THE “IGMS”: SO FAR SO GOOD, BUT NOT GOOD ENOUGH

Happy customers are the key ingredient for a successful recipe for all companies; the same holds true for the insurance industry. If a policyholder is unhappy either with the service that he gets from the insurance company, or with the product itself, or for any other reason; then his grievances must be tended to with utmost priority. Effective Grievance Management of Insurance Sector pertaining to Life and Non life products of different insurer companies are geographic hectic and intense in nature. Administration of these grievance related issues in geographic format would certainly stabilize towards a standard effective mechanisms on IGMS project management front in delivering the desired services to policy holders towards goals of IGMS program by and large in a common frame work. Further it helps IRDA to gauge the effectiveness of grievance redressal systems of insurers in the industry. IRDAI has launched the Integrated Grievance Management System (IGMS). Apart from creating a central repository of industry-wide insurance grievance data, IGMS is a grievance redress monitoring tool for IRDAI. Policyholders who have grievances should register their complaints with the Grievance Redress Channel of the Insurance Company first. If policyholders are not able to access the insurance company directly for any reason, IGMS provides a gateway to register complaints with insurance companies.

IRDAI is the monitoring body of all insurance companies in India and for this reason, it is often referred to as the watchdog. In short, what the Reserve Bank of India (RBI) is to banks, IRDA is to Insurance Companies. It governs all Non-Life, which includes health insurance, travel insurance, motor insurance, home insurance etc, Life Insurance Companies, Reinsurance companies and looks after the interest of the insurance industry as a whole. IGMS is a comprehensive solution which not only has the ability to provide a centralised and online access to the policyholder but complete access and control to IRDAI for monitoring market conduct issues of which policyholder grievances are the main indicators. IGMS has the ability to classify different complaint types based on pre-defined rules. The system has the ability to assign, store and track unique complaint IDs. It also sends intimations to various stakeholders as required, within the workflow. The system has defined target Turnaround Times (TATs) and measures the actual TATs on all complaints. IGMS sets up alerts for pending tasks nearing the laid down Turnaround Time. The system automatically triggers activities at the appropriate time through rule based workflows. The system enables real time access to all users at all times and from any location.

It has also a mechanism to capture complaints received in physical as well as email form or voice calls received by IRDA Grievance Call centre (IGCC). The IGCC also provides details of the redressal systems of insurance companies whenever policyholders require them. Further, the IGCC also educates policyholders about the Insurance Ombudsman who provides a channel for fair disposal of complaints falling within the jurisdiction laid down.

It has also a mechanism to capture complaints received in physical as well as email form or voice calls received by IRDA Grievance Call centre (IGCC). The IGCC also provides details of the redressal systems of insurance companies whenever policyholders require them. Further, the IGCC also educates policyholders about the Insurance Ombudsman who provides a channel for fair disposal of complaints falling within the jurisdiction laid down.

IRDA should institute senior citizen-centric nodal officers at the director-level, and also at insurance companies, to specifically address all elder-related issues. Part of the solution would also be a changed stance from IRDA. IRDA’s job is not to focus on individual complaints; but it does take up such cases on a random basis and investigates insurance companies to protect the insured. IRDA’s approach is to put systems in place and see how they work and the corrections that need to be done in the processes. It means individual complaints may not get solved by IRDA’s IGMS. Consumers still have to go to the insurance ombudsman, consumer court or civil court. The advantages of ombudsman are no cost to the insured and binding decision on insurance companies. While the insurance ombudsman is good option, there is often a delay in getting a hearing. It can range from six months to one year after making a complaint. In some places the ombudsman’s post gets filled after being vacant for over nine months. This increases the backlog of complaints.

The Bombay High Court suggested that IRDA should empower the insurance ombudsman to levy compensatory or penal costs on insurance companies for repudiating insurance claims on flimsy grounds. It is now up to IRDA to to see strict observance of its guidelines. Still, given the amount of mis-selling and fraud, a lot needs to change to improve customer satisfaction including empowering the insurance ombudsman to levy penalty on insurers. It is extremely difficult to justify the reasons for the same particularly with IRDA members having so much of interactions with these insurers by participation at every conceivable events and venues sponsored by these companies to promote their cause. IRDAI has to ensure that proper checks and controls are put in place to protect the insurance policyholder. At times, even a letter written to CEO, remains unanswered. There is a need to put a system of public accountability. They do it because they believe aam-admi (common-man) does not have power and cannot face litigation. Let there be transparency in every aspect so that end of the day people get justice, failing which insurance companies will continue to under deliver.

