CONFLUENCE OF TECHNOLOGY ADVANCEMENT IS SET TO TRANSFORM MOTOR INSURANCE

The Indian government has recently passed the Motor Vehicle Amendment Bill 2016 in Lok Sabha. The Bill brings in major amendments to the 30-year-old Motor Vehicle Act. Certain amendments emphasise on third party (TP) cover offered under motor insurance policies. Third party insurance cover is compulsory by law since it addresses the crucial aspect of liability arising out of any damage to property or life due to an accident. The Bill seeks to get every stakeholder to take up more responsibility by distributing the liabilities to ensure accountability for road safety. Another significant reason that makes it pertinent for every individual to understand the implications of these newly proposed amendments is that it may not be your fault on the road but you can still get embroiled in a case involving damages to a third party. The Motor Vehicles Act 1988 makes it mandatory for any and all vehicles running on India’s roads to have a valid ‘liability only’ or ‘third party’ insurance cover. This means that the insurance policy purchased must cover any potential injuries and damage caused by one’s vehicle to another person or their property. Motor insurance is generally regarded as something central to road safety and responsibility, ensuring that compensation is provided to victims of road accidents. With the advent of AI in the insurance industry, insurance agents can now count on sophisticated systems for precision, efficiency, and flawless automation of existing customer-facing, underwriting and claims processes.

The use of technology has gained momentum during the year with the industry exploring and implementing technological advancements such as Blockchain, telematics and internet of things, among others. Automobile Insurance as an industry works on traditional methods. These methods are tried, tested and used by multiple insurers. They eventually get the same result: Time-consuming claim settlement process and fraudulent claims, Low levels of accuracy and manual processes are the main culprits for an automobile insurer. The confluence of technology advancements, big data and IoT is set to transform motor insurance for customers as well as for insurers. The customer experience of tomorrow will entail personalized offers, instantaneous paperless transactions, an intuitive digital experience, natural language interaction, and above all, peace of mind. IoT can be used to its full potential for accessing real-time information, understanding risks and taking preventative measures. Due to highly innovative nature and customised applications, in almost every industry, IoT has created a huge buzz around the globe. With advancements in the insurance industry and a positive shift in customers’ demands, the technology of the Internet of things is expected to rule this industry. With the help of, much appreciated, IoT the age-old methods followed in the insurance industry will witness a positive change. Insurers can create accurate products, better manage pre and post sales services and can simultaneously mitigate risks.

TELEMATICS IN MOTOR INSURANCE:

When applied to motor vehicles, telematics can allow insurers to monitor and record the driving behaviour of car drivers. It is essentially meant to reward good driving habits. Internationally, safe drivers are offered lower premiums than those with not-so-good driving habits. But, by and large, that is not the case in India. At present, premiums of motor insurance policies in India are priced based on parameters like the vehicle’s engine capacity, its category and purpose of use, and its age. For instance, customers who use their vehicles for lesser duration, or lesser distances, are prone to fewer risks and those who use their vehicles for longer durations and longer distances are prone to more risks; but both sets of customers today pay the same premium for a particular vehicle. There are some other parameters that can be considered in the assessment of risks with regard to a vehicle, such as: upkeep of the vehicle, how frequently it is driven, what distance it is driven for, the quality of roads it is driven on, and the driving habits of the driver. Consideration of these factors will lead to a more meaningful risk assessment and provide for a more accurate mechanism for pricing. Moreover, due to the increasing use of other modes of transport like suburban trains, other mass transit systems, employer-provided transport, taxis, and other cars on rent; some people may already not be using their own vehicles very frequently. The vehicles of these people may be in a low-risk category. On the other hand, vehicles engaged in public transport and taxi services are prone to more risks as they are on the road for longer durations each day. Today, premiums are being charged based on available information related to limited parameters only. If accurate information and more relevant data are available, premiums can be worked out more scientifically, commensurate with the risks involved.

