HAS TRUST IN INSURANCE COMPANIES REACHED A PEAK UNDER IRDAI’s LEADERSHIP?

EASE OF DOING BUSINESS:

Insurance Laws (Amendment) Act, 2015 provides for enhancement of the Foreign Investment Cap in an Indian Insurance Company from 26% to an Explicitly Composite Limit of 49% with the safeguard of Indian Ownership and Control. Insurance penetration of India i.e. Premium collected by Indian insurers is 3.44% of GDP in FY 2015-16. Per capita premium underwritten i.e. insurance density in India during FY 2015-16 is US$ 54.7. The reasons that the insurance sector in India is under-penetrated and inadequately penetrated are: lack of awareness, low level of financial inclusion, and lack of trust in the system. In addition, the support system is over-regulated and cost of compliance is high. Regulations are about input policing rather than being outcome-based. The essential and pre-requisite “Ease of Doing Business” framework has not been installed with vigour. The approach to public accountability is hesitant and tentative, and the level playing field imperative does not prevent a government entity from getting preferential treatment. The Indian insurance industry too has contributed to the current intrusive ‘rule based’ regulatory mechanisms. Insurance business has not been very successful in creating value, delivering returns below the cost of capital for years. The non-life insurance industry has the highest combined ratio across developed and emerging countries, almost for the last 15 years. What one observes is that ‘poor market conduct’ leads to even more intrusive regulations – with the one feeding the other in a circular movement. The Indian insurance market though feels redeemed with the top lines and the gross premium increases, the growing number of policies across life/non-life sectors, and the investment-led rather than underwriting-led profits. Digitisation of the databases of insurance companies, linking of insurance policies with personal identifiers such as Aadhaar, vehicle registration numbers etc. contribute to the growth. Technology is another tool that companies are betting on to lift their fortunes. Today motor, health and travel insurance policies are sold online. Policies are sold online or through agents, manufacturers and banks. But online sales are merely 3% compared to 30% in the US and UK. Disruption will come in the industry with companies focusing on pure online distribution.

EASE OF DOING BUSINESS:

Insurance Laws (Amendment) Act, 2015 provides for enhancement of the Foreign Investment Cap in an Indian Insurance Company from 26% to an Explicitly Composite Limit of 49% with the safeguard of Indian Ownership and Control. Insurance penetration of India i.e. Premium collected by Indian insurers is 3.44% of GDP in FY 2015-16. Per capita premium underwritten i.e. insurance density in India during FY 2015-16 is US$ 54.7. The reasons that the insurance sector in India is under-penetrated and inadequately penetrated are: lack of awareness, low level of financial inclusion, and lack of trust in the system. In addition, the support system is over-regulated and cost of compliance is high. Regulations are about input policing rather than being outcome-based. The essential and pre-requisite “Ease of Doing Business” framework has not been installed with vigour. The approach to public accountability is hesitant and tentative, and the level playing field imperative does not prevent a government entity from getting preferential treatment. The Indian insurance industry too has contributed to the current intrusive ‘rule based’ regulatory mechanisms. Insurance business has not been very successful in creating value, delivering returns below the cost of capital for years. The non-life insurance industry has the highest combined ratio across developed and emerging countries, almost for the last 15 years. What one observes is that ‘poor market conduct’ leads to even more intrusive regulations – with the one feeding the other in a circular movement. The Indian insurance market though feels redeemed with the top lines and the gross premium increases, the growing number of policies across life/non-life sectors, and the investment-led rather than underwriting-led profits. Digitisation of the databases of insurance companies, linking of insurance policies with personal identifiers such as Aadhaar, vehicle registration numbers etc. contribute to the growth. Technology is another tool that companies are betting on to lift their fortunes. Today motor, health and travel insurance policies are sold online. Policies are sold online or through agents, manufacturers and banks. But online sales are merely 3% compared to 30% in the US and UK. Disruption will come in the industry with companies focusing on pure online distribution.

