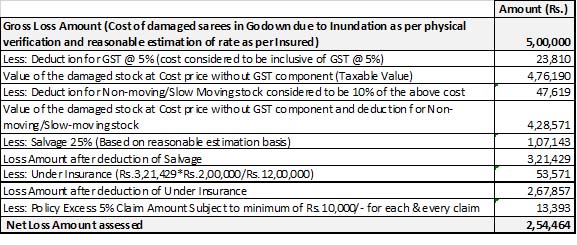

Loss assessment under a Fire Insurance Policy and impact of GST

The end consumer always takes the entire burden of indirect taxes in a tax structure. Goods and Services Tax (GST) in which as many as 17 different central and state taxes and 23 different cesses got subsumed with effect from 01.07.2017 is also a form of value added tax and the major form of indirect taxes in our country today apart from Basic Customs Duty which prevails only on import of goods. Seamless movement of Input Tax Credit (ITC) is possible in the GST regime on supply of goods and services and a taxable person registered under GST law is eligible for ITC unless it is restricted for him to avail otherwise.

As per Rule 56 (2) of the Central GST Rules, 2017, every registered person has to maintain the accounts of stock in respect of goods received and supplied by him, and such accounts shall contain particulars of the opening balance, receipt, supply, goods lost, stolen, destroyed, written off or disposed of by way of gift or free sample and the balance of stock including raw materials, finished goods, scrap and wastage. However, this provision is not applicable to a taxable person who is either a trader or a manufacturer and has opted for Composition scheme.

A Fire Insurance Policy can cover input goods which may be in form of stocks (raw material, work-in-progress, finished goods, consumables, stores and spares etc.) and capital goods in form of plant and machinery, furniture and fixture, computer, electrical installation etc. Whenever there is an inward supply of either input or capital goods, a taxable person is eligible for ITC which in fact reduces his tax cost. He avail such eligible ITC and utilize the same against off-setting his GST liability which may be in form of Integrated GST (IGST), Central GST (CGST) of State GST (SGST). Of course, ITC available in form of CGST and SGST are not allowed to be utilized against each other for discharging tax liability. However, ITC can be availed by the taxable person by filing GSTR 3B and upon fulfilment of certain conditions which are as under:

Conclusion

It is of course advisable to an Insured to reverse the ITC in case there is any loss/ destruction/ damage/ theft of stock as he can get the benefit of the same from the Insured. Tax Department or GST Auditor if come across the same at a subsequent stage, then there will be a liability/demand along with interest and penalty which will be a very costly affairs for an insured as a taxable person. Of course, understanding of this provision and consequence thereof is required along with filing the GSTR 3B and submission of the same before the Underwriter before assessment of such loss.

Conclusion

It is of course advisable to an Insured to reverse the ITC in case there is any loss/ destruction/ damage/ theft of stock as he can get the benefit of the same from the Insured. Tax Department or GST Auditor if come across the same at a subsequent stage, then there will be a liability/demand along with interest and penalty which will be a very costly affairs for an insured as a taxable person. Of course, understanding of this provision and consequence thereof is required along with filing the GSTR 3B and submission of the same before the Underwriter before assessment of such loss.

- There must be a valid and GST compliant Tax Invoice available with the taxable person;

- The goods must have been supplied to the taxable person;

- The Supplier must have filed GST Return 1;

- The Supplier must have paid the GST either by utilizing his ITC or by cash;

- The Supplier must have been paid within 180 days from the date of Invoice by the taxable person;

- If the goods are lost; or

- the goods are destroyed; or

- the goods are stolen;

- the goods are written off;

Conclusion

It is of course advisable to an Insured to reverse the ITC in case there is any loss/ destruction/ damage/ theft of stock as he can get the benefit of the same from the Insured. Tax Department or GST Auditor if come across the same at a subsequent stage, then there will be a liability/demand along with interest and penalty which will be a very costly affairs for an insured as a taxable person. Of course, understanding of this provision and consequence thereof is required along with filing the GSTR 3B and submission of the same before the Underwriter before assessment of such loss.

Author

Shiba Prasad Padhi

Research Scholar, Fakir Mohan University, Balasore, Odisha

Published : The Insurance Times, January, 2019 issue.

Leave a Reply