Asia-Pacific is a very lucrative market for cyber security insurance companies: N K V Roop Kumar, Chief of Risk, SBI Life Insurance

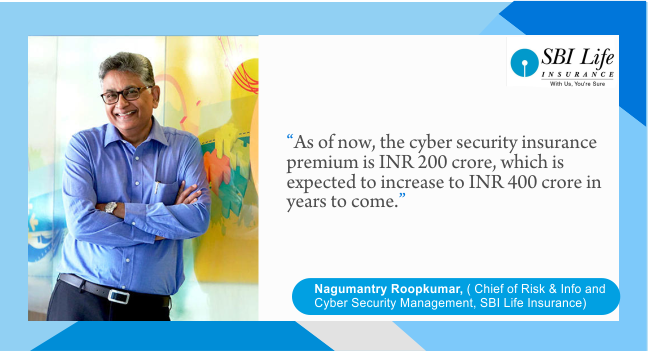

Mr Nagumantry Roop Kumar is a Risk & Insurance professional, with 31 years of experience (20 years in LIC of India and 11 years in SBI Life Insurance Co) in handling Enterprise Risk Management, Business Continuity Management, Information & Cyber Security, Fraud Monitoring, Operations & Marketing. In an interview with The Insurance Times, Mr Roop Kumar talks about the Risk Management Practices in India.

What is the Current Scenario of Risk Management Practices in India?

India is one of the fastest growing economies in the world, facing significant challenges in risk, business continuity & cyber security. Indian Regulators are according high priority to Risk Management & Governance. They have mandated that all institutions are to put in place, an ERM framework to deal with various challenges which they are facing.

The insurance regulator, IRDAI, is coming up with Risk Based Capital & Risk Based Supervision Guidelines. Also in the past, IRDAI has released Corporate Governance guidelines of 2016, Information Security Guidelines 2017, Outsourcing Guidelines 2017 etc.

RBI in its latest mandate directs “NBFCs to appoint Chief Risk Officer and the CRO should be reporting to the MD&CEO/Risk Management Committee (RMC) of the Board.”

RBI Guidelines, Basel 3 guidelines to Banks, also stress upon creating a strong ERM framework. The Indian industry is in need of competent risk professionals to manage this increasing need.

Deloitte 2018 Global Risk Survey highlights that-

- Only 64% of the Organizations have an “in-house” risk management function.

- Only 61% have a full time CRO

- Risk management is an emerging discipline in India and not completely mature.

- Technical, professional qualifications and special interest groups/societies are still taking root in the country.

- Regulations are recent and evolving, and are in the process of implementation in India.

- Information & Cyber Security

- Natural Disasters

- Fire

- Terrorism and Insurgency

- Political and Governance instability

- Need to analyze threats/trends/action on behavior.

- Evolve proactive brand related crisis management.

- Create responses to social media incidents, initiate targeted campaigns, create Brand Advocates.

- Foster a “Risk Intelligent” culture and training of employees.

Leave a Reply