone has driven your car without insurance, and with your permission, you could face a fine and up to eight points for permitting a vehicle to be on a public road without an insurance policy being in force. The root of the problem is that many drivers assume that by having comprehensive insurance on their own vehicle, they are automatically covered to drive other vehicles – but this is not always the case. Some policies offer no cover at all, some offer third party only, meaning in the event of an accident where the car borrower was at fault there would be no payment for any damage to the vehicle. Diesel vehicles have always commanded higher motor insurance premium and the differential between petrol and diesel variants has traditionally been around 10-15%. But with diesel vehicles ruling the auto mart, that differential has been on the rise. With the arrival of new diesel models in the last couple of years, especially in the hatch back and mid size segments, this (difference) has now moved up to 20% to 22% in the case of certain vehicles. In case of some models and in certain geographies, the premium differential can move up to 20%. Since diesel cars have higher usage and the cost of spare parts is higher than their petrol counterparts, this is reflected in the premium pricing. Diesel cars have higher claims ratio than petrol vehicles. While buying a new car, customers are bound to have been pulled in by the bevy of discounts and freebies. One of the most attractive among these is the offer of free insurance. Since buying a car insurance policy is compulsory, the word ‘free’ pulls in buyers, but there could be hidden clauses. The first catch is that the insurance provided is typically only for a year. From the second year on, it’s buyer’s responsibility to renew the policy and pay the premium. Moreover, free insurance would mean a lower discount on the price of the car as dealers invariably recover the premium through the final cost that payble for the vehicle. Besides, the free policy may not include various types of damages, such as that by floods. So, read the fine print carefully before taking this bait, or opt for a higher discount on the car and buy an insurance policy separately. Find out how due diligence and research can help reduce the insurance premium to pay for the first year as well as subsequently. Although monoline motor insurance companies have not made their presence in India even after the sector was opened up a decade ago, slow growth of property insurances has willy-nilly turned a few companies into predominantly auto insurers. According to data published by the life insurance regulator, three companies – Royal Sundaram General Insurance, Bharti Axa General Insurance and Shriram General Insurance – have more than 70% of their business coming from motor insurance, making them close to monoline companies. Monoline companies are those with a general insurance license but choose to focus on one line of business. Although there are specialist health insurers, this is a separate licence category. Going by current trends some insurers might end up becoming monline companies. Monoline companies are seen as being good for a line of activity since their specialization helps drive innovation. Although bulk of auto insurance in the private sector is still with larger companies such as ICICI Lombard and Bajaj Allianz, the share of motor in their overall business is lower. The Bharti Axa General Insurance, the company did not start out as a predominantly motor business. The motor business is losing less money than other businesses and is also one line that is growing fast. As of March 2012, over 71% of Bharti Axa’s total premium came from motor insurance, followed by health and other businesses. Given the continued demand for cars, road transportation of people and goods and growth of automobile sector, motor insurance segment will continue to grow. But at the same time, other branches of non-life are expected to do well as prices have started to harden. One reason why such a large number of vehicles remain uninsured is the proliferation of fake policies. Several non-life companies have come across fake policies issued in their name. With advancement in printing technology, it is possible for fraudsters to replicate policies of existing companies, helping them get through police checks. However, it is at the time of accident and claims from third parties that insurers detect the existence of fake policies. Second, vehicle owners in small cities and villages do not face any scrutiny of their documents. An uninsured vehicle is one of the structural issues faced by the non-life industry in writing motor-third party insurance, which is a drag on the balance sheet of non-life companies. The other issues were rigid prices and the tendency of court awards to go up in keeping with inflation. The premium falls with each passing year due to two reasons: reduced IDV and accumulated NCB. Besides, the value of your vehicle will decline each year because of depreciation, and a lower market value automatically translates to a lower premium. However, at the time of a partial damage claim, this depreciation factor kicks in, reducing the claim amount that is payable by the company. The sales of automobiles have maintained a robust growth, in double digits, even when the economic growth is apparently slowing down. Secondly, the third party insurance in automobiles is compulsory and mandated by law. Moreover, in recent years there have been increases in the third party premium. Lastly, post de-tariffication, pricing in property insurances has witnessed steady fall by way of discounting, resulting only in its modest growth. In the case of private cars, the industry is witnessing a claims ratio of 65-70%. This means that margins are very thin after providing for management costs. However, chances of catastrophic losses are lower and the business is less cyclic. To manage profitable motor portfolio insurers, General Insurance Council and the Regulator should make combined efforts by insuring the uninsured vehicles plying on the road and causing loss of life and property to the Nation.Author : JAGENDRA KUMAR

Published : The Insurance Times Magazine – February 2013

Leave a Reply