WEB AGGREGATORS IN INDIA: PAST IMPERFECT, PRESENT TENSE, FUTURE UNCERTAIN

Web Aggregators compile and provide information about insurance policies of various companies on a website. Insurance aggregators provide a platform to compare various insurance policies in the same category, typically aiming at buying one that suits the needs of an individual. The platform aims at enhancing the user experience by either letting individuals compare policies right there or redirect them to the website of that particular insurer. Although the primary aim of these websites is to let the customers make their choices based on a thorough comparison, the comparison criterion includes basic common factors, such as insurance premium and sum assured. IRDAI has recently launched Insurance Regulatory and Development Authority of India (Insurance Web aggregators) Regulations 2017 and it will supersede Insurance Regulatory and Development Authority (Web Aggregators) Regulations, 2013. The new guidelines for the web aggregators mandate that no insurance web aggregator should promote or push a particular product of a particular company either through its web-site or through distance marketing. Further, the product has to be sold based on the need analysis of the prospect. While soliciting and procuring the insurance business, the Insurance Web Aggregator has to ensure that if the Web Aggregator is having tie-ups with more than one insurer, they have to provide prospective buyers with the details such as scope of coverage, term of policy, premium payable, premium terms and any other information which the customer seeks on all products available with them. The earlier guidelines made it difficult for web aggregators to offer products that could earn them reasonable income so that they could sustain themselves in the long run. Consumers will now also benefit from the easy access to these products online, as the digital channel is increasingly becoming their preferred mode for research and transactions.

While soliciting and procuring the insurance business, the Insurance Web Aggregator has to ensure that if the Web Aggregator is having tie-ups with more than one insurer, they have to provide prospective buyers with the details such as scope of coverage, term of policy, premium payable, premium terms and any other information which the customer seeks on all products available with them. The objective of the Insurance Web Aggregator Regulations is to supervise and monitor. Web Aggregator is an insurance intermediary who maintains a website for providing interface to the insurance prospects for price comparison and information of products of different insurers and other related matters. IRDAI has clearly defined and given a structure to some of the important activities and functions of the Web Aggregators. They include: display of product comparisons on web-site and their conditions, transmission of leads by web aggregator to the insurer in a specified manner, the manner and process of sale of insurance online by web aggregators, sale of insurance by tele-marketing mode and other distance marketing for solicitation of insurance based on the leads generated from its designated website. Even the payment of remuneration of an Insurance Web Aggregator shall be governed by the regulations as set by IRDAI. The new guidelines for the web aggregators also mandate that no insurance web aggregators should promote or push a particular product of a particular company either through its web-site or through distance marketing. Further, the product has to be sold based on the need analysis of the prospect. Apart from more products to sell, the regulations also bring good news to the web aggregators on the issue of remuneration. Since these web aggregators have gained prominence in India, IRDAI has brought about a set of regulations for these aggregators. This set of regulations define the process of attaining a license to act as a web aggregator, disclosure norms, penalties for aggregators without a license, remuneration of web aggregators and other related matters.

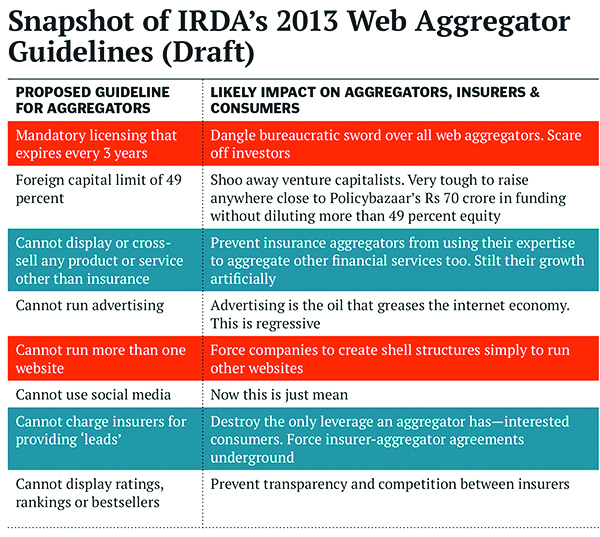

The guidelines for Web aggregators released in 2013 put a blanket ban on such entities for advertising and giving reviews or ratings of products on their websites. Charging for lead generation was also banned, when this was a widely accepted business model in e-commerce. The regulations further prevented Web aggregators from selling non-insurance products. Even unit-linked insurance plans (ULIPs) were not to be sold over the distance mode, even though these plans were emerging strongly post revisions. The model was so tightly defined by the guidelines that it left very little space for innovation.

