Digitalization is the use of digital technologies to change a business model and provide new revenue and value-producing opportunities; it is the process of moving to a digital business. Through digitalization, a company’s digitized resources (such as online channels, machines equipped with digital sensors, cloud-based software) are transformed into new sources of revenue and operational gains. For over a decade, it is observed that almost all the enterprises have undergone a radical change and brought wide transformation in their functions, operations and processes. Today, most of the companies are found to use digital technology. Hence, companies started looking at

Digitalization not as option but an opportunity for their growth and survival.

In its Global technology M&A, Ernst & Young captures five megatrends that are driving digital transformation across industries—namely, smart mobility, social networking, cloud computing, big data analytics, and accelerated technology adaptation. Additionally, trends such as, consumerization of IT continue to impact the enterprise IT ecosystem in India and across the globe. Thus, the need for digitalization is setting newer trends in Indian enterprises. Thus, for a developing country like India,

Digitalization is the necessity in today’s challenging environment.

Keeping in view the importance of digitalization, our Prime Minister Shri Narendra Modi is looking forward for digitalization of the country itself. For this purpose, Digitize India Platform (DIP) is in the process. DIP will provide digitization services for scanned document images or physical documents for any organization. The aim is to digitize and make usable all the existing content in different formats and media, languages, digitize and create data extracts for document management, IT applications and records management. DIP provides an innovative solution by combining machine intelligence and a cost effective crowd sourcing model. It features a secure and automated platform for processing and extracting relevant data from document images in a format that is usable for meta-data tagging, IT application processing and analysis.

Shri SNSSB Srinivasa (2004) found that the immense untapped potential for the life insurance market demands innovative thinking and execution of the plan in a creative manner. If digital processes, with user-friendly features, are put in place, India could become the I.T. leader in the world and render services for the rest of the world. Mr. Anurag Kumar (2012) concluded that while developing cross-selling strategies, banks should always remember that cross-selling is not a transaction based activity, it is primarily a relationship building exercise. Gunter Schwarz, Henrik Naujoks, Camille Goossens, David Whelan, Andrew Schwedel, Harshveer Singh (2014) examined that Asian customers show the highest demand for digital tools. Strengthening security and user-friendliness would increase digital demand in most countries. Dr Shubhada Mohan Kulkarni (2015) found that the life insurance industry can leverage the digital channel to maximize revenues through greater reach and comfort for the customer. In a study made by Cognizant Technology Solutions Ltd. on Insurance insights, revealed that increased investment in IT is expected as insurers take the natural next step to achieve higher levels of systems integration to further improve bancassurance channel effectiveness. As digitalization is relatively a new consideration, there is no much literature available.

The present paper makes an attempt to understand the digitalization in banking and insurance sectors and concludes with the importance of digitalization in bancassurance in India. For this purpose, the data is collected from secondary sources.

-

Digitalization in banking sector

Over the last few years, banking industry has witnessed a transition from transaction-oriented business to a customer-oriented one. In order to give the customer satisfaction, banks are creating various avenues for rendering their services. In this regard, banks have to be innovative. Digitalization is one such kind.

