Allianz Risk Barometer: Cyber incidents and Business interruption dominate risk landscape for companies of all sizes in India in 2018

- Evolving nature of risk, and rise in cyber-related incidents, means business interruption ranks as top threat for companies globally, according to 1,900+ risk experts from 80 countries.

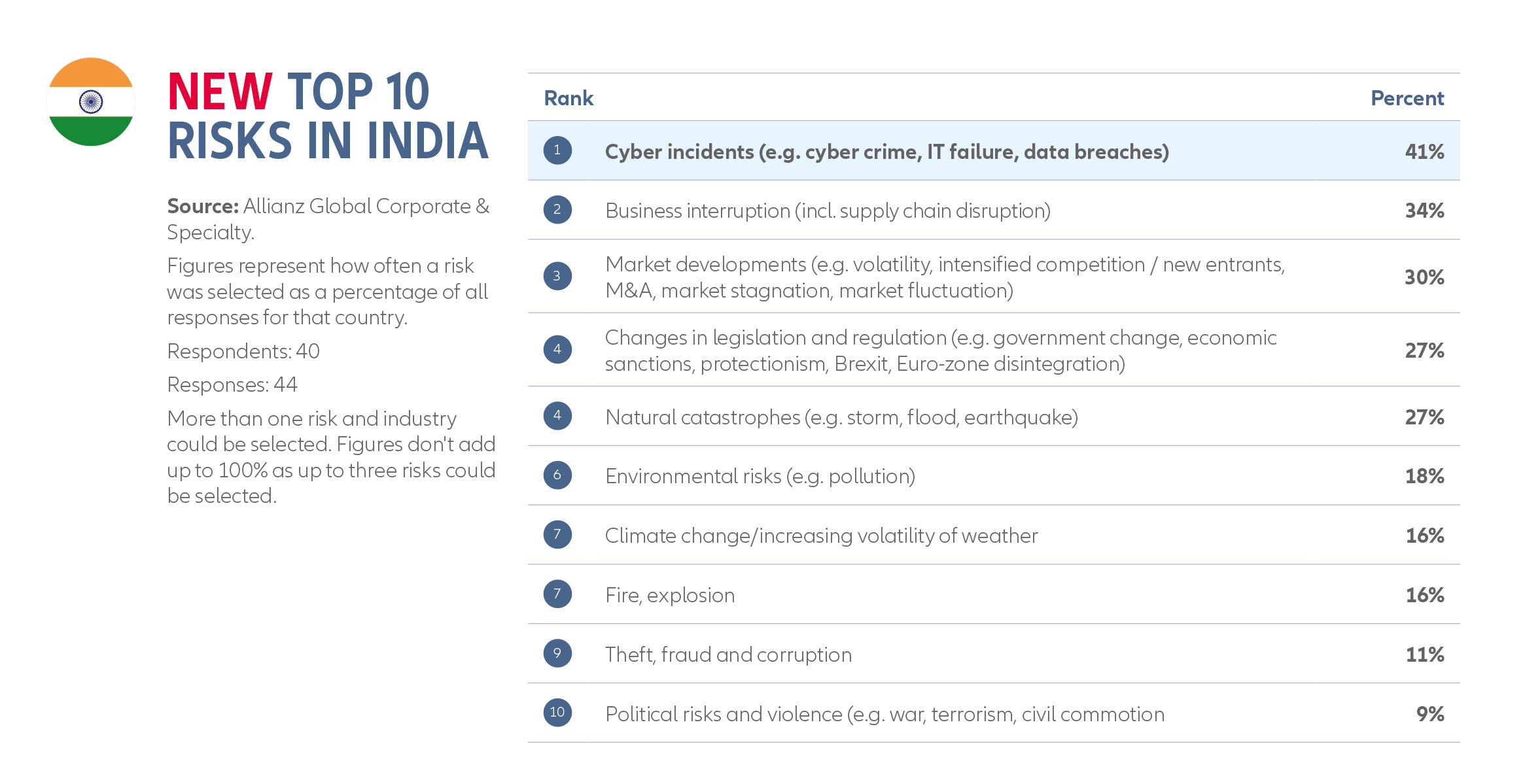

- India included for the first time in global survey, saw cyber incidents top the list with potential “cyber hurricane” events and tougher data protection rules shaping cyber risk environment for year-ahead. Crisis response crucial for mitigation.

- Rising FDI and new entrants into India has put Market Developments in third place as businesses grapple with intensified competition and rising M&A activities.

- Other risks include Legislation and Regulation in light of India’s push towards liberalisation as well as Natural Catastrophes, which are both tied at fourth place.