The guidelines for Web aggregators released in 2013 put a blanket ban on such entities for advertising and giving reviews or ratings of products on their websites. Charging for lead generation was also banned, when this was a widely accepted business model in e-commerce. The regulations further prevented Web aggregators from selling non-insurance products. Even unit-linked insurance plans (ULIPs) were not to be sold over the distance mode, even though these plans were emerging strongly post revisions. The model was so tightly defined by the guidelines that it left very little space for innovation.

Insurance is a large growing market. Various estimates say that there would be 450 million internet users by 2020. The insurance industry has increased multiple-fold post the introduction of insurance web aggregators in the market. They have become extremely receptive to these aggregators and are rushing to enter into agreements and tie-ups with them. They understand the reach of the internet and have played wisely by embracing the power of the online aggregators, especially after the regulations provided by the IRDA. The insurance web aggregators act as information providers, telemarketers, solicitors and brokers. They have made life so much more convenient for busy buyers today and have helped raise the insurance industry of the country to an all-new high. The scope for them is enormous today since the online market is one so vast that leaving it untapped would be a grave blunder on the part of the insurance companies. Insurance will continue to see massive changes thanks to insurance aggregators, transforming from a seller’s market to a buyer’s market world over. Insurers will continue to partner with these aggregators, while focusing primarily on the needs of the consumer, in so doing. Aggregators will face competition from other insurance aggregator websites, threats on the cyber-security front and the challenge of personalisation of products according to the profile of the customer; however they will continue to emerge as the most popular choice for purchasing insurance products. New web aggregator rules gazetted by the IRDAI now allow all kinds of insurance products to be sold on the aggregators’ portals, as well as make doing business on the platforms easier in several other respects. Key changes made to the regulations are as follow:

Insurance is a large growing market. Various estimates say that there would be 450 million internet users by 2020. The insurance industry has increased multiple-fold post the introduction of insurance web aggregators in the market. They have become extremely receptive to these aggregators and are rushing to enter into agreements and tie-ups with them. They understand the reach of the internet and have played wisely by embracing the power of the online aggregators, especially after the regulations provided by the IRDA. The insurance web aggregators act as information providers, telemarketers, solicitors and brokers. They have made life so much more convenient for busy buyers today and have helped raise the insurance industry of the country to an all-new high. The scope for them is enormous today since the online market is one so vast that leaving it untapped would be a grave blunder on the part of the insurance companies. Insurance will continue to see massive changes thanks to insurance aggregators, transforming from a seller’s market to a buyer’s market world over. Insurers will continue to partner with these aggregators, while focusing primarily on the needs of the consumer, in so doing. Aggregators will face competition from other insurance aggregator websites, threats on the cyber-security front and the challenge of personalisation of products according to the profile of the customer; however they will continue to emerge as the most popular choice for purchasing insurance products. New web aggregator rules gazetted by the IRDAI now allow all kinds of insurance products to be sold on the aggregators’ portals, as well as make doing business on the platforms easier in several other respects. Key changes made to the regulations are as follow:

The objective of the Insurance Web Aggregator Regulations is to supervise and monitor the web aggregator as an insurance intermediary, which maintains a website for providing an interface to insurance prospects for price comparison and information about products of different insurers and other related matters. Similar to buying insurance products offline through an insurance agent or a broker, buying life insurance online also needs to be an informed decision. It’s better to speak to the web aggregator executive before initiating the transaction online so as to not end up buying the wrong product for your specific need. And, approaching them after doing at least a bit of research on what your requirements are will make the process much more seamless, informative and free from surprises. According to a study conducted by the Boston Consulting Group titled ‘The Changing Face of Indian Insurance’, due to the expanding digital footprint in the country, comparisons of insurance products and internet searches with the help of online insurance aggregators have moved up from 10% in January 2012 to 17% in January 2015. This number is expected to increase further with an increase in internet usage. Insurance aggregators provide customers with a convenient and transparent means by which, they can compare insurance products and decide which product suits their needs. Thanks to technological advancements in the digital space and the growing use of smart phones, customers now have easy access to a wealth of information via the internet. Online aggregators provide full-fledged websites, where they compile the information of insurance policies of varied companies, and give customers the option of comparing the prices of products. They act as brokers, knowledge providers, solicitors and telemarketers. The regulator has acknowledged the role of Web Aggregators in expanding the online platform. However, as the rewards will usually be a part of the companies’ marketing budgets, allowing them is unlikely to result in higher prices for the products. Currently, web aggregators account for less than 1% of the total insurance sale and these guidelines will boost greater participation by the web aggregators.