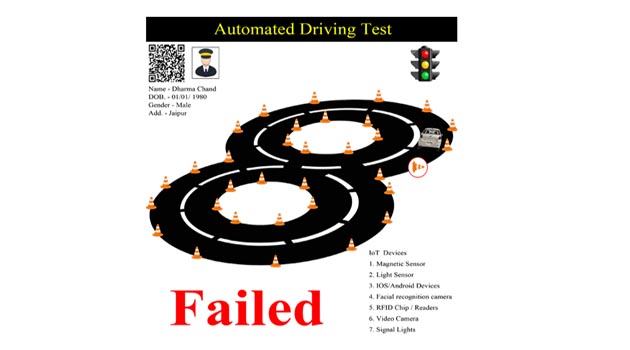

APPLICATION OF IoT DEVICE:

Especially in motor insurance customers are empowered to self-survey the loss and to file claims instantly using their smart phones, and insurers can immediately assess and settle the claims. This has significantly reduced the claim settlement time from days to minutes and provided value not just from an efficiency standpoint, but also from a time and convenience perspective for customers. Internet of Things has colossal applications in the field of Auto Insurance. IoT device embedded in a vehicle will provide information about the driving patterns to an insurer. Constraints such as average speed at which this vehicle is driven or usage of breaks will help in determining the risk profile of a driver. Based on the risk profile, an insurer can deduce the cost of an insurance policy. This cost would be much more accurate and fair to the driver, as opposed to charging a generalised price which is currently in use. This will result in higher customer satisfaction as a safe driver will have to pay a reduced cost as compared to a customer with a history of repeated claims. An IoT device embedded in a vehicle will provide real-time data to the insurer as well as the customer. Data regarding the state of various parts, detection of a failure, warning signs like speed warnings or proximity levels, will be provided. In case, an accident occurs in spite of the above-mentioned warnings, IoT devices will report the incident to the insurer. This report will be forwarded to the nearest service provider. In-turn drastically decreasing the reach time of roadside assistance service and emergency facilities at the accident spot. Customers can track the status of repairs and understand the time required to receive their repaired vehicle. Based on this, customers can also estimate the magnitude of damage and approximate claim amount that their insurer is likely to settle.

APPLICATION OF IoT DEVICE:

Especially in motor insurance customers are empowered to self-survey the loss and to file claims instantly using their smart phones, and insurers can immediately assess and settle the claims. This has significantly reduced the claim settlement time from days to minutes and provided value not just from an efficiency standpoint, but also from a time and convenience perspective for customers. Internet of Things has colossal applications in the field of Auto Insurance. IoT device embedded in a vehicle will provide information about the driving patterns to an insurer. Constraints such as average speed at which this vehicle is driven or usage of breaks will help in determining the risk profile of a driver. Based on the risk profile, an insurer can deduce the cost of an insurance policy. This cost would be much more accurate and fair to the driver, as opposed to charging a generalised price which is currently in use. This will result in higher customer satisfaction as a safe driver will have to pay a reduced cost as compared to a customer with a history of repeated claims. An IoT device embedded in a vehicle will provide real-time data to the insurer as well as the customer. Data regarding the state of various parts, detection of a failure, warning signs like speed warnings or proximity levels, will be provided. In case, an accident occurs in spite of the above-mentioned warnings, IoT devices will report the incident to the insurer. This report will be forwarded to the nearest service provider. In-turn drastically decreasing the reach time of roadside assistance service and emergency facilities at the accident spot. Customers can track the status of repairs and understand the time required to receive their repaired vehicle. Based on this, customers can also estimate the magnitude of damage and approximate claim amount that their insurer is likely to settle.