India, January 22, 2018: They take aim at the backbone of the connected economy and, when they strike, can jeopardize the success, or even the existence, of companies of every size and sector. Business interruption (# 1 with 42% of responses / # 1 in 2017) and Cyber incidents (# 2 with 40% of responses, up from # 3 in 2017) are this year’s top business risks globally, according to the Allianz Risk Barometer 2018. In India, the top two risks are ranked in reverse, with Cyber taking the top spot with a 7% lead over Business Interruption.

These are the key findings of the seventh Allianz Risk Barometer, which is published annually by Allianz Global Corporate & Specialty (AGCS).The 2018 report is based on the insights of a record 1,911 risk experts from 80 countries which includes 372 respondents from Asia.

“For the first time, business interruption and cyber risk are neck-and-neck globally in the Allianz Risk Barometer and these risks are increasingly interlinked,” says Chris Fischer Hirs, Chief Executive Officer, AGCS. “Whether resulting from attacks such as WannaCry, or more frequently, system failures, cyber incidents are now a major cause of business interruption for today’s networked companies whose primary assets are often data, service platforms or their groups of customers and suppliers. However, last year’s severe natural disasters remind us that the impact of perennial perils shouldn’t be underestimated either. Risk managers face a highly complex and volatile environment of both traditional business risks and new technology challenges in future.”

New business interruption triggers emerging

Business interruption (BI) is the most important risk globally for the sixth year in a row, ranking top in 13 countries and the Europe, Asia Pacific, and Africa & Middle East regions. No business is too small to be impacted. Companies face an increasing number of scenarios, ranging from traditional exposures, such as fire, natural disasters and supply chain disruption, to new triggers stemming from digitalization and interconnectedness that typically come without physical damage, but with high financial loss. Breakdown of core IT systems, terrorism or political violence events, product quality incidents or an unexpected regulatory change can bring businesses to a temporary or prolonged standstill with a devastating effect on revenues.

For the first time, cyber incidents also rank as the most feared BI trigger, according to businesses and risk experts, with BI also considered the largest loss driver after a cyber incident. Cyber-attacks caused businesses to lose revenues of approximately $81 billion in the Asia-Pacific region between September 2014 and September 2015[1].

BI also ranks as the second most underestimated risk in the Allianz Risk Barometer. “Businesses can be surprised about the actual cause, scope and financial impact of a disruption and underestimate the complexity of ‘getting back to business’. They should continuously fine tune their emergency and business continuity plans to reflect the new BI environment and adequately consider the rising cyber BI threat,” says Volker Muench, Global Property and BI expert, AGCS.

Cyber risks continue to evolve

Cyber incidents continues its upward trend in the Allianz Risk Barometer. Five years ago it ranked # 15. In 2018 it is # 2 globally. Multiple threats such as data breaches, network liability, hacker attacks or cyber BI, ensure it is the top business risk in 11 surveyed countries including India, Singapore and Indonesia. It also ranks as the most underestimated risk and the major long-term peril.

In India, the Reserve Bank of India revealed that from 2014-2017, banks across the country lost about US$37.87 million (Rs252 crore) to cyber crime or an average of $1388 (Rs88,553) an hour. Across Asia Pacific, businesses also saw their operations disrupted by recent events such as the WannaCry and Petya ransomware attacks, which brought significant financial losses to a large number of businesses in other parts of the world. On an individual level, recently identified security flaws in computer chips in nearly every modern device reveal the cyber vulnerability of modern societies. The potential for so-called “cyber hurricane” events to occur, where hackers disrupt larger numbers of companies by targeting common infrastructure dependencies, will continue to grow in 2018.

“The rise in cyber crime is not just an indication of vulnerable back-end systems but also a warning that businesses cannot underestimate the threat any longer. Experience has shown that a company’s response to a cyber crisis, such as a breach, has a direct impact on the cost, as well as on a company’s reputation and market value,” says AGCS’s Global Head of Cyber, Emy Donavan.

Cyber threats also vary according to company size or industry. “Small companies are likely to be crippled if hit with a ransomware attack, while larger firms are targets of a greater range of threats, such as the distributed denial of service (DDoS) attacks which can overwhelm systems,” says Donavan.

Allianz Risk Barometer results show that awareness of the cyber threat is soaring among small- and medium-sized businesses, with a significant jump from # 6 to # 2 for small companies and from # 3 to # 1 for medium-sized companies. With regard to sector exposure, cyber incidents rank top in the Entertainment & Media, Financial Services, Technology and Telecommunications industries.

Market Developments and Regulation rising concerns

Globally, businesses are less concerned about the risk of Market Developments, however in India the scenario is the reverse. With Foreign Direct Investment (FDI) in India increasingly steadily over the last three years and hitting an all-time high in 2016-2017 at $60.08 billion, companies in India are grappling with intensified competition and increased M&A activity. With record amounts of cash on balance sheets, another M&A wave is expected in 2018, as increasing share buybacks cast doubt on the ability to grow organically in the face of the digital revolution.