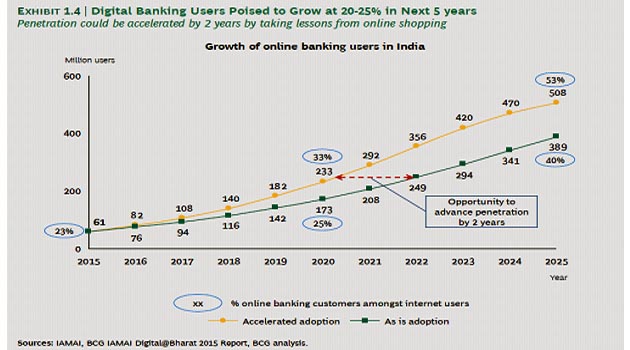

According to the McKinsey Asia Personal Financial Services Survey, 2014, there are nearly 700 million digital banking consumers across Asia. In India, Internet access is growing at 34% p.a. and has covered 20% of the population. The number of people doing digital banking is now 13% of the total banked population; this number is growing at 20-25% p.a. As many as 35% of digital banking customers also use mobile wallets from non-banks and 50% of digital banking customers are keen to try out new payment banks launched later this year. The penetration of digital banking amongst internet users is about 23%. From the figure, it can be observed that currently, there are 61 million online banking customers in India. This number is set to grow at 23% p.a. to reach about 173 million by 2020. At the current rate of adoption, this will reach 25% by 2020. However, with the concerted action from banking industry, this number could be as high as 33% by 2020. (BCG Report on Productivity in Indian banking: 2015 Inclusive growth with disruptive innovations gearing up for digital disruption)

The rise in digital banking is also because of increased mobile banking transactions. According to the RBI, the number of users in 2013-14 is 12.96 million. The RBI’s technical committee on mobile banking emphasised that, in terms of per-transaction or per-branch costs, mobile banking transaction is economical compared to the traditional banking channels and hence mobile banking channel should be encouraged for long-term economic gains.

Banks like State Bank of India, India’s largest bank is preparing an integrated channel strategy to optimize services for the next three years to achieve an optimum mix between various distribution channels – branches, ATMs, POS terminals, internet banking, mobile banking and business correspondent and customer service points.

The role of digital banking assumes paramount importance especially in a developing country like India. By and large almost all the banks in India have taken up the digitalized their operations.

-

Digitalization in insurance sector

Digital insurance in India is rising. Unlike banks, insurance companies have not reached the digitalization process yet. Insurance companies are exploring cost-effective modes of distribution. Internet, mobile & social media are helping create the popularity for digital insurance like never before. Customers prefer online because of better pricing, increased transparency & convenience of purchase. At present, LIC (Life Insurance Corporation) is in the process of digitization engaged in the creation of insurance repositories.

Alternative channels such as phone, internet-PC, and internet-mobile are gaining popularity and sometimes these alternative channels are preferred by customers over traditional channels (2012 insurance survey of 16,500 customers across 30 countries. Results can be found in the World Insurance Report 2013, Capgemini and Efma).

According to Digital@Insurance-20X By 2020, a Google-BCG report, by 2020, six per cent of all insurance sales in India will occur online. At this point, life insurance sales contribute about Rs 300 crore, motor insurance another Rs 250 crore, while other insurance lines such as health and travel make up approximately Rs 150 crore of the total insurance pie. Digital influence on new insurance sales is already Rs. 7000-8000 crores

It is projected that by 2020, 3 out of 4 insurance policies will be influenced online. Life insurance new business to grow to Rs. 125-150K crores, Life insurance renewals to grow to Rs. 550-700K crores; Non-life insurance to grow to Rs. 200-230K crores

-

Bancassurance – Concept and growth in India

With the Liberalization, Privatization and Globalization (LPG), the banking and insurance sectors underwent many changes. At the end of March 2014, there are 53 insurance companies operating in India; of which 24 are in the life insurance business and 28 are in non-life insurance business. In addition, GIC is the sole national reinsurer. Of the 53 companies presently in operation, eight are in the public sector – two are specialized insurers, namely ECGC and AIC, one in life insurance namely LIC, four in non-life insurance and one in reinsurance. The remaining forty five companies are in the private sector. (IRDA Annual Report 2013-14).

Life insurance industry recorded a premium income of Rs.3,14,283 crore during 2013-14 as against Rs. 34,898.47 crore in 2000-01. The CAGR (Compound Annual Growth Rate) during this period is 18.42% per year. Following the recommendations of the Malhotra Committee report, in 1999, the Insurance Regulatory and Development Authority (IRDA) was constituted as an autonomous body to regulate and develop the insurance industry. The life insurance industry in India has been progressing at a rapid pace particularly after the year 2000. The entry of private banks after 2003 increased FDI (Foreign Direct Investment) in equity to 49% placed additional challenges to the insurance sector.