PROGRAMMING OF DRONES:

The insurance industry is transforming at a bewildering rate and there are changes in the way consumers are purchasing insurance. As opposed to traditional inspectors visiting the garage for creating an inspection report, drones can be programmed to identify the damage. Reports about the current state of parts and real-time cost of replacing them can be derived with the help of multiple IoT devices and drones. This will speed up the process of inspection and at the same time provide highly accurate reports to the insurer. General Insurance Companies in India detect around 6% of fraudulent claims in one year, resulting in a loss of $25 to $30 billion when compared to an international range of 10-15%. IoT devices have potential to drag this number downwards. With respect to auto insurance, insurers will already be aware of the state of an automobile and its parts. It will be possible to differentiate old and current damages, thus making it possible to process a claim for current damages. Drone surveys were carried out to get a clear picture in Gujarat where farmers took insurance for vulnerable groundnut but grew cotton in place of it. The drones saved the insurance companies crores of rupees. What once was associated with defence, is now transforming the way of monitoring and surveillance in the insurance sector. Drones can not only streamline insurance processes but also reduce faulty claims, while, at the same time improving customer relationships. With minimal human intervention, they capture high quality images and videos in challenging conditions like tough terrain or inclement weather.

FREE INSURANCE FOR UBER DRIVERS:

Uber Technologies Inc. rolled out a free insurance program for more than 450,000 drivers registered on its ride-hailing app in India, seeking to attract more drivers. It’s teaming up with ICICI Lombard General Insurance Co., the South Asian country’s largest private non-life insurer, to cover drivers in case of an accident while using the Uber app, en route or on an Uber trip. The policy includes accidental death and disablement, hospitalization and medical treatment. Uber has been racing local rival Ola to sign up drivers. Incentives have fallen and commission rates have risen, causing drivers for both companies to take their cabs off the roads in New Delhi, Bangalore and other cities. They are demanding accident insurance, better incentives and reasonable work hours. Ola, which has pledged to add 5 million drivers to its platform by 2022, rolled out a medical benefits program for 500,000 registered drivers, including those for street cabs and three-wheeler auto rickshaws, giving them to free health checks and accident insurance at discounted rates. Uber’s free new program includes death insurance of Rs500,000 ($7,800), as much as Rs500,000 for permanent disability, and as much as Rs200,000 for hospitalization coverage or a Rs50,000 limit for outpatient treatments.

ELECTRIC VEHICLES:

The automotive industry is on the throes of a major disruption over the next decade through electrification of vehicles, connected cars and intensification of the use of artificial intelligence. While that opens up opportunities for some, it would also mean existing players would need to adapt and adjust. The EV market in India is at a nascent but promising stage. India’s technology requirements for electric vehicles are different from that of the West due to the unique environmental condition and driving pattern. Hence, investments to make electric vehicle technology affordable are immense. With the thrust towards EVs, the government has at the same time also advanced the date for BS-VI emission norms, which is highly capital intensive. Tailoring to lessons learnt in the Indian conditions would be one jump that most would be attempting – one way to minimize the risk is with rapid prototyping and extensive fleet validation. EV is not propelled emission free as long as the power is not coming from renewable energies. Technology trends and new business models are transforming the insurance industry by leaps and bounds. The top priority of insurance company today is profitable & sustainable growth and to enable this, the global insurance carriers are taking all possible measures to deploy innovative technology for improving the business processes and streamlining legacy applications.

GREATER EMPHASIS ON TECHNOLOGY:

The insurance industry is at the threshold of a long period of growth. With the rapid change in technology and digitisation Indian auto manufacturers are laying greater emphasis on technology to make their vehicles safer after reports that base models suffered greatly in this respect during crash tests and in anticipation of the rule changes. Where installed, anti-theft devices, speed governors and ABS are said to have had an effect on safety. For instance, fewer Hondas are being stolen after the company began fitting an immobiliser in all its cars. The increasing deployment of technology helping drive down motor insurance premiums since use of devices such as immobilisers, rear view cameras, speed governors, telematics dongles that boost safety and mobile apps that capture driving behaviour. Besides this, more stringent rules results in features such as anti-lock braking systems (ABS) becoming a standard fitment on all cars. “Anybody giving proof of safety measures is rewarded with discount of up to 50% depending on make and model of the vehicle. With usage-based insurance, in-vehicle telecommunication devices (either an installed black box, smart phone app, OBD dongle or embedded telematics) are installed to gather real-time data. The behaviour of the driver – such as kilometres driven, GPS location data, any rapid acceleration, hard braking and at what time of the day a vehicle is driven – all relevant information to insurers is captured real-time. The data is analysed and risk scores are determined based on the analytics results.

