DIGITAL PAYMENT REVOLUTION IN INDIAN LIFE INSURANCE SPACE- SYNOPSIS

Abstract

Insurance Companies are coping with technological innovation to remain competitive which will boost profitability, enhance customer delight, streamline operations and reduce costs. Gone were the days when customer rush to a branch and remits the premium .Now there are manifold ways where customer can pay the premium. Also the KYC (Know Your Customer) process has been streamlined with the dawn of Aadhar as the proof of identity. We are into an era of E-KYC where customers can complete KYC Process by just displaying Aadhar Card to the sales person who in turn scans the Aadhar to retrieve info from UIDAI server. With wide assortment in digital payment gateways, Insurance companies are transmuting business from push to pull business. KEY WORDS: BHIM,AEPS, BANKING CARDS, ONLINE PORTALS|

DR.R.RADHIKA, RESEARCH GUIDE RAMESH KUMAR SATULURI, RESEARCH SCHOLAR GITAM University, Hyderabad. |

INTRODUCTION Technological innovations are disrupting the way business is carried across spectrums. Insurance industry is no exception to this digital revolution and metamorphosis. One of the major segments influencing entire sales process is Millennials of this decade. Millennials are fast entering their major spending pace. Growing up in the current generation they have their own expectations and priorities. They are tech savvy and obsessed with Smart Phone and usage of internet. This is surely going to change the entire sales process.

- Total Transaction Value in the Digital Payments segment amounts to US$51,756m in 2018

- Total Transaction Value is expected to show an annual growth rate (CAGR 2018-2022) of 17.4% resulting in the total amount of US$98,309m by 2022

- The market’s largest segment is Digital Commerce with a total transaction value of US$51,463m in 2018.

Source: www.statista.com

Nearly 46 crore population have become internet savvy which is driving the entire payment behavior and hence we see huge spike on digital payments. OBJECTIVES OF THE STUDY- To understand the impact of Digital Payments in India in Life Insurance Space

- To suggest measures in improving Digital Payment Revolution

- To comprehend future trends in Digital Payments

- Limited time to review the future trends in Digital Payments

- Measures adopted by Insurance Companies are fast changing and dynamic.

- Research is limited to reviewing literature and best practices in Indian Life Insurance Industry

- BRITTO RAMESH KUMAR(2010)1 in his topic “AN ARCHITECTURE FOR SECURE MOBILE PAYMENT SYSTEM USING PUBLIC KEY INFRASTRUCTURE” opined that the success of proposed architecture is dependent on Multi-factor authentication scheme and End-to-end data security which is vital for Digital Payments revolution to take off.

- SANJAY MATHUR(2012)2 in his topic named “CUSTOMER RELATIONSHIP MANAGEMENT AND DIGITAL PAYMENTS IN DEVELOPING COUNTRIES” was studying about various aspects of Digital Payments and also recommended steps to be taken to ensure data security and privacy.

- CHITRA KIRAN(2013)3 in topic “DESIGN AND DEVELOPMENT OF PROCESS ORIENTED BUSINESS TRANSACTION FOR MOBILE COMMERCE” discussed about the fundamentals of mobile commerce and its various aspects with respect to process oriented architecture, encompasses issues in wireless network with respect to mobile payment systems. r presented a novel approach of process oriented architecture for secure mobile commerce framework using uniquely designed hybrid mobile adhoc routing protocols using reactive and proactive type in real time test-bed

- Himaghna Dey Sarkar(2018)4 in article “Digital Payments In India: Current Challenges And Growth Prospects” opined that the Indian economy continues to be heavily reliant on cash and Digital payment systems are heavily reliant on smartphones that are enabled with data connections, NFC, Bluetooth etc. Author states that Government efforts towards the elevation of these cutting-edge, novel technologies and their systematic penetration among the masses will inevitably lead to a boundlessly prolific cashless economy.

- Satyen Kothari(2018)5 in article “ 5 reasons why consumers still don’t use digital payments” emphasized that India is well on its way to becoming a trillion dollar digital economy and government departments are actively driving the blueprint to achieve this. However, we aren’t there yet. It is because of habit, trust, transparency and pervasiveness.

- Vivek Kumar Singh(2018)6 in his article “How Digital Payment Technologies Are Replacing Cash in India” opined that cash as a payment instrument is still dominating the payment space, and digital payment usage is still limited to a small, largely urban and technologically enabled audience. Author further states that delving deeper into the payment practices and infrastructures in the country, one can clearly see that there is an overall technological disconnect that is ensuring that cash remains king.

