Personal accident insurance market in India to benefit from policy standardization, says GlobalData

The Insurance Regulatory and Development Authority of India (IRDAI) has mandated all general and health insurers in the country to offer standard personal accident insurance ‘Saral Suraksha Bima’ from 1 April 2021. This product with standard coverage and policy wordings will simplify product offering and promote the uptake of personal accident insurance policies in the country, says GlobalData, a leading data and analytics company.

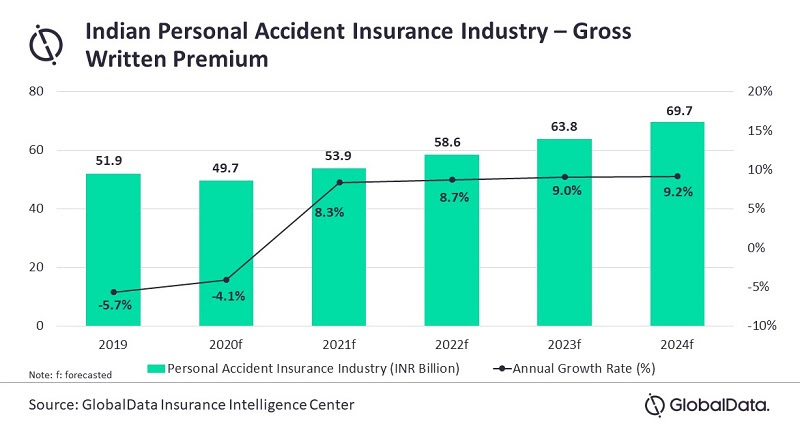

GlobalData estimates the personal accident insurance industry in India to grow at a compound annual growth rate (CAGR) of 6.1% during 2019-2024 due to mandatory personal accident cover for employees, motor and travel insurance policies. In addition, there is an increasing awareness of independent personal accident cover mainly due to limited benefits offered under group policies.

Anjuli Shrivastav, Insurance Analyst at GlobalData, comments: “The standard features and policy wordings offered under ‘Saral Suraksa Bima’ product will make it easier for buyers to choose standalone personal accident insurance from a wide variety of products available in the market. Uniformity and greater transparency in policy contracts will improve the uptake of standalone personal accident insurance product and help increase penetration.”

As per the new guidelines, standard personal accident product will come with one year tenure and cover death and disability. Sum insured will be in multiples of INR50,000 with a minimum insured amount of INR250,000 and a maximum of INR10m.

Insurers will be allowed to provide extra benefits and add optional covers such as temporary total disablement, hospitalization expenses in the same product and determine premiums within the guidelines prescribed by the IRDAI. This will encourage insurers to test new products and offer innovative and customized products.

Ms. Shrivastav concludes: “The uniform clauses set by the regulator will provide more confidence to the policyholders when purchasing a new product, as the risk of being deprived will be lower. This will benefit insurers in generating new business premiums and in retaining customers.”

Leave a Reply