In addition to this, in light of the Government’s push towards market liberalization, businesses are also faced with increased regulatory reform, which places additional pressure on compliance costs and efficiency.

Weather and technology risk on the rise

After a record-breaking $135 billion in insured losses from natural catastrophes alone in 2017[2] – the highest ever – driven by hurricanes Harvey, Irma and Maria in the United States and the Caribbean, Natural catastrophes returns to the top three business risks globally and at fourth place in India. In Asia, Typhoon Hato wreaked havoc in Hong Kong, Macau and southern China and was the worst natural disaster Macau had encountered in more than 50 years.

In India, widespread floods continued to plague the country last year and are expected to be a perennial challenge. According to AGCS research, of the Top 10 global cities ranked by assets, most exposed to flooding in the next 50 years, two cities are from India (Mumbai & Calcutta). The remaining eight cities hail from US, China, Japan and Thailand.

“In terms of insured losses, 2017 was the costliest natural catastrophe year in five years. Despite most catastrophes taking place in North America and Mexico, they still impact Asia, as 50% of claims by value are from companies not based in these areas but from subsidiaries of multi-national companies located outside the disaster zones,” says Mark Mitchell, Chief Executive Officer, AGCS Asia. “This reflects the growing trend of globalization and the need for multinational companies to adopt a global approach to risk exposures and insurance coverage. As manufacturing shifts east, Asia is increasingly exposed to such disasters because of economic growth and concentration of suppliers. Manufacturing and outsourced services have migrated to China, India and other high-growth markets in South East Asia and so too have large claims.”

“The impact of natural catastrophes goes far beyond the physical damage to structures in the affected areas. As industries become leaner and more connected, natural catastrophes can disrupt a large variety of sectors that might not seem directly affected at first glance around the world,” adds Ali Shahkarami, Head of Catastrophe Risk Research, AGCS.

Respondents fear 2017 could be a harbinger of increasing intensity and frequency of natural hazards. Climate change/increasing weather volatility is a new entrant in the Risk Barometer top 10 in 2018 and the loss potential for businesses is further exacerbated by rapid urbanization in coastal areas.

English version of the report: http://www.agcs.allianz.com/assets/PDFs/Reports/Allianz_Risk_Barometer_2018_EN.pdf

Appendix document http://www.agcs.allianz.com/assets/PDFs/Reports/Allianz_Risk_Barometer_2018_APPENDIX.pdf

Press contacts

Singapore: Wendy Koh +65 6395 3796 [email protected]

About Allianz Global Corporate & Specialty

Allianz Global Corporate & Specialty (AGCS) is the Allianz Group’s dedicated carrier for corporate and specialty insurance business. AGCS provides insurance and risk consultancy across the whole spectrum of specialty, alternative risk transfer and corporate business: Marine, Aviation (incl. Space), Energy, Engineering, Entertainment, Financial Lines (incl. D&O), Liability, Mid-Corporate and Property insurance (incl. International Insurance Programs).

Worldwide, AGCS operates in 32 countries with own units and in over 210 countries and territories through the Allianz Group network and partners. In 2016, it employed around 5,000 people and provided insurance solutions to more than three quarters of the Fortune Global 500 companies, writing a total of €7.6 billion gross premium worldwide annually.

AGCS SE is rated AA by Standard & Poor’s and A+ by A.M. Best.

For more information please visit www.agcs.allianz.com or follow us on Twitter @AGCS_Insurance LinkedIn and Google+.

Forward-looking statementsThe statements contained herein may include prospects, statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such forward-looking statements.

Such deviations may arise due to, without limitation, (i) changes of the general economic conditions and competitive situation, particularly in the Allianz Group’s core business and core markets, (ii) performance of financial markets (particularly market volatility, liquidity and credit events) (iii) frequency and severity of insured loss events, including from natural catastrophes, and the development of loss expenses, (iv) mortality and morbidity levels and trends, (v) persistency levels, (vi) particularly in the banking business, the extent of credit defaults, (vii) interest rate levels, (viii) currency exchange rates including the Euro/U.S. Dollar exchange rate, (ix) changes in laws and regulations, including tax regulations, (x) the impact of acquisitions, including related integration issues, and reorganization measures, and (xi) general competitive factors, in each case on a local, regional, national and/or global basis. Many of these factors may be more likely to occur, or more pronounced, as a result of terrorist activities and their consequences.

No duty to update The company assumes no obligation to update any information or forward-looking statement contained herein, save for any information required to be disclosed by law.

Leave a Reply