REFFERENCES:

WHAT IS A WEB AGGREGATOR ?

As per the definition of the Insurance Regulatory and Development Authority of India (IRDAI), Insurance Web Aggregators compile and provide information about insurance policies of various companies on a website. In other words, they collect data from various sources and databases, such as insurance company websites, and compile this data to make it presentable to any potential insurance policy buyers. Online access to life insurance plans is also available through insurance aggregators who are essentially insurance brokers having an online presence. The websites of insurance aggregators work as comparison sites as they showcase plans of various insurers. The objective of the Insurance Web Aggregator Regulations is to supervise and monitor Web Aggregator as an insurance intermediary who maintains a website for providing interface to the insurance prospects for price comparison and information of products of different insurers and other related matters. The earlier guidelines made it difficult for web aggregators to offer products that could earn them reasonable income so that they could sustain themselves in the long run. Consumers will now also benefit from the easy access to these products online, as the digital channel is increasingly becoming their preferred mode for research and transactions. Web aggregators compile and provide information on insurance policies of various companies on a website. IRDAI has mandated web aggregators to provide unbiased information of insurance products on different types of policies—like whole life insurance, term plan, health insurance, endowment, annuity on their portals. Web aggregators currently account for less than 1% of total insurance sales and the new rules will boost greater participation by web aggregators. In January 2017, there were 21 web aggregators in India.

ROLE OF WEB AGGREGATORS:

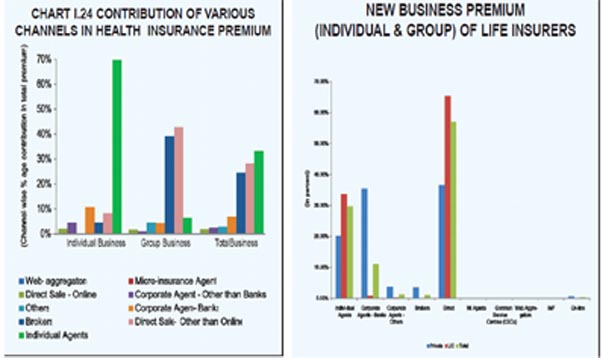

While the role of web aggregators requires them to facilitate comparison of various insurance policies by entering into agreements with insurers, it does not include endorsing any particular insurer or advertising a particular insurance policy. The primary motive should be merely to provide the required justified information to the potential buyer. While performing its duties, an insurance web aggregator has to ensure that no inconvenience is caused to the customer. It can act as an insurance broker or solicitor, contacting the potential buyer directly. It may also provide the buyer’s contact details to various relevant insurance companies, provided the buyer is made aware of the fact that their contact details are going to be shared with any such insurance company. Classified as Insurance intermediaries, web aggregators are portals that help the customer to compare and buy insurance products. They further improve the purchase expense by either directing customers to the insurer’s website or helping them through the sale process. The primary role of these portals is to enable comparison. In the sense, they provide a listing of products and showcase comparison on parameters such as eligibility criteria, sum assured and premiums. As per rules, web aggregators need to display product pricing that is inclusive of all taxes. Further, the rules prohibit web aggregators from displaying ratings, rankings, endorsements or bestselling insurance products. They are also to refrain from commenting on insurers or their products at any location in their websites. Web Aggregators have played an important role in boosting the online market for several products, such as term plans. Comparison is essential for the customers in the online products, such as term plans, that over 90% of the customers compare and buy them through web aggregators. IRDAI has clearly defined and given a structure to some of the important activities and functions of the Web Aggregators. They include – display of product comparisons on web-site and their conditions, transmission of leads by web aggregator to the insurer in a specified manner, the manner and process of sale of insurance online by web aggregators, sale of insurance by tele-marketing mode and other distance marketing for solicitation of insurance based on the leads generated from its designated website.