PROTECTION OF POLICYHOLDER’S INTEREST:

In the 17 years since the private sector general insurance companies were permitted to write policies, hardly anything changed for nearly a decade. Almost every company was reporting losses because of controlled pricing and the way claims were settled. But that may change for the better. New companies that are coming in will have very little to destabilise market dynamics when the industry is at Rs 1.25 lakh crore. Business means fulfilling customer’s requirements. Companies that have the greater number of satisfied customers are more successful. Satisfying the customers with all the queries and solving all their issues ensures a healthy growth to any company. And a growth of unsatisfied customers is the sure indication of the closure of a business. The ‘IRDAI Protection of Policyholders’ Interests Regulations 2017 ensure that “Every insurer shall display the service parameters and turnaround times as approved by the board on its website and keep the same updated as and when the service parameters are revised by the board.” With the prevalence of employer-paid health insurance, IRDAI now insists that the policy document mention upfront co-payer limits if the policy is co-paid by the employees. Insurers are also now required to update on their website the terms and conditions of every insurance product that is withdrawn or modified. And update the list at frequent intervals. The Indian general insurance industry, which generates an annual premium of Rs 1.27 lakh crore, is still dominated by the public sector companies, but the likes of ICICI Lombard, Bajaj Allianz General Insurance and HDFC Ergo have made strides with advancing market share. It is ranked 18th among 88 nations. Stars are aligning for the business to get more profitable now than in the past – be it technology or the changes in regulations, including the provisions of the Motor Vehicles Act, and the improving data availability with the information bureau helping to eliminate frauds. It all changed in 2007 when the insurance regulator brought in the detariffication policy, except for third party motor insurance where the regulator retains price control.

PRODUCT INNOVATION:

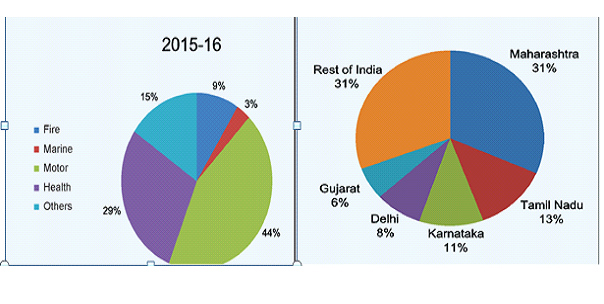

While several products were add-ons to the existing policies, most new policies were in crop insurance and motor insurance. In the current financial year, about 70 new products, including add-ons, have been launched in the general insurance segment, according to the IRDAI. While several products were add-ons to the existing policies, most new policies were in crop insurance and motor insurance. General insurance sector have already received Rs 10,000-12,000 crore from crop insurance and premiums is likely to touch Rs 18,000-20,000 crore by the end of current financial year. In the first year itself, industry is expecting to get Rs 20,000 crore through crop insurance and premiums are likely to grow in the coming year. It’s one of the new segments that general insurance industry is focusing on. Even long-term two wheeler policies were filed by various insurers. This segment has seen premium in the range of Rs 300-500 crore. Industry as, of 1.72 lakh complaints in 2016-17, about 50 per cent related to unfair business practices, according to IRDAI’s consumer booklet 2016-17. Many a time, exclusions are lost in a maze of fine print. But the IRDAI has now said that the terms and conditions for claims, renewals have to be bifurcated. So that customers exactly know the coverage limits of their policy. An important addition pertinent to policyholders is the regulator’s insistence that the insurer mentions service parameters or turnaround time. Now the regulator is trying to increase accountability by insisting they put up on their website the average servicing time taken for services -as approved by their board. The spread of general insurance business in 2015-16 was as follow:

PROTECTION OF POLICYHOLDER’S INTEREST:

In the 17 years since the private sector general insurance companies were permitted to write policies, hardly anything changed for nearly a decade. Almost every company was reporting losses because of controlled pricing and the way claims were settled. But that may change for the better. New companies that are coming in will have very little to destabilise market dynamics when the industry is at Rs 1.25 lakh crore. Business means fulfilling customer’s requirements. Companies that have the greater number of satisfied customers are more successful. Satisfying the customers with all the queries and solving all their issues ensures a healthy growth to any company. And a growth of unsatisfied customers is the sure indication of the closure of a business. The ‘IRDAI Protection of Policyholders’ Interests Regulations 2017 ensure that “Every insurer shall display the service parameters and turnaround times as approved by the board on its website and keep the same updated as and when the service parameters are revised by the board.” With the prevalence of employer-paid health insurance, IRDAI now insists that the policy document mention upfront co-payer limits if the policy is co-paid by the employees. Insurers are also now required to update on their website the terms and conditions of every insurance product that is withdrawn or modified. And update the list at frequent intervals. The Indian general insurance industry, which generates an annual premium of Rs 1.27 lakh crore, is still dominated by the public sector companies, but the likes of ICICI Lombard, Bajaj Allianz General Insurance and HDFC Ergo have made strides with advancing market share. It is ranked 18th among 88 nations. Stars are aligning for the business to get more profitable now than in the past – be it technology or the changes in regulations, including the provisions of the Motor Vehicles Act, and the improving data availability with the information bureau helping to eliminate frauds. It all changed in 2007 when the insurance regulator brought in the detariffication policy, except for third party motor insurance where the regulator retains price control.

