STRATEGIES FOR THE LIFE INSURANCE AGENTS TO ACHIEVE TRIUMPH IN SELLING POLICIES

INTRODUCTION:

Strategy is a term that comes from the Greek word ‘strategia’, meaning ‘generalship.’ In the military, strategy often refers to maneuvering troops into position before the enemy is actually engaged. In this sense, strategy refers to the deployment of troops. Once the enemy has been engaged, attention shifts to tactics. Here, the employment of troops is central. Substitute ‘resources’ and the transfer of the concept to the business world begin to take form. Corporate strategy is the pattern of decisions in a company that determines and reveals its objectives, purposes or goals; produces the principal policies and plans for achieving those goals and defines the range of business the company is to pursue; the kind of economic and human organization it is or intends to be and the nature of the economic and non-economic contribution it intends to make to its shareholders, employees, customers, and communities. Noted experts on ‘Business Strategy’ suggested that adopting the concept of strategy from military use for business was easy because very little change is required to be adopted in style. In business, as in the military, strategy bridges the gap between policy and tactics. Together, strategy and tactics bridge the gap between ends and means. Now let us focus on specific requirement of an agent as detailed below: Life Insurance agents require –- To become more professional as per the need of current market of too many insurers.

- To obtain better returns for the resources invested by them.

- Their goal setting require :-

- Increase in Business;

- Increase in Commission income;

- Increase in area of coverage;

- Increase in products variety sold;

- Target prospect in professional manner.

- Their action plan require :-

- Setting clear time-bound plan;

- Plan of Action should not include more than 5-6 issues;

- Should be measurable in terms of accomplishment;

- Spell out specific terms, conditions, rules & regulations adequately to the prospects.

SPECIFIC STRATEGIES FOR LIFE INSURERS:

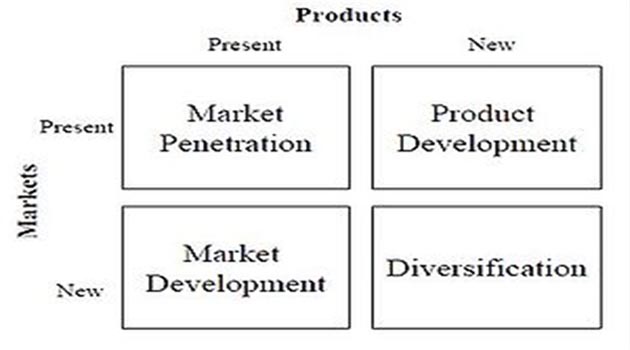

PROPER CUSTOMER SEGMENTATION: Any life insurance agent should do business across many customer segments and as because if he focuses on any one particular segment, he faces the same risk as faced by his customer segment. Therefore, he should have a basket of mixed customer segments. For example, if a particular agent works only among the diamond market customers in Mumbai then whenever the diamond market goes into a recession or faces any market challenge, the agent will also face a similar situation and his business will be affected directly. An agent should not have more than 20 per cent of his customer from any particular segment. This will expose him to only a 20 per cent risk which can be easily worked around. MARKET PENETRATION STRATEGY: Philip Kotler has given a very beautiful marketing model called Ansoff’s Matrix which is diagrammatically reproduced below: Ansoff matrix is a strategic marketing planning tool (it is named after its inventor, Igor Ansoff, the father of strategic management, and first published in 1957 in Harvard Business Review) that links a firm’s marketing strategy with its general strategic direction and presents four alternative growth strategies as a table (matrix). These strategies are seeking growth in all the four parameters: (1) Market penetration: by pushing existing products in their current market segments; (2) Market developments: by developing new markets for the existing products. (3) Product developments: by developing new products for the existing markets. (4) Diversification: by developing new products for new markets. The Ansoff’s Growth matrix is a tool that helps businesses decide their product and market growth strategy.Product-Market Growth Matrix:

The Ansoff Product-Market Growth Matrix is a marketing tool created by Igor Ansoff and first published in his article “Strategies for Diversification” in the Harvard Business Review (1957). The matrix allows marketers to consider ways to grow the business via existing and/or new products, in existing and/or new markets – there are four possible product/market combinations. This matrix helps companies decide what course of action should be taken given current performance. The matrix consists of four strategies:

The Ansoff Product-Market Growth Matrix is a marketing tool created by Igor Ansoff and first published in his article “Strategies for Diversification” in the Harvard Business Review (1957). The matrix allows marketers to consider ways to grow the business via existing and/or new products, in existing and/or new markets – there are four possible product/market combinations. This matrix helps companies decide what course of action should be taken given current performance. The matrix consists of four strategies:

- Market Penetration (existing markets, existing products): Market penetration occurs when a company enters/penetrates a market with current products. The best way to achieve this is by gaining competitors’ customers (part of their market share). Other ways include attracting non-users of your product or convincing current clients to use more of your product/service, with advertising or other promotions. Market penetration is the least risky way for a company to grow.