While the Online Portal contributes to only 2.3% of the total sales the spending pattern and behavior of Gen X and Y population and Web Aggregators as a channel is surely going to take the participation to the next level in the days to come.

Every insurance company is capitalizing on online portals with payment gateways for customers to remit bot the new and renewal premiums. Also quite a lot portal went one step further in enabling financial planning as a tool to ascertain the shortfall in life stage goals and suggest an appropriate plan for the customer. Furthermore insurance companies have also placed information on Maturity amount and the ways and means it can be re deployed leading to cross sell and up sell.

UPI TRANSACTIONS

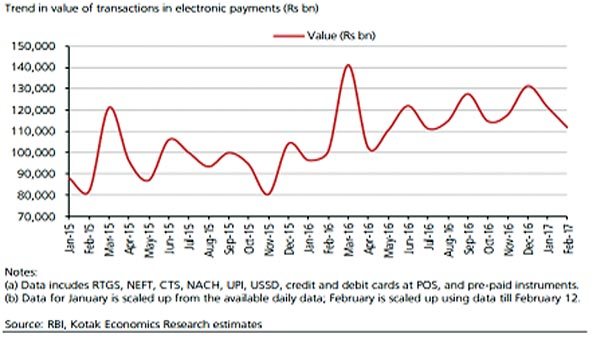

Unified Payments Interface (UPI) is a technology that links manifold bank accounts into a distinct mobile application amalgamating numerous banking features, flawless fund directing and merchant payments gateway in one fold. We are witnessing a steady increase in the transaction volume between January’15 and February’17.

While the Online Portal contributes to only 2.3% of the total sales the spending pattern and behavior of Gen X and Y population and Web Aggregators as a channel is surely going to take the participation to the next level in the days to come.

Every insurance company is capitalizing on online portals with payment gateways for customers to remit bot the new and renewal premiums. Also quite a lot portal went one step further in enabling financial planning as a tool to ascertain the shortfall in life stage goals and suggest an appropriate plan for the customer. Furthermore insurance companies have also placed information on Maturity amount and the ways and means it can be re deployed leading to cross sell and up sell.

UPI TRANSACTIONS

Unified Payments Interface (UPI) is a technology that links manifold bank accounts into a distinct mobile application amalgamating numerous banking features, flawless fund directing and merchant payments gateway in one fold. We are witnessing a steady increase in the transaction volume between January’15 and February’17.

UPI also pops up payment requests from concerned parties which can be acknowledged and paid as per the obligation. Insurance companies are creating virtual payment address to facilitate customers remit the premium. Companies progressed further to send payment requests to countless customer bases and with a click of the button they could renew their policies. Virtual payment address is an innovation which lessens the burden of remembering account number and IFSC code.

These technologies not only permit customers to remit the premium but will also aid companies to connect to their innumerable renewal base in one fold.

BHIM (BHARAT INTERFACE FOR MONEY)

BHIM allows users to transfer or accept money from other UPI payment addresses or scanning QR code or account number number with IFSC code or MMID (Mobile Money Identifier) Code to users who do not have a UPI-based bank account.[5]. Aadhaar Authentication should be done by merchant using any Registered device viz, Micro-ATM/POS, mPOS, Kiosk/Tablet/Mobile Handset.

within 10 days of the launch BHIM app had 1 crore downloads from Android Play Store and over 2 million transactions across the UPI (Unified Payment Interface) and USSD (Unstructured Supplementary Service Data) platforms.

With respect to Insurance Industry every company has got a Rural and Social Obligation to be fulfilled. All the Insurance Companies who complete their 10yrs of operation should meet 20% premium target for Rural and 50000 lives for Social as part of their obligation. This will ensure that companies are penetrating deeper in Rural Areas. For the year 2016-17 Life Insurers along underwrote 60.45 lakh policies in the rural sector viz. 22.9 percent of the new individual policies.

It is surely going to have positive impact on insurance companies since most of them are penetrating in rural markets and it will aid companies to reach all their customers who primarily operate feature phones. Also Insurance companies are seriously contemplating to send payment request to all their renewal customers thus establishing connectivity. The other possibility is depositing their maturity/surrender/withdrawal amount through BHIM. The current limit on money transfer may hold companies to go ahead with the plan but surely in the days to come we would expect them to really encash the situation.

The only constraint as of now would be restricting the payout to Rs.10000 which limits the capacity of insurance companies use this medium of payment.

AEPS THROUGH MICRO ATM

Aadhaar Enabled Payment System (AEPS) is a system developed by the National Payments Corporation of India (NPCI) that allows people to carry out financial transactions on a Micro-ATM by furnishing just their Aadhaar number and verifying it with the help of their fingerprint/iris scan.