PRODUCT INNOVATION:

While several products were add-ons to the existing policies, most new policies were in crop insurance and motor insurance. In the current financial year, about 70 new products, including add-ons, have been launched in the general insurance segment, according to the IRDAI. While several products were add-ons to the existing policies, most new policies were in crop insurance and motor insurance. General insurance sector have already received Rs 10,000-12,000 crore from crop insurance and premiums is likely to touch Rs 18,000-20,000 crore by the end of current financial year. In the first year itself, industry is expecting to get Rs 20,000 crore through crop insurance and premiums are likely to grow in the coming year. It’s one of the new segments that general insurance industry is focusing on. Even long-term two wheeler policies were filed by various insurers. This segment has seen premium in the range of Rs 300-500 crore. Industry as, of 1.72 lakh complaints in 2016-17, about 50 per cent related to unfair business practices, according to IRDAI’s consumer booklet 2016-17. Many a time, exclusions are lost in a maze of fine print. But the IRDAI has now said that the terms and conditions for claims, renewals have to be bifurcated. So that customers exactly know the coverage limits of their policy. An important addition pertinent to policyholders is the regulator’s insistence that the insurer mentions service parameters or turnaround time. Now the regulator is trying to increase accountability by insisting they put up on their website the average servicing time taken for services -as approved by their board. The spread of general insurance business in 2015-16 was as follow:

CLAIM SETTLEMENT:

Motor and health, which constitutes 65-70% of the industry, has always been the Achilles heel for the general insurance industry. It is beset with losses in the third party motor segment, which is 35% of the industry losses. Many customers only realise at the time of making a claim that their health insurance policy does not cover certain medical conditions or ailment. Policyholders usually depend on what has been told to them by their insurance agents, who sometimes overstate the coverage. To prevent such cases, the IRDAI have asked insurers to group together all policy exclusions upfront in the policy document. Another change with the new regulation is the introduction of penal interest. If the customer is not paid the claim within 90 days of reporting, the insurer has to pay the bank rate + 2 per cent interest for every day of further delay. Often, there is a delay in the settlement of claims. It could be a three-month or six-month delay, or more. And the insurer’s lethargy over the claim would be made known to the public only when IRDAI publishes its annual report. Multiple indemnity policies having identical coverage does not benefit the policyholder, ideally coverage in multiple policies should be mutually exclusive. When buying multiple benefit policies it is important that the second insurer is made aware of the existence of the first policy as that forms a crucial part of underwriting. The health insurance policies such as Mediclaim are indemnity covers i.e. only the hospital bills get reimbursed up to the sum insured of a policy. The other variant of health insurance policies are the defined-benefit policies i.e. the entire sum insured gets paid on the occurrence of the defined ailment irrespective of the hospital bills. For the past couple of years, insurance companies have been sharing data to detect frauds in the system. They have tied up with LexisNexis and Experian to collate database on frauds. Accordingly, they are training claims assessors to document claims decisions and have proper evidence on record to repudiate such frauds. Insurers have blacklisted around 70 locations to prevent fraudulent claims.

SOLVENCY OF INSURANCE COMPANIES:

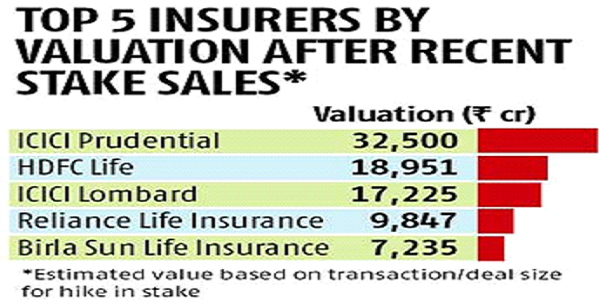

A likely era of consolidation begins in the insurance sector with board approval for merger of Max Financial Services and Max Life with HDFC Life. The second such deal this month; earlier, it was announced that L&T General would merge into HDFC ERGO General Insurance (a Rs 551 crore deal). HDFC Ergo bought L&T General Insurance at the price to book of 1.8 times in June last year. Fairfax Financial Holding had bought a 9% stake in ICICI Lombard General Insurance at the price to book of 5.7 times in October 2015. Participants in the market also say this offering would hit market only in next financial year.