- Product Development (existing markets, new products): A firm with a market for its current products might embark on a strategy of developing other products catering to the same market (although these new products need not be new to the market; the point is that the product is new to the company). For example, McDonald’s is always within the fast-food industry, but frequently markets new burgers. Frequently, when a firm creates new products, it can gain new customers for these products. Hence, new product development can be a crucial business development strategy for firms to stay competitive.

- Market Development (new markets, existing products): An established product in the marketplace can be tweaked or targeted to a different customer segment, as a strategy to earn more revenue for the firm. For example, Lucozade was first marketed for sick children and then re-branded to target athletes. This is a good example of developing a new market for an existing product. Again, the market need not be new in itself; the point is that the market is new to the company.

- Diversification (new markets, new products): Virgin Cola, Virgin Megastores, Virgin Airlines, Virgin Telecommunications are examples of new products created by the Virgin Group of UK, to leverage the ‘Virgin Brand’. This resulted in the company entering new markets where it had no presence before.

Market Penetration (existing markets, existing products):

This involves increasing sales of an existing product and penetrating the market further by either promoting the product heavily or reducing prices to increase sales. Market penetration is the name given to a growth strategy where the business focuses on selling existing products into existing markets. Market penetration seeks to achieve four main objectives:- Maintain or increase the market share of current products – this can be achieved by a combination of competitive pricing strategies, advertising, sales promotion and perhaps more resources dedicated to personal selling

- Secure dominance of growth markets

- Restructure a mature market by driving out competitors; this would require a much more aggressive promotional campaign, supported by a pricing strategy designed to make the market unattractive for competitors

- Increase usage by existing customers – for example by introducing loyalty schemes A market penetration marketing strategy is very much about “business as usual”. The business is focusing on markets and products it knows well. It is likely to have good information on competitors and on customer needs. It is unlikely, therefore, that this strategy will require much investment in new market research.

- New geographical markets; for example exporting the product to a new country

- New product dimensions or packaging: for example

- New distribution channels

- Different pricing policies to attract different customers or create new market segments.

NEW PRODUCT DEVELOPMENT STRATEGY (existing markets, new products):

This is a new product to be marketed to our existing customers. Here we develop and innovate new product offerings to replace existing ones. Such products are then marketed to our existing customers. This often happens with the auto markets where existing models are updated or replaced and then marketed to existing customers. The organization develops new products to aim within their existing market, in the hope that they will gain more custom and market share. For Example, Sony launching the Play station 2 to replace their existing model. Product development is the name given to a growth strategy where a business aims to introduce new products into existing markets. This strategy may require the development of new competencies and requires the business to develop modified products which can appeal to existing markets. Quadrant II houses the ‘New Product Development Strategy’ that helps an agent to increase his/her revenue. This works on the premise that customers also need other financial products like health insurance, term insurance (as a co-lateral security for the house-building loan he/she requires to avail), various Life Insurance Products on pensions/ annuities and ULIPs (for his/her retirement & complete financial planning). If the agent cannot fulfill the need of his/her customer, there is a good chance that the customer will look to other agents who offer all the services under one roof to avoid dealing with different people. This will lead to the customer switching the loyalties. So it is very important that apart from life insurance the agent may also offer other products which are spin offs from his relationship with the customer. Here it is possible to earn additional income with a very little effort. It is very easy for an agent to double his/her income by using the product development strategy. Quadrant II strategy is a little more difficult than Quadrant I in terms of the effort versus the income potential. The existing customers’ situation may have changed. For example, his/her income may have increased, his/her family may have expanded, he/she could have got a promotion or other normal progression in life. All this will definitely create an environment of new needs for some insurance products. Generally every agent should focus on getting at least 80% of his/her business from his/her current market comprising his/her existing customers. This is the easiest way to increase his/her revenue. BUSINESS DIVERSIFICATION (new markets, new products) [DIVERSIFICATION AS A GROWTH STATEGY]: This is where we market completely new products to new customers. There are two types of diversification, namely related and unrelated diversification. Related diversification means that we remain in a market or industry with which we are familiar.The diversification can be divided again into horizontal, vertical and lateral diversification as below:

- The horizontal diversification is the extension of the production Programme.

- The vertical diversification is the sales stage stored by products pre order.

- The lateral diversification is the sales of completely new products, which within the range of the technology and marketing in no connection.

CONSOLIDATION:

Where the organization adopts a strategy of withdrawing from particular markets, scaling back on operations and concentrating on its existing products in existing markets – it is referred as consolidation. CONCLUSION: Using Ansoff matrix the agent may analyze and plan to meet customer needs and expectations. Facts that are worth considering by the agent in the way of self–introspection or a true feed back may include:- What strategy are agent’s Organization / agent’s Dept. is implementing now for its products/services – you the agent will need to place products/services in an appropriate quadrant?

- Is this the right strategy in terms of meeting customer needs and expectations?

- Is implementation effective?