PAST IMPERFECT:

With the growing need for customers to compare insurance products before making a purchase, the concept of insurance aggregators was introduced. Aggregators provide customers a comparison between similar insurance products, thus enabling them to make an educated choice before purchase. Though insurance aggregators have seen a good success rate in the UK, India and other key European markets, they are yet to achieve the same levels of success in other regions in the world. With an increased focus on developing digital technologies, the Asia-Pacific and American regions will see many growth opportunities for online insurance aggregators over the next 5-10 years, with online aggregators already having been established in Canada, Australia, USA, Hong Kong, South Korea, Singapore and India. The emergence of insurance aggregators has completely revolutionised the distribution and purchase of insurance products and services. They were first introduced in the UK insurance industry in 2002 with the launch of the site ‘confused.com’. After merely a decade, they now account for 50% of personal insurance products, and 60% of new motor insurance policies, Insurance aggregators were introduced for the purpose of enabling customers to compare insurance products, while deciding which product to buy. They are independent entities, who are granted a license (by the IRDAI in the case of India, to display insurance product information of multiple companies on a common platform. Web aggregators are lacking in following areas:- Only certain type of person can lead a Web Aggregator business:The Principle Officer (for example, the CEO) has to be someone who has been carrying out reinsurance related activity or insurance consultancy for a continuous period of seven years, or for not less than seven years, has been a principal underwriter or a manager in a nationalized insurance company in India, or is an associate or fellow of some of the institutes specified by the IRDA.

- Can’t sell much stake to Indian Investors:Foreign investors can own up to 49% of the paid-up equity capital of Insurance Web-Aggregator at any time. However, Indian investors together, can only own 25%, and no Indian investor can own more than 15% of the paid-up equity capital.

- Founders and investors can’t exit in the last two years:The foreign promoter or foreign investor or Indian Promoter of the existed venture have exit for any reason at any time during the preceding two financial years from the date of application.

- Approval of hosting provider and other vendors: including for the Lead Management System, Webhosting, and Other core activities. It also needs to approve the “Change of location of the Servers hosting the comparison website(s)”

- Determination of name:All insurance web aggregators need to have the phrase “Insurance Web-Aggregator” in their name. They also need to “take the prior approval of the Authority for change of its name.” Oh, and “Insurance Web-Aggregators are not permitted to use any other name in their correspondence/ literature/ letter heads without the prior approval of the Authority.”

- The lead generation work: Web Aggregator has to send the lead to the insurer “Not later than three days of (the users) visit to the web site.” Specific products under specific criteria can only be compared, such as eligibility criteria, premium term, riders, benefits, etc.

The guidelines for Web aggregators released in 2013 put a blanket ban on such entities for advertising and giving reviews or ratings of products on their websites. Charging for lead generation was also banned, when this was a widely accepted business model in e-commerce. The regulations further prevented Web aggregators from selling non-insurance products. Even unit-linked insurance plans (ULIPs) were not to be sold over the distance mode, even though these plans were emerging strongly post revisions. The model was so tightly defined by the guidelines that it left very little space for innovation.

PRESENT TENSED:

The Indian insurance regulator, on 13th May, 2017, in a gazette notification, proposed new rules for websites that allow individuals to compare a range of general and life insurance policies, and then purchase a suitable policy. These new rules are not to cause any disruption but to reduce vagueness only. Online aggregators provide full-fledged websites, where they compile the information of insurance policies of varied companies, and give customers the option of comparing the prices of products. They act as brokers, knowledge providers, solicitors and telemarketers. Comparisons of various insurance policies offered by insurance giants in the market have become extremely simple, with all the competing features, costs and coverage displayed on a single screen. However, three changes to the rules are noteworthy. First, the rules now allow all kinds of insurance products to be sold on the web aggregators ‘portals. Earlier, Unit Linked Insurance Plans (ULIPs) were not allowed. Two, the ticket size of the policies that can be sold here has been increased from Rs. 50,000 to Rs. 1.5 lakh, giving a fillip to bundled life insurance policies. Three, the rules now allow remuneration even on zero commission policies, such as the online term plans, through rewards. Following are the imposed limitations on the Web Aggregators:- No referral arrangement: The Web Aggregator cannot have a referral arrangement with an Insurer.

- No payment for transmission of leads generated:No charges shall be paid for transmission of leads by the Insurance Web-Aggregator to the Insurer.

- Payments only for conversion sales: Leads which are converted into sale of insurance policies will entitle the Insurance Web-Aggregator to earn remuneration as applicable to insurance intermediaries.