CLAIM SETTLEMENT:

Motor and health, which constitutes 65-70% of the industry, has always been the Achilles heel for the general insurance industry. It is beset with losses in the third party motor segment, which is 35% of the industry losses. Many customers only realise at the time of making a claim that their health insurance policy does not cover certain medical conditions or ailment. Policyholders usually depend on what has been told to them by their insurance agents, who sometimes overstate the coverage. To prevent such cases, the IRDAI have asked insurers to group together all policy exclusions upfront in the policy document. Another change with the new regulation is the introduction of penal interest. If the customer is not paid the claim within 90 days of reporting, the insurer has to pay the bank rate + 2 per cent interest for every day of further delay. Often, there is a delay in the settlement of claims. It could be a three-month or six-month delay, or more. And the insurer’s lethargy over the claim would be made known to the public only when IRDAI publishes its annual report. Multiple indemnity policies having identical coverage does not benefit the policyholder, ideally coverage in multiple policies should be mutually exclusive. When buying multiple benefit policies it is important that the second insurer is made aware of the existence of the first policy as that forms a crucial part of underwriting. The health insurance policies such as Mediclaim are indemnity covers i.e. only the hospital bills get reimbursed up to the sum insured of a policy. The other variant of health insurance policies are the defined-benefit policies i.e. the entire sum insured gets paid on the occurrence of the defined ailment irrespective of the hospital bills. For the past couple of years, insurance companies have been sharing data to detect frauds in the system. They have tied up with LexisNexis and Experian to collate database on frauds. Accordingly, they are training claims assessors to document claims decisions and have proper evidence on record to repudiate such frauds. Insurers have blacklisted around 70 locations to prevent fraudulent claims.

SOLVENCY OF INSURANCE COMPANIES:

A likely era of consolidation begins in the insurance sector with board approval for merger of Max Financial Services and Max Life with HDFC Life. The second such deal this month; earlier, it was announced that L&T General would merge into HDFC ERGO General Insurance (a Rs 551 crore deal). HDFC Ergo bought L&T General Insurance at the price to book of 1.8 times in June last year. Fairfax Financial Holding had bought a 9% stake in ICICI Lombard General Insurance at the price to book of 5.7 times in October 2015. Participants in the market also say this offering would hit market only in next financial year.

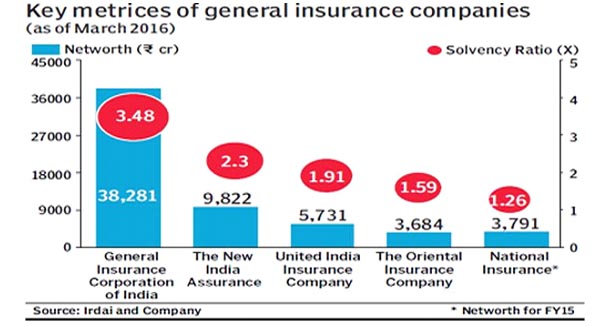

The Cabinet Committee on Economic Affairs (CCEA) approved listing of five state-owned general insurance companies, thus paving the way for reducing the government’s stake in these insurers from 100% to 75%. It is expected that a price-to-book multiple of anywhere between 1.2 and 1.5 times while offering their shares to the public. The government can raise anywhere between R18,400 and R23,000 crore by offloading its 25% stake in these five companies. This is the base case scenario and the government might be able to raise more money if the market is conducive. New India Assurance Company, United India Insurance, Oriental Insurance Company, National Insurance Company and GIC Re will list on stock exchanges. Even solvency ratios have not been encouraging if compared to other private insurers. According to the data from IRDAI, solvency ratio of National Insurance is 1.26% and 1.59% for Oriental Insurance as on March 2016. But New India Assurance has one of the highest solvency ratio of 2.3% among large general insures in India. It is the board’s decision, but it is very unlikely that some foreigner will buy the stake in the four companies. Yes they can participate in the IPO and can invest, but stake sale is very unlikely.