Subsequently, the Government of India specified insurance as a permissible form of business under section 6 (1) of the Banking Regulation Act, 1949, was issued on August 3, 2000 and accordingly the guidelines were issued. On the side of banking sector, with the opening up of private banks, due to intense competition, banks are to look for alternative sources of revenue. This led to the evolution of ‘Bancassurance’. “Bancassurance” refers to distribution of insurance products through banking channels. It involves three parties – the banker, insurer and the policy holder.

Insurance is very important particularly in a country like India as insurance is more sold than bought. Although, there are various channels for marketing insurance products, the country, with its rural population percentage covering as much as 70%, requires a unique channel which enables to bring insurance products to reach the common man through a local bank branch- alternatively called as Bancassurance channel.

Bancassurance will spread awareness and promote insurance across various segments of the society through the bank branch network. Banks can perceive bancassurance as a customer retention strategy by making available all financial products and services at one stop by increasing the quality of the customer experience. Bancassurance also provides fee-based income to banks. Besides, the customers respond more to their bankers as the latter is expected to have a better understanding of the former’s financial needs. Bancassurance saves costs to the insurance companies by means of cost reduction in selecting, training, motivating, and compensating the agents. However, banks must ensure that procedures related to claim settlement and policy servicing should not result in administrative and legal issues from its customers.

Bancassurance is in a different stage of maturity across different regions but is expected to grow at a high rate with the commission earned through bancassurance expected to grow globally at a CAGR of 5.29% between 2013 and 2017. Although agents and broker remain the major distribution channels, alternative channels such as the internet, banccassurance, and social media are rapidly finding favor with insurance customers.(Trends in Insurance Channels 2013: Key emerging business and technology trends across insurance channels, Capgemini). As an insurance channel, bancassurance can take different forms based on the banking system regulations and culture of each country. In developed countries, insurers leverage the reach and brand image of banks to increase the customer base and cross-sell insurance products. But in developing countries, insurers leverage the banking infrastructure to reach the rural population. In Europe, bancassurance holds one-third of the total market share. There are significant growth opportunities in emerging European countries such as Turkey and Poland.

In Asia-Pacific, bancassurance is still an emerging channel and it is expected to grow faster due to improved customer service and entrance of large foreign insurance players in the market. The presence of large foreign insurance players has fuelled the bancassurance growth in Latin America.In contrast, bancassurance is still in a nascent phase in the U.S. with only 2% market share. This is mainly due to the separation between insurance providers and banks. Even though the maturity varies across regions, insurers are expected to invest on bancassurance to leverage the customer reach and trust of bank network. (Bancassurance growth to be fostered by emerging markets, Trimetric Research, April 2013.

Bancassurance concept originated in Europe and gained momentum in India only after 2000. Under channel-wise individual and group new business performance, in terms of percentage of premium, bancassurance channel alone contributed to 5.57% and 2.33% respectively in 2006-07. The corresponding increase was 15.62% and 6.35% in 2013-14. In non-life business, Gross direct premium was 5.57% in 2006-07 as against 6.61% in 2013-14.

In FY 2015, the bancassurance business for insurers with bank partners had increased. The sector gets 55%-65% of business from banks and those with bank promoters get more than half of their business from banks.

Currently, banks are allowed to tie-up as a corporate agent with one life, one non-life and one standalone health insurer, as a corporate agent. IRDA has proposed an open architecture policy whereby an insurer can have tie-ups with up to three insurers.