- No payments for signing up an insurance co:No insurer shall pay and no Insurance Web-Aggregator shall receive any signing fee or any other charges by whatever name called, except those permitted by the Authority under relevant regulations, for becoming its Insurance Web-Aggregator.

- Only a display fee of Rs 50,000 per insurance productfor displaying the product on the website.

- Deal with the insurance company three years only:The agreement between an insurer and Insurance Web-Aggregator shall be valid for a period of three years from its date, subject to the validity of registration of Insurance Web-Aggregator.

- Can’t market other products:A web insurance aggregator cannot display other products or services (financial, FMCG or anything else) on their website.

- Can’t sell lead to more than three insurers, even with user permission:Insurance Web-Aggregator should provide an option to select up to three insurers by the visitor, to whom the lead shall be transmitted simultaneously.

- No display advertising

- Can’t operate multiple websites:“or tie up with other approved / unapproved /un-registered entities / websites for lead generation / comparison of product. Only exceptions available to them are if they use the domain names with .com, .in or .co.in “for the primary website of the Insurance Web-Aggregator…”. Even then, the Insurance web aggregator has to inform the IRDA in writing of each new website and the date of launching such websites or mobile sites, “within 15 days from the date of Domain Name Registration and Date of launching respectively in case of any change in the name(s) of the existing websites or new websites.”

- Can’t operate the websites of other Financial / Commercial / marketing or sales or service entities

FUTURE UNCERTAIN:

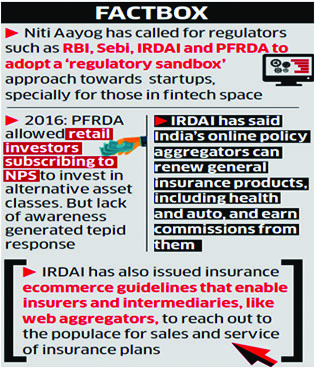

The IRDA of India has brought in new changes for insurance aggregators keeping in view the remunerations issue. These companies are now eligible for renewal commissions too, in case of a non-life insurance policy, such as motor insurance, health insurance, and home insurance. The e-filing income tax associated with health insurance remains the same, i.e. under section 80D of the Income Tax Act, 1961. Life insurance policies are still not considered as per the remuneration issue, as these policies are long-term agreements. Insurance aggregators must continue to emerge and offer insurance products directly to consumers, while coming up with new and inventive services to encourage loyalty and brand retention. In the non-life space—for products such as health insurance, motor insurance and home insurance—it has now been clarified that web aggregators are entitled to renewal commissions as well. However, for life insurance policies, renewal commissions are still not allowed as they are long-term contracts. So, when they sell a life insurance policy, web aggregators are entitled to first-year commissions only. General insurance products are annual contracts and every time the policy is renewed, there is a new policy number assigned to the policyholder. This means that web aggregators are entitled to renewal commissions, but it was a huge grey area and many insurers interpreted the rules differently. But, in the non-life space—regarding general insurance products such as health insurance, motor insurance and home insurance policies—it has now been clarified that web aggregators are entitled to renewal commissions as well. However, for life insurance policies, they are still not allowed the renewal commissions as they are long-term contracts. So, when they sell a life insurance policy, web aggregators are entitled to first-year commission only—remember that commissions in life insurance are front loaded. In the life insurance space, the rules now even allow for zero commissions products remuneration, in the form of rewards. As per the new rules on commissions, which were announced in December last year, insurers can pay extra—over and above commissions—to distributors through rewards. The reward, however, is capped at 20% of first-year commission and is for intermediaries who primarily sell insurance. Allowing rewards brings in transparency and regulates the amount that can go to intermediaries. However, there is still considerable flexibility for web aggregators as they can engage in other activities such as outsourcing. This is currently not at par with rules for other intermediaries. While the current rules don’t allow commissions for pure online products, the industry practice has been to compensate web aggregators under different cost heads such as by paying them a fee for outsourcing activities. These regulations, in that sense, have acknowledged these activities and formalised these payments. This, however, will not hike prices. The regulator has acknowledged the role of intermediaries in expanding the online platform. However, as the rewards will usually be a part of the companies’ marketing budgets, allowing them is unlikely to result in higher prices for the products