The Cabinet Committee on Economic Affairs (CCEA) approved listing of five state-owned general insurance companies, thus paving the way for reducing the government’s stake in these insurers from 100% to 75%. It is expected that a price-to-book multiple of anywhere between 1.2 and 1.5 times while offering their shares to the public. The government can raise anywhere between R18,400 and R23,000 crore by offloading its 25% stake in these five companies. This is the base case scenario and the government might be able to raise more money if the market is conducive. New India Assurance Company, United India Insurance, Oriental Insurance Company, National Insurance Company and GIC Re will list on stock exchanges. Even solvency ratios have not been encouraging if compared to other private insurers. According to the data from IRDAI, solvency ratio of National Insurance is 1.26% and 1.59% for Oriental Insurance as on March 2016. But New India Assurance has one of the highest solvency ratio of 2.3% among large general insures in India. It is the board’s decision, but it is very unlikely that some foreigner will buy the stake in the four companies. Yes they can participate in the IPO and can invest, but stake sale is very unlikely.

PUBLIC AWARENESS:

The IRDAI makes use of various platforms like newspapers, television, radio and outdoor publicity to create awareness about importance of insurance. IRDAI had a budget of Rs 60 crore towards advertisement, but only an estimated Rs 24 crore, or 40 per cent, was spent. Unable to spend even 50 per cent of earmarked funds for insurance awareness last fiscal, the Regulator is looking for innovative methods to utilise this year’s advertisement budget that has been raised to Rs 66.5 crore. The government is keen on increasing insurance penetration in the country, especially in remote areas. The advertisement for consumer affairs department of IRDAI for 2017-18 has been budgeted at Rs 66.50 crore. While increasing the budget for the current financial year, the regulator is “planning for more advertisement”. Towards this purpose, IRDAI has started scouting for creative agencies for production of TV spots, radio jingles, and organising exhibitions. It also has plans to empanel agencies to carry out publicity campaign at the national level. The empanelment will be for two years extendable by another one year. The regulator looks to spend funds on advertising programmes for promoting insurance awareness among the public, issuing notices, quarterly journal and calendar, among other activities. During the first decade of insurance liberalisation, the sector has reported a consistent increase in market penetration to 5.20 per cent in 2009, from 2.71 per cent in 2001. Since then, this has been in decline. However, there was a slight increase in 2015, when it reached 3.44 per cent compared to 3.3 per cent in 2014. While insurance penetration is measured as the percentage of insurance premium to GDP, insurance density is calculated as the ratio of premium to population (per capita premium).

PUBLIC AWARENESS:

The IRDAI makes use of various platforms like newspapers, television, radio and outdoor publicity to create awareness about importance of insurance. IRDAI had a budget of Rs 60 crore towards advertisement, but only an estimated Rs 24 crore, or 40 per cent, was spent. Unable to spend even 50 per cent of earmarked funds for insurance awareness last fiscal, the Regulator is looking for innovative methods to utilise this year’s advertisement budget that has been raised to Rs 66.5 crore. The government is keen on increasing insurance penetration in the country, especially in remote areas. The advertisement for consumer affairs department of IRDAI for 2017-18 has been budgeted at Rs 66.50 crore. While increasing the budget for the current financial year, the regulator is “planning for more advertisement”. Towards this purpose, IRDAI has started scouting for creative agencies for production of TV spots, radio jingles, and organising exhibitions. It also has plans to empanel agencies to carry out publicity campaign at the national level. The empanelment will be for two years extendable by another one year. The regulator looks to spend funds on advertising programmes for promoting insurance awareness among the public, issuing notices, quarterly journal and calendar, among other activities. During the first decade of insurance liberalisation, the sector has reported a consistent increase in market penetration to 5.20 per cent in 2009, from 2.71 per cent in 2001. Since then, this has been in decline. However, there was a slight increase in 2015, when it reached 3.44 per cent compared to 3.3 per cent in 2014. While insurance penetration is measured as the percentage of insurance premium to GDP, insurance density is calculated as the ratio of premium to population (per capita premium).