According to the RBI, majority of the household savings are found to be in bank deposits. This is a reflection of the customer trust and loyalty in banks in India. While for banks, it is a means of generating additional fee income, for insurance companies, it is a tool for increasing their market penetration and premium and also cost saving as the products are distributes through the huge branch network of the banks. In the process, customers can benefit from the reduced price, high quality product and delivery. Further, Bancassurance in India has lot of scope in terms of mainly favourable demographic dividend whereby, the median age of an is expected to be 29 years by 2020, with 900 million of the population falling in the age group of 15-60 years by 2025. Further, the natural calamities occurring in the country such as cyclone, tsunami and heavy rains are likely to create the demand for taking insurance policies. Also, RBI’s initiatives towards financial inclusion to bring the unbanked and under banked into the insurance coverage, increased FDI cap and changing regulatory norms are expected to see more future for bancassurance i n India.. As it is, Government of India data show that the total number of accounts opened under PMJDY (Prime Minister Jan Dhan Yojana scheme, a drive towards financial inclusion) stood at Rs.18.96 Crore as on October 21

st 2015 with a total balance of Rs.25,899 crore.

-

Importance of digitalization in bancassurance business in India

Digitalization involves paperless work and is necessary for networked society. In India, rising level of internet, mobile phones and smart phones are bringing tremendous growth for digitalization. Bancassurance, online sales channel and other alternative distribution channels are becoming increasingly dominant in the life insurance industry in India. By 2020, 75% of insurance sales will be online. There is a saving of 15% to 20% in total costs of life insurance due to digitization. The savings so generated if passed on to the customers can not only result in customer delight but also build customer relationships in the long run.

Digitalization allows the up-to-date customer information available with banks and this can help both banks and insurance companies design the products suiting the changing requirements of the customers. Insurance companies can seek the advantages derived by the digital banking operations such as convenience, speed and safety at which services are delivered in distributing the insurance products and services too. Besides, insurance companies and brokers are seeing a big business by offering customized insurance packages for e-commerce firms to cover risks such as data theft, online frauds and hacking of websites.

There is a need for both the banks and insurance companies to create a single customer view which gives a comprehensive picture of customer information, i.e., his needs, preferences, interactions in order to have better knowledge and understanding of customers. While banks can track customer demographics and his transactions in detail, insurers can collect timely data on mortality and morbidity, weather and natural disasters like earthquakes, tsunami and floods in order to facilitate better claim management. Recently, due to torrential rains occurred in Chennai during November 2015, it is estimated that insurance companies are likely to take a hit of more than Rs.2,000 crore claims from automobiles, property and small & medium enterprises (SME).

In the context of economy being digitalized, getting right and timely information provides plenty of opportunities to the firms. Thus, digitalization would bring several advantages to all the three parties of the bancassurance to make it a win-win-win situation.

About the Author : Mrs. P.Srilatha, Faculty Member, M.C. Gupta College of Business Management and Ph.D. scholar, Jawaharlal Nehru Technological University (JNTU), Hyderabad,

Email: [email protected]

- Shri SNSSB Srinivasa, Promoting insurance through information technology, The Journal of insurance institute of India, Vol. no. XXX, July – December 2004, pp 94-105.

- Anurag Kumar, Cross Selling (With Special Reference to State Bank of India), International Journal Of Social Sciences & Interdisciplinary Research, Vol.1 No. 6, June 2012, pp 116-123.

- Gunter Schwarz, Henrik Naujoks, Camille Goossens, David Whelan, Andrew Schwedel, Harshveer Singh, Customer loyalty and the Digical® transformation in P&C and life insurance: Global edition 2014, June 18, 2014.

- Dr Shubhada Mohan Kulkarni, Life Insurance Distribution at Crossroads, IOSR Journal of Business and Management, PP 16-22.

- A Report of Cognizant Technology Solutions Ltd. on Insurance Insights.

- Reports of the IRDA and RBI

- Watson – India market life insurance update September 2014.

- Trends in Insurance Channels 2013: Key emerging business and technology trends across insurance channels, Capgemini.

- http://timetricmarketing.wordpress.com/2013/04/02/bancassurance-growth.

- http://thefinancialbrand.com/53300/digital-banking-customer-retention-trends/

- https://www.linkedin.com/pulse/20141010112245-10415234-seven-digital-banking-trends-you-might-see-in-2015

- Role of digital banking in furthering financial inclusion kpmg.com/in

- Business Line and The Economic Times News papers – Various issues.

Leave a Reply