Insurance is a large growing market. Various estimates say that there would be 450 million internet users by 2020. The insurance industry has increased multiple-fold post the introduction of insurance web aggregators in the market. They have become extremely receptive to these aggregators and are rushing to enter into agreements and tie-ups with them. They understand the reach of the internet and have played wisely by embracing the power of the online aggregators, especially after the regulations provided by the IRDA. The insurance web aggregators act as information providers, telemarketers, solicitors and brokers. They have made life so much more convenient for busy buyers today and have helped raise the insurance industry of the country to an all-new high. The scope for them is enormous today since the online market is one so vast that leaving it untapped would be a grave blunder on the part of the insurance companies. Insurance will continue to see massive changes thanks to insurance aggregators, transforming from a seller’s market to a buyer’s market world over. Insurers will continue to partner with these aggregators, while focusing primarily on the needs of the consumer, in so doing. Aggregators will face competition from other insurance aggregator websites, threats on the cyber-security front and the challenge of personalisation of products according to the profile of the customer; however they will continue to emerge as the most popular choice for purchasing insurance products. New web aggregator rules gazetted by the IRDAI now allow all kinds of insurance products to be sold on the aggregators’ portals, as well as make doing business on the platforms easier in several other respects. Key changes made to the regulations are as follow:

| Sr. No. | Head | Old Regulations | New Regulations | Impact |

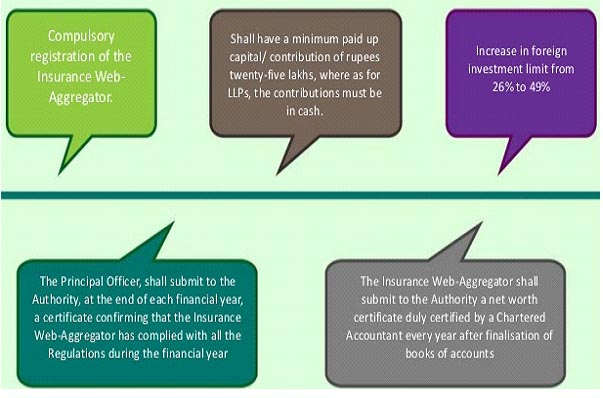

| 1. | Net Worth | INR 10,00,000 | INR 25,00,000 | To meet the requirement within 1Yr |

| 2. | Equity held by Foreign Investors (“FI”) | Less than equal to 26% of the paid-up equity capital at any time. | Less than equal to 49% of paid-up equity capital at any time. | This is as per the change in the FDI policy. Specific conditions are provided under Schedule XII of the New Regulations. |

| 3. | Professional Indemnity | Minimum – INR 10,00,000 Maximum – 3 times the remuneration received during the previous year | Minimum – INR 25,00,000 Maximum – INR 100,00,00,000 | Maximum indemnity has been provided. |

| 4. | Renewal Fees | INR 10,000 | INR 25,000 | Low impact. |

| 5. | Grant of registration | None | If the FI or Indian promoter has exited at any time during the preceding two financial years from the date of application, then the applicant may not be eligible to obtain registration as Insurance web aggregator. | IRDA can exempt the requirement. In future, the exit should be scheduled in accordance with renewal timelines. |

| 6. | Annual Fees | INR 5000 | Nil | Low impact. |

| 7. | Premium Ceiling in case of life insurance (for insurers) | Insurers shall not solicit non – single premium policies whose premium is exceeding INR 50,000. Single premium policies shall not be solicited for a premium exceeding INR 50,000 over telemarketing | Insurers shall not solicit non- single premium policies whose premium is exceeding INR 1,50,000. Single premium policies shall not be solicited for a premium exceeding INR 1,50,000 over telemarketing mode. | Business friendly. |

REFFERENCES:

- https://www.medianama.com/2016/06/223-still-no-point-in-starting-an-insurance-web-aggregator-in-india/

- https://economictimes.indiatimes.com/wealth/insure/irdais-new-web-aggregators-rules-to-curb-aggressive-selling/articleshow/58576757.cms

- A study by Boston Consulting Group titled ‘The Changing Face of Indian Insurance’

- https://economictimes.indiatimes.com/small-biz/entrepreneurship/india70why-family-offices-need-to-chip-in/articleshow/60066436.cms

- http://www.jclex.com/displaynews2.php?conid=171

- IRDA Journal 2015-16

- GIC Yearbook-2016

- Newspapers & Journals.

Author

JAGENDRA KUMAR

Ex. CEO, Pearl Insurance Brokers

71/143, “Ramashram” Paramhans Marg,

Mansarovar, JAIPUR-302020

Leave a Reply