INSURING THE UNINSURED:

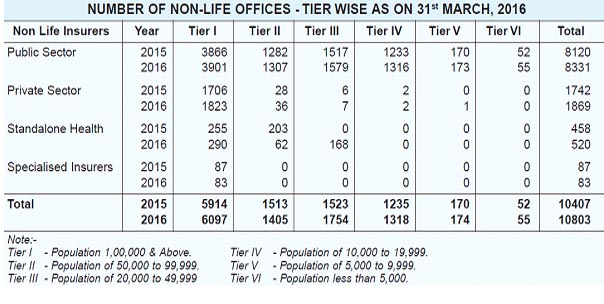

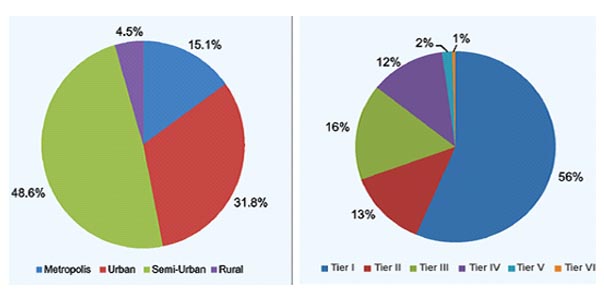

Growth in the insurance industry can be attributed to the government’s policy of insuring the uninsured by launching various schemes in the past few years. The Associated Chamber of Commerce and Industry of India (ASSOCHAM), has revealed that insurance penetration in India is likely to cross 4% by the end of this financial year. The insurance penetration has started its northward journey and it is evident from the fact that it has increased from 3.3% in 2014 to 3.44% in 2015 on the back of various insurance schemes launched by the government. As part of social security initiative and provide insurance cover to all, the government had launched Pradhan Mantri Suraksha Bima Yojna (PMSBY) and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) in 2015. Crop insurance for the farmers was launched last year. Despite the gentle rise in insurance penetration, which is percentage of insurance premium with reference to the gross domestic product (GDP), it is still far below the global average. PMSBY offers a renewable one-year accidental death-cum-disability cover of R2 lakh for partial/permanent disability to all savings bank account holders in the age group of 18-70 years for a premium of R12 per annum per subscriber. While PMJJBY offers a renewable one year life cover of R2lakh to all savings bank account holders in the age group of 18-50 years, covering death due to any reason, for a premium of Rs 330 per annum per subscriber. Besides, Pradhan Mantri Fasal Bima Yojana (PMFBY) launched last year to provide financial support to farmers suffering crop loss or damage arising out of unforeseen events will also add to insurance penetration. PMFBY is a significant improvement over the earlier schemes on several counts and comprehensive risk coverage from pre-sowing to post-harvest losses are some of the salient points. A budget provision of R5501.15 crore has been made for the scheme. The number of lives covered under the health insurance policies during 2015-16 was 36 crore, which is approximately 30% of India’s total population. The number has seen an increase every subsequent year as 28.80 crore people had the policy in the previous fiscal year. Crop insurance has become the third-biggest stream of revenue for insurance companies after motor and property. In the past, the challenge was assessing the final yield, but now technology would help with such assessments. However, fragmented landholding and yield being assessed on area basis exist the challenges. To conclude, the sector would be volatile in terms of profitability. While overall growth has been good, corporate premiums, however, have not seen a big jump. The motor insurance and health insurance segments saw 17 per cent and 22 per cent growth, respectively. The geographical distribution of life and non-life insurance offices, tier wise for 2015-16 are as follow:

INSURING THE UNINSURED:

Growth in the insurance industry can be attributed to the government’s policy of insuring the uninsured by launching various schemes in the past few years. The Associated Chamber of Commerce and Industry of India (ASSOCHAM), has revealed that insurance penetration in India is likely to cross 4% by the end of this financial year. The insurance penetration has started its northward journey and it is evident from the fact that it has increased from 3.3% in 2014 to 3.44% in 2015 on the back of various insurance schemes launched by the government. As part of social security initiative and provide insurance cover to all, the government had launched Pradhan Mantri Suraksha Bima Yojna (PMSBY) and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) in 2015. Crop insurance for the farmers was launched last year. Despite the gentle rise in insurance penetration, which is percentage of insurance premium with reference to the gross domestic product (GDP), it is still far below the global average. PMSBY offers a renewable one-year accidental death-cum-disability cover of R2 lakh for partial/permanent disability to all savings bank account holders in the age group of 18-70 years for a premium of R12 per annum per subscriber. While PMJJBY offers a renewable one year life cover of R2lakh to all savings bank account holders in the age group of 18-50 years, covering death due to any reason, for a premium of Rs 330 per annum per subscriber. Besides, Pradhan Mantri Fasal Bima Yojana (PMFBY) launched last year to provide financial support to farmers suffering crop loss or damage arising out of unforeseen events will also add to insurance penetration. PMFBY is a significant improvement over the earlier schemes on several counts and comprehensive risk coverage from pre-sowing to post-harvest losses are some of the salient points. A budget provision of R5501.15 crore has been made for the scheme. The number of lives covered under the health insurance policies during 2015-16 was 36 crore, which is approximately 30% of India’s total population. The number has seen an increase every subsequent year as 28.80 crore people had the policy in the previous fiscal year. Crop insurance has become the third-biggest stream of revenue for insurance companies after motor and property. In the past, the challenge was assessing the final yield, but now technology would help with such assessments. However, fragmented landholding and yield being assessed on area basis exist the challenges. To conclude, the sector would be volatile in terms of profitability. While overall growth has been good, corporate premiums, however, have not seen a big jump. The motor insurance and health insurance segments saw 17 per cent and 22 per cent growth, respectively. The geographical distribution of life and non-life insurance offices, tier wise for 2015-16 are as follow:

The insurance framework in India needs to be made more robust with global best practices serving as benchmarks, with due localisation. The regulator, IRDAI, must create an inclusive insurance and a digital economy, and must become an enabler – through the regulatory set up and forward-looking regulations for the Indian insurance market to tap technology-led disruptive changes. It is time to transform – in thoughts and actions. There is a need for coalition building, specialised knowledge, less hierarchy, more collaboration, and flatter professional structures. The regulator also has to be the change agent for full vertical alignment, from the fundamental philosophy of insurance to modern regulatory practices, and finally with the insurance industry delivering efficient services to the Indian insurance market. The changes cannot be held up for long as India’s share of the global economy is set to increase. India also needs to prepare to become a regional centre of excellence for (re)insurance for the markets across Asia and Africa, as the balance of economic power is moving from West to East. The essential object must be to prepare and promote the ease of doing insurance business in India, and the regulatory agenda needs to be development-oriented led by prudential regulations with conduct regulations pitching in as bulwarks. The insurance regulator needs to step up to the plate to craft a modern, transparent and progressive industry framework and a global (re)insurance platform. Insurance bundling on e-commerce platforms has enabled greater customisation in product and pricing, thereby, targeted marketing to customers.

IRDA through its order on 17 November 2015 stated that the insurance sector in India would be converging with International Financial Reporting Standards (IFRS). This circular requires all insurers to comply with the Ind AS for financial statements for accounting periods beginning on or after 1 April 2018, with comparatives for the periods ending 31 March 2018. Early adoption is not permitted. Ind AS will be applicable to both separate and consolidated financial statements. Even after permitting private players, the attitude of the regulator was more socialistic as it controlled prices and paid the claims out of a pool of resources created from the premiums collected by all the companies based on a defined proportion. The worst among them was the claims from third parties in the case of an accident involving an automobile. The lack of profitability and the underwriting disciplines means that the risk mitigation is not attended to, the right talent is not attracted and worse there is no research spends into lowering the risk thresholds – both for the traditional and emerging risks. The short-term approach taken by the market is, however, not getting corrected by the IRDAI in spite of occasional attempts. At the same time, capital accumulation is not enough to fund more growth. Paradoxically, the below par performance of the insurance firms means that fresh capital is not easy to get – either internal accruals, public listing or external borrowing or equity – all of which demand greater control and improved performance. This becomes a vicious cycle. India continues to be poorly and inadequately penetrated, that is still a question mark on the leadership of the IRDAI.

JAGENDRA KUMAR

Ex. CEO,

Pearl Insurance Brokers

71/143, “Ramashram” Paramhans Marg, Mansarovar, JAIPUR-302020

Ex. CEO,

Pearl Insurance Brokers

71/143, “Ramashram” Paramhans Marg, Mansarovar, JAIPUR-302020

References:

- IRDAI Annual Report 2015-16 ( Data contents)

- http://www.financialexpress.com/market/cabinet-clears-stake-sale-in-psu-general-eyes-rs-23000-cr/513320/

- http://www.business-standard.com/article/finance/consolidation-era-set-to-begin-in-insurance-sector-116061701057_1.html

- http://economictimes.indiatimes.com/wealth/insure/senior-citizen-health-insurance

- http://www.policyholder.gov.in/indian_insurance_market.aspx

- Newspapers & Journals

Leave a Reply