Motor On The Spot (Motor OTS) – is a mobile based self survey service for motor insurance claim settlements on the spot section, nor in the own-damage section at Bajaj Allianz. It allows customers to register as well self-inspect their motor insurance claims of up to Rs. 20,000 through the company’s self-service mobile app – “Insurance Wallet”. It reduces the claim settlement period to less than 30 minutes from the current average time of 7 days for motor claim settlement. With the help of telematics and by offering connected devices fitted into cars, insurers are helping the customer get a better understanding of their driving behaviour for efficient fuel consumption, to navigate road conditions and remotely monitor the vehicle’s location. In the future, the motor insurance premium could also be directly proportional to the performance and usage of the vehicle. Many insurers have also introduced chatbots leveraging on artificial intelligence to ensure 24/7 customer support and provide instant digital solutions. This may lead in time to automated underwriting enabling insurers to issue customer policies instantaneously with a much deeper understanding of information about customers. Luckily for Indian motor insurers, the prospect of driverless cars is some time away and market growth is also not a concern. Yet, technology advancements, the increasingly connected world and the ability to collect and process data is transforming the Indian motor insurance industry. Customer experience is about to improve drastically across sales, service, renewals and claims along with increased breadth of products. Change is inevitable. Companies that strategise and re-strategise fast enough remain in the race.

PROGRAMMING OF DRONES:

The insurance industry is transforming at a bewildering rate and there are changes in the way consumers are purchasing insurance. As opposed to traditional inspectors visiting the garage for creating an inspection report, drones can be programmed to identify the damage. Reports about the current state of parts and real-time cost of replacing them can be derived with the help of multiple IoT devices and drones. This will speed up the process of inspection and at the same time provide highly accurate reports to the insurer. General Insurance Companies in India detect around 6% of fraudulent claims in one year, resulting in a loss of $25 to $30 billion when compared to an international range of 10-15%. IoT devices have potential to drag this number downwards. With respect to auto insurance, insurers will already be aware of the state of an automobile and its parts. It will be possible to differentiate old and current damages, thus making it possible to process a claim for current damages. Drone surveys were carried out to get a clear picture in Gujarat where farmers took insurance for vulnerable groundnut but grew cotton in place of it. The drones saved the insurance companies crores of rupees. What once was associated with defence, is now transforming the way of monitoring and surveillance in the insurance sector. Drones can not only streamline insurance processes but also reduce faulty claims, while, at the same time improving customer relationships. With minimal human intervention, they capture high quality images and videos in challenging conditions like tough terrain or inclement weather.

FREE INSURANCE FOR UBER DRIVERS:

Uber Technologies Inc. rolled out a free insurance program for more than 450,000 drivers registered on its ride-hailing app in India, seeking to attract more drivers. It’s teaming up with ICICI Lombard General Insurance Co., the South Asian country’s largest private non-life insurer, to cover drivers in case of an accident while using the Uber app, en route or on an Uber trip. The policy includes accidental death and disablement, hospitalization and medical treatment. Uber has been racing local rival Ola to sign up drivers. Incentives have fallen and commission rates have risen, causing drivers for both companies to take their cabs off the roads in New Delhi, Bangalore and other cities. They are demanding accident insurance, better incentives and reasonable work hours. Ola, which has pledged to add 5 million drivers to its platform by 2022, rolled out a medical benefits program for 500,000 registered drivers, including those for street cabs and three-wheeler auto rickshaws, giving them to free health checks and accident insurance at discounted rates. Uber’s free new program includes death insurance of Rs500,000 ($7,800), as much as Rs500,000 for permanent disability, and as much as Rs200,000 for hospitalization coverage or a Rs50,000 limit for outpatient treatments.