Micro ATM is the swiping machine which is carried by business correspondent and allows the user to deposit or withdraw cash from the BC. It is effectively substituting a bank and aids us with wider penetration.

It is surely going to be a big help for insurance companies especially when they do not have enough branches in rural areas but however would want to source business from the untapped marked. Companies which have wider customer base in rural areas would be the most to benefit from Micro ATMs which allows them to have renewed focus on maintaining higher persistency levels.

DIGITAL WALLETS

While digital wallet companies such as Paytm, MobiKwik, Free Charge, Ola Money, and Amazon Pay gained massive ground, Alibaba-backed Paytm, India’s top digital payment firm, hit 100 million downloads on Google Play Store in December’17

Transactions recorded by prepaid payment instruments (PPI)—mobile wallets, prepaid cards, and paper vouchers—rose around 4% from Rs14,959 crore in February’17 to Rs15,521 crore ($2.26 billion) in May’17, Reserve Bank of India (RBI) data show. This was a result of merchants pushing aggressively with better offers and keeping the process simple.

While Govt. is aggressively pushing digital payments mobile wallets started tying up with General Insurance Companies to offer Insurance services.

Paytm, India’s largest mobile wallet app with more than 200 million users has come up with a new level of security system for its users: Wallet Insurance.

Also Mobile Wallets have tied up with Insurance Companies where the renewals can be paid through Wallets. Users who have completed e-kyc will enjoy a wallet balance of 1 lakh.

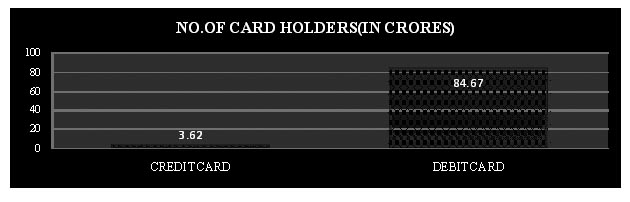

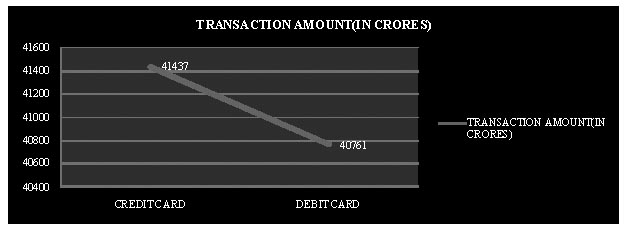

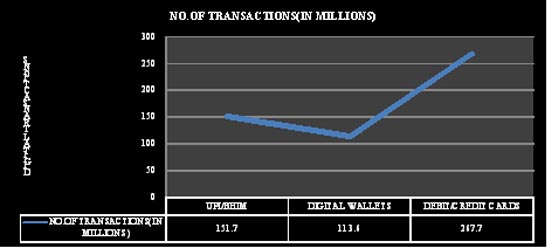

In January 2018, UPI/BHIM registered 151.7 Mn transactions. Also the effect of demonetization is clearly visible with Digital Wallets clocking 113.6 Million transactions. However the major pie lies with the usage of Debit and Credit cards which reported 267.7 Million Transactions.

UPI also pops up payment requests from concerned parties which can be acknowledged and paid as per the obligation. Insurance companies are creating virtual payment address to facilitate customers remit the premium. Companies progressed further to send payment requests to countless customer bases and with a click of the button they could renew their policies. Virtual payment address is an innovation which lessens the burden of remembering account number and IFSC code.

These technologies not only permit customers to remit the premium but will also aid companies to connect to their innumerable renewal base in one fold.

BHIM (BHARAT INTERFACE FOR MONEY)

BHIM allows users to transfer or accept money from other UPI payment addresses or scanning QR code or account number number with IFSC code or MMID (Mobile Money Identifier) Code to users who do not have a UPI-based bank account.[5]. Aadhaar Authentication should be done by merchant using any Registered device viz, Micro-ATM/POS, mPOS, Kiosk/Tablet/Mobile Handset.

within 10 days of the launch BHIM app had 1 crore downloads from Android Play Store and over 2 million transactions across the UPI (Unified Payment Interface) and USSD (Unstructured Supplementary Service Data) platforms.

With respect to Insurance Industry every company has got a Rural and Social Obligation to be fulfilled. All the Insurance Companies who complete their 10yrs of operation should meet 20% premium target for Rural and 50000 lives for Social as part of their obligation. This will ensure that companies are penetrating deeper in Rural Areas. For the year 2016-17 Life Insurers along underwrote 60.45 lakh policies in the rural sector viz. 22.9 percent of the new individual policies.