Rational expectations of an agent:

Rational expectations are an assumption used in many contemporary macroeconomic models, and also in other areas of contemporary economics. Since most macroeconomic models today study decisions over many periods, the expectations of workers, consumers, and firms about future economic conditions are an essential part of the model. How to model these expectations has long been controversial, and it is well known that the macroeconomic predictions of the model may differ depending on the assumptions made about expectations. To assume rational expectations is to assume that agents’ expectations are correct on average. In other words, although the future is not fully predictable, agents’ expectations are assumed not to be systematically biased and use all relevant information in forming expectations of economic variables. This way of modeling expectations was originally proposed by John F. Muth (1961) and later became influential when it was used by Robert E. Lucas Jr. and others. Modeling expectations is crucial in theories like new classical macroeconomics, new Keynesian macroeconomics, and the efficient market hypothesis of contemporary finance, which study the dynamics of the economy over time. For example, negotiations between workers and firms will be influenced by the expected level of inflation, and the value of a share of stock is dependent on the expected future income from that stock. Rational expectations theory defines this kind of expectations as being identical to the best guess of the future (the optimal forecast) that uses all available information. However, without further assumptions, this theory of expectations determination makes no predictions about human behavior and is empty. Thus, it is assumed that outcomes that are being forecast do not differ systematically from the market equilibrium results. As a result, rational expectations do not differ systematically or predictably from equilibrium results. That is, it assumes that people do not make systematic errors when predicting the future, and deviations from perfect foresight are only random. In an economic model, this is typically modeled by assuming that the expected value of a variable is equal to the value predicted by the model, plus a random error term representing the role of ignorance and mistakes. For example, suppose that P is the equilibrium price in a simple market, determined by supply and demand. The theory of rational expectations says that the actual price will only deviate from the expectation if there is an ‘information shock’ caused by information unforeseeable at the time expectations were formed. In other words ex ante the actual price is equal to its rational expectation, P: in this case, P = P* + e and E(P) = P* Where, P* is the rational expectation and e is the random error term, which has an expected value of zero, and is independent of P*. Rational expectations theories were developed in response to perceived flaws in theories based on adaptive expectations. Under adaptive expectations, expectations of the future value of an economic variable are based on past values. For example, people would be assumed to predict inflation by looking at inflation last year and in previous years. Under adaptive expectations, if the economy suffers from constantly rising inflation rates (perhaps due to government policies), people would be assumed to always underestimate inflation. This may be regarded as unrealistic – surely rational individuals would sooner or later realize the trend and take it into account in forming their expectations? Further, models of adaptive expectations never attain equilibrium, instead only moving toward it asymptotically. The hypothesis of rational expectations addresses this criticism by assuming that individuals take all available information into account in forming expectations. Though expectations may turn out incorrect, they will not deviate systematically from the expected values. Rational expectations theory is the basis for the efficient market hypothesis (efficient market theory). If a security’s price does not reflect all the information about it, then there exist “unexploited profit opportunities”: someone can buy (or sell) the security to make a profit, thus driving the price toward equilibrium. In the strongest versions of these theories, where all profit opportunities have been exploited, all prices in financial markets are correct and reflect market fundamentals (such as future streams of profits and dividends). Each financial investment is as good as any other, while a security’s price reflects all information about its intrinsic value. The hypothesis is often criticized as an unrealistic model of how expectations are formed. First, truly rational expectations would take into account the fact that information about the future is costly. The “optimal forecast” may be the best not because it is accurate but because it is too expensive to attain even close to accuracy. Further, the models of Muth and Lucas (and the strongest version of the efficient markets hypothesis) assume that at any specific time, a market or the economy has equilibrium (which was determined ahead of time), so that people from their expectations around this unique equilibrium. In fact, expectations would determine the nature of the equilibrium attained, reversing the line of causation posited by rational expectations theorists. A further problem relates to the application of the rational expectations hypothesis to aggregate behavior. It is well known that assumptions about individual behavior do not carry over to aggregate behavior (Sonnenschein-Mantel-Debreu Theorem). The same holds true for rationality assumptions: Even if all individuals have rational expectations, the representative household describing these behaviors may exhibit behavior that does not satisfy rationality assumptions (Janssen 1993). Hence the rational expectations hypothesis, as applied to the representative household, is unrelated to the presence or absence of rational expectations on the micro level and lacks, in this sense, a microeconomic foundation. It can be argued that it is difficult to apply the standard efficient market hypothesis (efficient market theory) to understand the stock market bubble that ended in 2000 and collapsed thereafter. (Advocates of Rational Expectations may say that the problem of ascertaining all the pertinent effects of the stock-market crash is a great challenge). Some economists now use the adaptive expectations model, but then complement it with ideas based on the rational expectations theory. For example, an anti-inflation campaign by the Central bank is more effective if it is seen as “credible,” i.e., if it convinces people that it will “stick to its guns”. The bank can convince a person to lower their inflationary expectations, which implies less of a feedback into the actual inflation rate. Those studying financial markets similarly may apply the efficient-market’s hypothesis but keeping the existence of exceptions in mind.Author : Anabil Bhattacharya

Published : Life Insurance Today, September 2018

Leave a Reply