ELECTRIC VEHICLES:

The automotive industry is on the throes of a major disruption over the next decade through electrification of vehicles, connected cars and intensification of the use of artificial intelligence. While that opens up opportunities for some, it would also mean existing players would need to adapt and adjust. The EV market in India is at a nascent but promising stage. India’s technology requirements for electric vehicles are different from that of the West due to the unique environmental condition and driving pattern. Hence, investments to make electric vehicle technology affordable are immense. With the thrust towards EVs, the government has at the same time also advanced the date for BS-VI emission norms, which is highly capital intensive. Tailoring to lessons learnt in the Indian conditions would be one jump that most would be attempting – one way to minimize the risk is with rapid prototyping and extensive fleet validation. EV is not propelled emission free as long as the power is not coming from renewable energies. Technology trends and new business models are transforming the insurance industry by leaps and bounds. The top priority of insurance company today is profitable & sustainable growth and to enable this, the global insurance carriers are taking all possible measures to deploy innovative technology for improving the business processes and streamlining legacy applications.

GREATER EMPHASIS ON TECHNOLOGY:

The insurance industry is at the threshold of a long period of growth. With the rapid change in technology and digitisation Indian auto manufacturers are laying greater emphasis on technology to make their vehicles safer after reports that base models suffered greatly in this respect during crash tests and in anticipation of the rule changes. Where installed, anti-theft devices, speed governors and ABS are said to have had an effect on safety. For instance, fewer Hondas are being stolen after the company began fitting an immobiliser in all its cars. The increasing deployment of technology helping drive down motor insurance premiums since use of devices such as immobilisers, rear view cameras, speed governors, telematics dongles that boost safety and mobile apps that capture driving behaviour. Besides this, more stringent rules results in features such as anti-lock braking systems (ABS) becoming a standard fitment on all cars. “Anybody giving proof of safety measures is rewarded with discount of up to 50% depending on make and model of the vehicle. With usage-based insurance, in-vehicle telecommunication devices (either an installed black box, smart phone app, OBD dongle or embedded telematics) are installed to gather real-time data. The behaviour of the driver – such as kilometres driven, GPS location data, any rapid acceleration, hard braking and at what time of the day a vehicle is driven – all relevant information to insurers is captured real-time. The data is analysed and risk scores are determined based on the analytics results.

Motor On The Spot (Motor OTS) – is a mobile based self survey service for motor insurance claim settlements on the spot section, nor in the own-damage section at Bajaj Allianz. It allows customers to register as well self-inspect their motor insurance claims of up to Rs. 20,000 through the company’s self-service mobile app – “Insurance Wallet”. It reduces the claim settlement period to less than 30 minutes from the current average time of 7 days for motor claim settlement. With the help of telematics and by offering connected devices fitted into cars, insurers are helping the customer get a better understanding of their driving behaviour for efficient fuel consumption, to navigate road conditions and remotely monitor the vehicle’s location. In the future, the motor insurance premium could also be directly proportional to the performance and usage of the vehicle. Many insurers have also introduced chatbots leveraging on artificial intelligence to ensure 24/7 customer support and provide instant digital solutions. This may lead in time to automated underwriting enabling insurers to issue customer policies instantaneously with a much deeper understanding of information about customers. Luckily for Indian motor insurers, the prospect of driverless cars is some time away and market growth is also not a concern. Yet, technology advancements, the increasingly connected world and the ability to collect and process data is transforming the Indian motor insurance industry. Customer experience is about to improve drastically across sales, service, renewals and claims along with increased breadth of products. Change is inevitable. Companies that strategise and re-strategise fast enough remain in the race.