It is surely going to have positive impact on insurance companies since most of them are penetrating in rural markets and it will aid companies to reach all their customers who primarily operate feature phones. Also Insurance companies are seriously contemplating to send payment request to all their renewal customers thus establishing connectivity. The other possibility is depositing their maturity/surrender/withdrawal amount through BHIM. The current limit on money transfer may hold companies to go ahead with the plan but surely in the days to come we would expect them to really encash the situation.

The only constraint as of now would be restricting the payout to Rs.10000 which limits the capacity of insurance companies use this medium of payment.

AEPS THROUGH MICRO ATM

Aadhaar Enabled Payment System (AEPS) is a system developed by the National Payments Corporation of India (NPCI) that allows people to carry out financial transactions on a Micro-ATM by furnishing just their Aadhaar number and verifying it with the help of their fingerprint/iris scan.

Micro ATM is the swiping machine which is carried by business correspondent and allows the user to deposit or withdraw cash from the BC. It is effectively substituting a bank and aids us with wider penetration.

It is surely going to be a big help for insurance companies especially when they do not have enough branches in rural areas but however would want to source business from the untapped marked. Companies which have wider customer base in rural areas would be the most to benefit from Micro ATMs which allows them to have renewed focus on maintaining higher persistency levels.

DIGITAL WALLETS

While digital wallet companies such as Paytm, MobiKwik, Free Charge, Ola Money, and Amazon Pay gained massive ground, Alibaba-backed Paytm, India’s top digital payment firm, hit 100 million downloads on Google Play Store in December’17

Transactions recorded by prepaid payment instruments (PPI)—mobile wallets, prepaid cards, and paper vouchers—rose around 4% from Rs14,959 crore in February’17 to Rs15,521 crore ($2.26 billion) in May’17, Reserve Bank of India (RBI) data show. This was a result of merchants pushing aggressively with better offers and keeping the process simple.

While Govt. is aggressively pushing digital payments mobile wallets started tying up with General Insurance Companies to offer Insurance services.

Paytm, India’s largest mobile wallet app with more than 200 million users has come up with a new level of security system for its users: Wallet Insurance.

Also Mobile Wallets have tied up with Insurance Companies where the renewals can be paid through Wallets. Users who have completed e-kyc will enjoy a wallet balance of 1 lakh.

In January 2018, UPI/BHIM registered 151.7 Mn transactions. Also the effect of demonetization is clearly visible with Digital Wallets clocking 113.6 Million transactions. However the major pie lies with the usage of Debit and Credit cards which reported 267.7 Million Transactions.

CONCLUSION

Recent survey conducted by Indian Express establishes the fact that Mobile Subscribers are going to reach 100 crore by 2020. This is phenomenal considering the data usage and also usage of feature phones in rural areas. With the inevitable change going to happen in the days to come we are going to witness higher penetration of digital payments in Insurance Space. Also the role of Online Portals and Web Aggregators cannot be undermined considering their reach and technological innovations.

More than the ease of operations and hassle free transactions to customers the fact remains most insurance companies are enhancing their bottom line (Profitability) through digital push and hence companies constituted digital boards internally to push the drive to zenith level.

REFERENCES

CONCLUSION

Recent survey conducted by Indian Express establishes the fact that Mobile Subscribers are going to reach 100 crore by 2020. This is phenomenal considering the data usage and also usage of feature phones in rural areas. With the inevitable change going to happen in the days to come we are going to witness higher penetration of digital payments in Insurance Space. Also the role of Online Portals and Web Aggregators cannot be undermined considering their reach and technological innovations.

More than the ease of operations and hassle free transactions to customers the fact remains most insurance companies are enhancing their bottom line (Profitability) through digital push and hence companies constituted digital boards internally to push the drive to zenith level.

REFERENCES

- https://www.irdai.gov.in/

- cashlessindia.gov.in/digital_payment_methods.html

- https://www.statista.com/outlook/296/119/digital-payments/india

- https://inc42.com/buzz

- https://www.entrepreneur.com/article/317733

- https://www.livemint.com/Technology/ACHEI1t6mB34c4xM5DiTsN/The-top-five-trends-in-Indias-digital-payment-landscape.html

- http://cashlessindia.gov.in/digital_payment_methods.html

- https://www.financialexpress.com/economy/modis-digital-india-at-play-digital-payments-triple-to-7-of-gdp-in-just-3-years-says-morgan-stanley/1194207/

Published : The Insurance Times, December, 2018

Leave a Reply