IRDA should institute senior citizen-centric nodal officers at the director-level, and also at insurance companies, to specifically address all elder-related issues. Part of the solution would also be a changed stance from IRDA. IRDA’s job is not to focus on individual complaints; but it does take up such cases on a random basis and investigates insurance companies to protect the insured. IRDA’s approach is to put systems in place and see how they work and the corrections that need to be done in the processes. It means individual complaints may not get solved by IRDA’s IGMS. Consumers still have to go to the insurance ombudsman, consumer court or civil court. The advantages of ombudsman are no cost to the insured and binding decision on insurance companies. While the insurance ombudsman is good option, there is often a delay in getting a hearing. It can range from six months to one year after making a complaint. In some places the ombudsman’s post gets filled after being vacant for over nine months. This increases the backlog of complaints.

The Bombay High Court suggested that IRDA should empower the insurance ombudsman to levy compensatory or penal costs on insurance companies for repudiating insurance claims on flimsy grounds. It is now up to IRDA to to see strict observance of its guidelines. Still, given the amount of mis-selling and fraud, a lot needs to change to improve customer satisfaction including empowering the insurance ombudsman to levy penalty on insurers. It is extremely difficult to justify the reasons for the same particularly with IRDA members having so much of interactions with these insurers by participation at every conceivable events and venues sponsored by these companies to promote their cause. IRDAI has to ensure that proper checks and controls are put in place to protect the insurance policyholder. At times, even a letter written to CEO, remains unanswered. There is a need to put a system of public accountability. They do it because they believe aam-admi (common-man) does not have power and cannot face litigation. Let there be transparency in every aspect so that end of the day people get justice, failing which insurance companies will continue to under deliver.

References:

HOW IGMS WORKS:

If you are dissatisfied with your insurance policy, you would approach your insurance company and lodge a complaint. And to make sure that insurers tend to complaints and resolve them quickly, the IRDAI set up the Integrated Grievance Management System (IGMS) in 2011. It works like a central repository of all consumer complaints received by life insurance and non-life insurance companies. It is an online consumer complaints registration system and all insurers have integrated their online complaint logging systems to IGMS, which is maintained by IRDAI. Every insurer is required to have a grievance management system and policy approved by IRDAI.The system flows like this:- A policyholder needs to login in toigms.irda.gov.in and create a profile for registering a complaint.

- Policyholders can register one or more complaints.

- Details of the complaint are passed on to respective insurance company or companies.

- While registering the complaint, the policyholder will get a list of branch offices of the insurance company.

- A confirmation email along with IRDA token no is sent to the customer, which will be used by IRDA and Insurance Company for tracking of the complaint through IGMS.

- If the complainant is not satisfied with the resolution provided by Insurer, he can escalate the complaint for a review by IRDA for a potential violation of Regulations.

- All the transactions between the Insurer, Insured and Remarks by IRDA are visible to the complainant.

SCOPE OF IGMS:

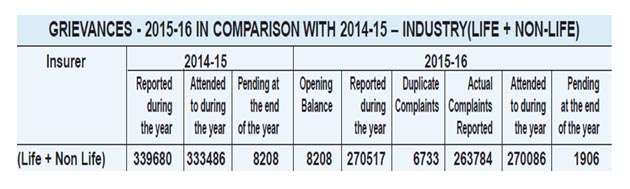

Its mandate is restricted as IRDAI does not adjudicate on individual complaints through IGMS. The idea is to effect speedy disposal of complaints and have a repository to help IRDAI track nature of complaints and timelines. There is data on types of complaints. The latest is of FY15. In three years, complaints regarding unfair business practices remained on top, followed by policy servicing and claim for life insurers. A complaint registered through IGMS will flow to the insurer’s system as well as the IRDAI repository. Updating of status will be mirrored in the IRDAI system. IGMS enables generation of reports on all criteria like ageing, status, nature of complaint and any other parameter that is defined. The Integrated Grievance Management System (IGMS) is an online consumer complaints registration system created by IRDA. All insurance companies have integrated their online complaint logging systems to the IGMS maintained by IRDA. The Complaint Registration Process involves TWO SIMPLE steps: Step 1:Register yourself by entering your details Step 2: Register your complaint and view its status First approach the insurer’s Grievance Redressal Mechanism. This is given in your insurance policy document. You can also get the Grievance Redressal Mechanisms of all insurers at the following links. Once the policy holder registers in to IGMS then details of complaint are passed on to respective insurance companies. Policy holder can see the details of the branch offices of the insurance company while registering the complaint. Policy holder receives the confirmation email after registering the complaint along with IRDA token no which will be used by IRDA and Insurance Company for tracking of the complaint through IGMS. A complaint registered through IGMS flows to the insurer’s system as well as the IRDA repository.THE REDRESSAL FRAMEWORK:

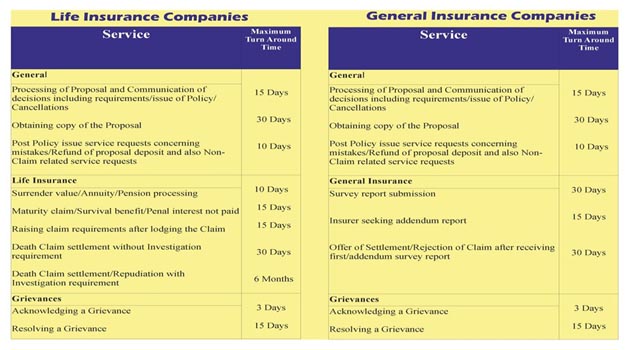

IRDAI’s regulations stipulate the Turnaround Times (TAT) for various services that an insurance company has to render to you, the consumer. These are part of the IRDA Protection of Policyholders’ Interests (PPHI) Regulations 2002. Insurance companies are also required to have an effective Grievance Redressal Mechanism and IRDAI has created the guidelines for that too. Here are the TATs for an insurance company to deal with various types of complaints:

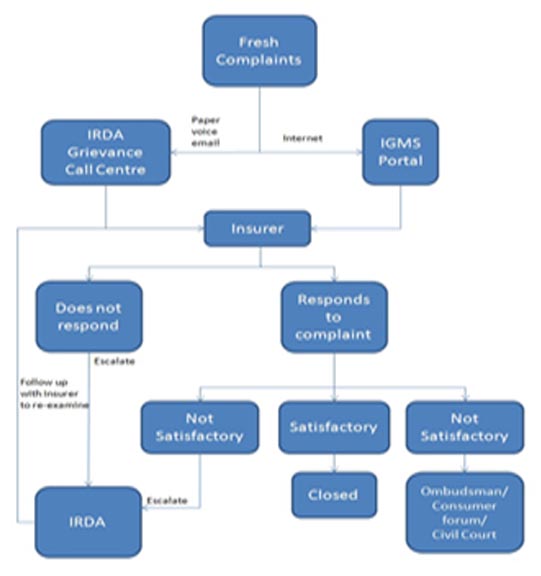

GRIEVANCE FLOWCHART:

IRDAI has stipulated that each insurance company should codify and make public the way it will deal with consumer complaints and resolve them. The Regulator has provided links to the Grievance Redressal Policies of all the Life insurance Companies and Non-Life Insurance Companies To enable effective monitoring of Policyholder protection Regulations and Grievance Guidelines and Turnaround times thereby mandated, as well as to create a central repository of industry-wide insurance grievances’ data, IRDA has implemented IGMS which is a comprehensive solution, not only has the ability to provide a centralized and online access to the policyholder but complete access and control to IRDA for monitoring market conduct issues of which policyholder grievances are the main indicators. It uses Web interface to ensure that it is accessible at all places and is on real time.

It has also a mechanism to capture complaints received in physical as well as email form or voice calls received by IRDA Grievance Call centre (IGCC). The IGCC also provides details of the redressal systems of insurance companies whenever policyholders require them. Further, the IGCC also educates policyholders about the Insurance Ombudsman who provides a channel for fair disposal of complaints falling within the jurisdiction laid down.

IRDA GRIEVANCE CALL CENTRE:

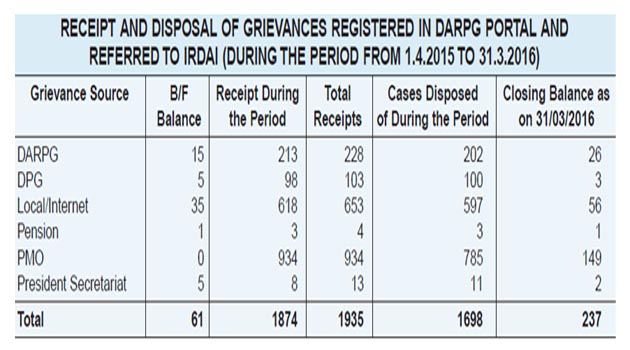

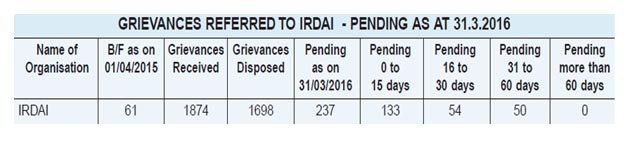

Thus IGMS provides a standard platform to all insurers to resolve policyholder grievances and provides IRDAI with a tool to monitor the effectiveness of the grievance redress system of insurers. There is an alternative channel for you to register your complaint about your insurance policy or find out its status. Policyholder can call the IRDA Grievance Call Centre. Tall free numbers are provided to register the grievance on all working days. A policyholder can make optimum use of this system by giving accurate information about the complaint like the policy number, name of the insurer, complainant’s contact details etc. It is useful to keep the policy document ready while registering the complaint online. You can also approach IGMS directly by logging into igms.irda.gov.in and registering your complaint or calling the toll free number to register your complaint into the insurer’s system. Policyholder can also email to [email protected]. But IRDAI encourages policyholders to approach the insurer first. Apart from the complaints registered in the IGMS Portal of IRDAI, Complaints registered in DARPG Portal against insurers are also referred to IRDAI. IRDAI regularly accesses the portal of the DARPG and ensures that complaints relating to the insurance sector are downloaded and necessary action to get them examined by the insurers is taken.

NO APPELLATE JURISDICTION:

The entire process have specified turnaround times as mandated by the regulator and hence customers get a response with the stipulated time frame. IGMS help address the needs of thousands of dissatisfied or aggrieved customers, while at the same time ensure that insurance companies provide an appropriate solution. IRDA only monitors the grievance redressal process of the insurance companies and gives appropriate directions for the protection of interest of policyholder. IRDA exercises no appellate jurisdiction over such disputes, it only guides the aggrieved customers to approach proper channel for redressal of their grievance. IRDA is responsible for healthy development of Insurance business where the customers get their due share. Sadly, there are areas where the customer is in the receiving end.

SCOPE FOR IMPROVEMENT:

IRDAI came out with many initiatives including the integrated grievance management system (IGMS) to help with consumer redressal. It facilitates online registration of policyholders’ complaints and track the status of their complaints. It gives insurance regulator a tool to monitor the effectiveness of the grievance redressal system of insurers. IRDA can have real-time monitoring and tracking details of all grievances lodged with all insurers, along with their disposal status. It gives mirroring of the complaints database of the insurers through the IRDA portal. However, customer grievance redressal has not drastically improved even after introduction of new system. There is a need for proactive action against insurers and for IRDA to stop being just a facilitator.

IRDA should institute senior citizen-centric nodal officers at the director-level, and also at insurance companies, to specifically address all elder-related issues. Part of the solution would also be a changed stance from IRDA. IRDA’s job is not to focus on individual complaints; but it does take up such cases on a random basis and investigates insurance companies to protect the insured. IRDA’s approach is to put systems in place and see how they work and the corrections that need to be done in the processes. It means individual complaints may not get solved by IRDA’s IGMS. Consumers still have to go to the insurance ombudsman, consumer court or civil court. The advantages of ombudsman are no cost to the insured and binding decision on insurance companies. While the insurance ombudsman is good option, there is often a delay in getting a hearing. It can range from six months to one year after making a complaint. In some places the ombudsman’s post gets filled after being vacant for over nine months. This increases the backlog of complaints.

The Bombay High Court suggested that IRDA should empower the insurance ombudsman to levy compensatory or penal costs on insurance companies for repudiating insurance claims on flimsy grounds. It is now up to IRDA to to see strict observance of its guidelines. Still, given the amount of mis-selling and fraud, a lot needs to change to improve customer satisfaction including empowering the insurance ombudsman to levy penalty on insurers. It is extremely difficult to justify the reasons for the same particularly with IRDA members having so much of interactions with these insurers by participation at every conceivable events and venues sponsored by these companies to promote their cause. IRDAI has to ensure that proper checks and controls are put in place to protect the insurance policyholder. At times, even a letter written to CEO, remains unanswered. There is a need to put a system of public accountability. They do it because they believe aam-admi (common-man) does not have power and cannot face litigation. Let there be transparency in every aspect so that end of the day people get justice, failing which insurance companies will continue to under deliver.

Author

JAGENDRA KUMAR

Ex. CEO, Pearl Insurance Brokers 71/143, “Ramashram” Paramhans Marg, Mansarovar, JAIPUR-302020

References:

- IRDA Annual Report 2015-16 ( Data contents)

- http://www.policyholder.gov.in/integrated_grievance_management.aspx

- http://www.igms.irda.gov.in/

- http://www.moneylife.in/article/irdarsquos-consumer-redress-system-1-lot-of-scope-for-improvement/31236.html

- http://economictimes.indiatimes.com

- Newspapers & Journals

Leave a Reply