REFERENCES:

APPLICATION OF IoT DEVICE:

Especially in motor insurance customers are empowered to self-survey the loss and to file claims instantly using their smart phones, and insurers can immediately assess and settle the claims. This has significantly reduced the claim settlement time from days to minutes and provided value not just from an efficiency standpoint, but also from a time and convenience perspective for customers. Internet of Things has colossal applications in the field of Auto Insurance. IoT device embedded in a vehicle will provide information about the driving patterns to an insurer. Constraints such as average speed at which this vehicle is driven or usage of breaks will help in determining the risk profile of a driver. Based on the risk profile, an insurer can deduce the cost of an insurance policy. This cost would be much more accurate and fair to the driver, as opposed to charging a generalised price which is currently in use. This will result in higher customer satisfaction as a safe driver will have to pay a reduced cost as compared to a customer with a history of repeated claims. An IoT device embedded in a vehicle will provide real-time data to the insurer as well as the customer. Data regarding the state of various parts, detection of a failure, warning signs like speed warnings or proximity levels, will be provided. In case, an accident occurs in spite of the above-mentioned warnings, IoT devices will report the incident to the insurer. This report will be forwarded to the nearest service provider. In-turn drastically decreasing the reach time of roadside assistance service and emergency facilities at the accident spot. Customers can track the status of repairs and understand the time required to receive their repaired vehicle. Based on this, customers can also estimate the magnitude of damage and approximate claim amount that their insurer is likely to settle.

PROGRAMMING OF DRONES:

The insurance industry is transforming at a bewildering rate and there are changes in the way consumers are purchasing insurance. As opposed to traditional inspectors visiting the garage for creating an inspection report, drones can be programmed to identify the damage. Reports about the current state of parts and real-time cost of replacing them can be derived with the help of multiple IoT devices and drones. This will speed up the process of inspection and at the same time provide highly accurate reports to the insurer. General Insurance Companies in India detect around 6% of fraudulent claims in one year, resulting in a loss of $25 to $30 billion when compared to an international range of 10-15%. IoT devices have potential to drag this number downwards. With respect to auto insurance, insurers will already be aware of the state of an automobile and its parts. It will be possible to differentiate old and current damages, thus making it possible to process a claim for current damages. Drone surveys were carried out to get a clear picture in Gujarat where farmers took insurance for vulnerable groundnut but grew cotton in place of it. The drones saved the insurance companies crores of rupees. What once was associated with defence, is now transforming the way of monitoring and surveillance in the insurance sector. Drones can not only streamline insurance processes but also reduce faulty claims, while, at the same time improving customer relationships. With minimal human intervention, they capture high quality images and videos in challenging conditions like tough terrain or inclement weather.

FREE INSURANCE FOR UBER DRIVERS:

Uber Technologies Inc. rolled out a free insurance program for more than 450,000 drivers registered on its ride-hailing app in India, seeking to attract more drivers. It’s teaming up with ICICI Lombard General Insurance Co., the South Asian country’s largest private non-life insurer, to cover drivers in case of an accident while using the Uber app, en route or on an Uber trip. The policy includes accidental death and disablement, hospitalization and medical treatment. Uber has been racing local rival Ola to sign up drivers. Incentives have fallen and commission rates have risen, causing drivers for both companies to take their cabs off the roads in New Delhi, Bangalore and other cities. They are demanding accident insurance, better incentives and reasonable work hours. Ola, which has pledged to add 5 million drivers to its platform by 2022, rolled out a medical benefits program for 500,000 registered drivers, including those for street cabs and three-wheeler auto rickshaws, giving them to free health checks and accident insurance at discounted rates. Uber’s free new program includes death insurance of Rs500,000 ($7,800), as much as Rs500,000 for permanent disability, and as much as Rs200,000 for hospitalization coverage or a Rs50,000 limit for outpatient treatments.

ELECTRIC VEHICLES:

The automotive industry is on the throes of a major disruption over the next decade through electrification of vehicles, connected cars and intensification of the use of artificial intelligence. While that opens up opportunities for some, it would also mean existing players would need to adapt and adjust. The EV market in India is at a nascent but promising stage. India’s technology requirements for electric vehicles are different from that of the West due to the unique environmental condition and driving pattern. Hence, investments to make electric vehicle technology affordable are immense. With the thrust towards EVs, the government has at the same time also advanced the date for BS-VI emission norms, which is highly capital intensive. Tailoring to lessons learnt in the Indian conditions would be one jump that most would be attempting – one way to minimize the risk is with rapid prototyping and extensive fleet validation. EV is not propelled emission free as long as the power is not coming from renewable energies. Technology trends and new business models are transforming the insurance industry by leaps and bounds. The top priority of insurance company today is profitable & sustainable growth and to enable this, the global insurance carriers are taking all possible measures to deploy innovative technology for improving the business processes and streamlining legacy applications.

GREATER EMPHASIS ON TECHNOLOGY:

The insurance industry is at the threshold of a long period of growth. With the rapid change in technology and digitisation Indian auto manufacturers are laying greater emphasis on technology to make their vehicles safer after reports that base models suffered greatly in this respect during crash tests and in anticipation of the rule changes. Where installed, anti-theft devices, speed governors and ABS are said to have had an effect on safety. For instance, fewer Hondas are being stolen after the company began fitting an immobiliser in all its cars. The increasing deployment of technology helping drive down motor insurance premiums since use of devices such as immobilisers, rear view cameras, speed governors, telematics dongles that boost safety and mobile apps that capture driving behaviour. Besides this, more stringent rules results in features such as anti-lock braking systems (ABS) becoming a standard fitment on all cars. “Anybody giving proof of safety measures is rewarded with discount of up to 50% depending on make and model of the vehicle. With usage-based insurance, in-vehicle telecommunication devices (either an installed black box, smart phone app, OBD dongle or embedded telematics) are installed to gather real-time data. The behaviour of the driver – such as kilometres driven, GPS location data, any rapid acceleration, hard braking and at what time of the day a vehicle is driven – all relevant information to insurers is captured real-time. The data is analysed and risk scores are determined based on the analytics results.

Motor On The Spot (Motor OTS) – is a mobile based self survey service for motor insurance claim settlements on the spot section, nor in the own-damage section at Bajaj Allianz. It allows customers to register as well self-inspect their motor insurance claims of up to Rs. 20,000 through the company’s self-service mobile app – “Insurance Wallet”. It reduces the claim settlement period to less than 30 minutes from the current average time of 7 days for motor claim settlement. With the help of telematics and by offering connected devices fitted into cars, insurers are helping the customer get a better understanding of their driving behaviour for efficient fuel consumption, to navigate road conditions and remotely monitor the vehicle’s location. In the future, the motor insurance premium could also be directly proportional to the performance and usage of the vehicle. Many insurers have also introduced chatbots leveraging on artificial intelligence to ensure 24/7 customer support and provide instant digital solutions. This may lead in time to automated underwriting enabling insurers to issue customer policies instantaneously with a much deeper understanding of information about customers. Luckily for Indian motor insurers, the prospect of driverless cars is some time away and market growth is also not a concern. Yet, technology advancements, the increasingly connected world and the ability to collect and process data is transforming the Indian motor insurance industry. Customer experience is about to improve drastically across sales, service, renewals and claims along with increased breadth of products. Change is inevitable. Companies that strategise and re-strategise fast enough remain in the race.

REFERENCES:

- https://inc42.com/resources/iot-auto-insurance-industry

- http://www.livemint.com/Opinion/dzXVslZzB04TF1TXMZ5eFN/The-changing-face-of-motor-insurance-in-India.html

- https://www.icicilombard.com/insurance-information/travel-insurance-info

- https://cio.economictimes.indiatimes.com/news/enterprise-services-and-applications

- http://www.yusata.com/menus/news.html

- Newspapers & Journals

Author

JAGENDRA KUMAR, Ex. CEO, Pearl Insurance Brokers

Leave a Reply